Saneesh Edacherian, Ansgar Richter, Amit Karna, Balagopal Gopalakrishnan

{"title":"连接正确的结:董事会委员会联锁对印度公司业绩的影响","authors":"Saneesh Edacherian, Ansgar Richter, Amit Karna, Balagopal Gopalakrishnan","doi":"10.1111/corg.12523","DOIUrl":null,"url":null,"abstract":"<div>\n \n \n <section>\n \n <h3> Research Question/Issue</h3>\n \n <p>Information processing, agency, and resource dependence perspectives provide diverging predictions regarding the relationship between board interlocks and firm performance, which are rooted in different perspectives on the roles of boards of directors. This study argues that these various approaches are reconcilable when considering the nature of board <i>committees</i> to which the interlocked directors are assigned.</p>\n </section>\n \n <section>\n \n <h3> Research Findings/Insights</h3>\n \n <p>We test our hypotheses on a sample of 5133 firm-year observations in India. Our analyses support our hypotheses. The results show that interlocks between audit committees, whose primary function relates to providing financial oversight and ensuring compliance, are negatively related to firm performance. In contrast, interlocks between nomination and remuneration committees of Indian firms, which provide them with access to resources such as human capital and information on appropriate incentive structures, are positively related to performance.</p>\n </section>\n \n <section>\n \n <h3> Theoretical/Academic Implications</h3>\n \n <p>Our study clarifies the relationship between board committee interlocks and firm performance by taking a multi-theoretical perspective. Our analysis suggests that information processing, agency, and resource dependence theories complement one another in explaining the effect of interlocks on firm performance.</p>\n </section>\n \n <section>\n \n <h3> Practitioner/Policy Implications</h3>\n \n <p>Our results show that it is not board interlocks per se that are detrimental to firm performance; in fact, appointing well-connected directors with experience in serving on other boards might be beneficial for firms. However, firms should not assign specific monitoring-intensive tasks such as auditing to directors who also serve on other firms' audit committees. Our findings suggest that these directors should have greater independence and focus.</p>\n </section>\n </div>","PeriodicalId":48209,"journal":{"name":"Corporate Governance-An International Review","volume":"32 1","pages":"135-155"},"PeriodicalIF":4.6000,"publicationDate":"2023-03-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/corg.12523","citationCount":"0","resultStr":"{\"title\":\"Connecting the right knots: The impact of board committee interlocks on the performance of Indian firms\",\"authors\":\"Saneesh Edacherian, Ansgar Richter, Amit Karna, Balagopal Gopalakrishnan\",\"doi\":\"10.1111/corg.12523\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div>\\n \\n \\n <section>\\n \\n <h3> Research Question/Issue</h3>\\n \\n <p>Information processing, agency, and resource dependence perspectives provide diverging predictions regarding the relationship between board interlocks and firm performance, which are rooted in different perspectives on the roles of boards of directors. This study argues that these various approaches are reconcilable when considering the nature of board <i>committees</i> to which the interlocked directors are assigned.</p>\\n </section>\\n \\n <section>\\n \\n <h3> Research Findings/Insights</h3>\\n \\n <p>We test our hypotheses on a sample of 5133 firm-year observations in India. Our analyses support our hypotheses. The results show that interlocks between audit committees, whose primary function relates to providing financial oversight and ensuring compliance, are negatively related to firm performance. In contrast, interlocks between nomination and remuneration committees of Indian firms, which provide them with access to resources such as human capital and information on appropriate incentive structures, are positively related to performance.</p>\\n </section>\\n \\n <section>\\n \\n <h3> Theoretical/Academic Implications</h3>\\n \\n <p>Our study clarifies the relationship between board committee interlocks and firm performance by taking a multi-theoretical perspective. Our analysis suggests that information processing, agency, and resource dependence theories complement one another in explaining the effect of interlocks on firm performance.</p>\\n </section>\\n \\n <section>\\n \\n <h3> Practitioner/Policy Implications</h3>\\n \\n <p>Our results show that it is not board interlocks per se that are detrimental to firm performance; in fact, appointing well-connected directors with experience in serving on other boards might be beneficial for firms. However, firms should not assign specific monitoring-intensive tasks such as auditing to directors who also serve on other firms' audit committees. Our findings suggest that these directors should have greater independence and focus.</p>\\n </section>\\n </div>\",\"PeriodicalId\":48209,\"journal\":{\"name\":\"Corporate Governance-An International Review\",\"volume\":\"32 1\",\"pages\":\"135-155\"},\"PeriodicalIF\":4.6000,\"publicationDate\":\"2023-03-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/corg.12523\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Corporate Governance-An International Review\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/corg.12523\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Corporate Governance-An International Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/corg.12523","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

Connecting the right knots: The impact of board committee interlocks on the performance of Indian firms

Research Question/Issue

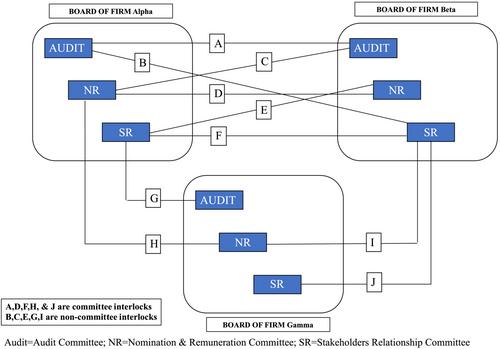

Information processing, agency, and resource dependence perspectives provide diverging predictions regarding the relationship between board interlocks and firm performance, which are rooted in different perspectives on the roles of boards of directors. This study argues that these various approaches are reconcilable when considering the nature of board committees to which the interlocked directors are assigned.

Research Findings/Insights

We test our hypotheses on a sample of 5133 firm-year observations in India. Our analyses support our hypotheses. The results show that interlocks between audit committees, whose primary function relates to providing financial oversight and ensuring compliance, are negatively related to firm performance. In contrast, interlocks between nomination and remuneration committees of Indian firms, which provide them with access to resources such as human capital and information on appropriate incentive structures, are positively related to performance.

Theoretical/Academic Implications

Our study clarifies the relationship between board committee interlocks and firm performance by taking a multi-theoretical perspective. Our analysis suggests that information processing, agency, and resource dependence theories complement one another in explaining the effect of interlocks on firm performance.

Practitioner/Policy Implications

Our results show that it is not board interlocks per se that are detrimental to firm performance; in fact, appointing well-connected directors with experience in serving on other boards might be beneficial for firms. However, firms should not assign specific monitoring-intensive tasks such as auditing to directors who also serve on other firms' audit committees. Our findings suggest that these directors should have greater independence and focus.

期刊介绍:

The mission of Corporate Governance: An International Review is to publish cutting-edge international business research on the phenomena of comparative corporate governance throughout the global economy. Our ultimate goal is a rigorous and relevant global theory of corporate governance. We define corporate governance broadly as the exercise of power over corporate entities so as to increase the value provided to the organization"s various stakeholders, as well as making those stakeholders accountable for acting responsibly with regard to the protection, generation, and distribution of wealth invested in the firm. Because of this broad conceptualization, a wide variety of academic disciplines can contribute to our understanding.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: