{"title":"利用地缘政治风险预测欧盟农产品期货波动性:GARCH-MIDAS 模型提供的证据","authors":"Hengzhen Lu, Qiujin Gao, Ling Xiao, Gurjeet Dhesi","doi":"10.1007/s11846-023-00722-0","DOIUrl":null,"url":null,"abstract":"<p>This paper examines whether the information contained in geopolitical risk (<i>GPR</i>) can improve the forecasting power of price volatility for carbon futures traded in the EU Emission Trading System. We employ the GARCH-MIDAS model and its extended forms to estimate and forecast the price volatility of carbon futures using the most informative <i>GPR</i> indicators. The models are examined for both statistical and economic significance. According to the results of the Model Confidence Set tests for the full-sample and sub-sample data, we find that the extended model, which accounts for the threat of geopolitical risk, exhibits superior forecasting ability for the full-sample data, while the model that includes drastic changes in geopolitical risk in Phase II and the model that considers serious geopolitical risk in Phase III have the best predictive power. Moreover, all <i>GPR</i>-related variables we use contribute to increasing economic gains. In particular, the threat of geopolitical risk contains valuable information for future EUA futures volatility and can provide the highest economic gains. Therefore, carbon market investors and policymakers should pay great attention to geopolitical risk, especially its threat, in risk and portfolio management.</p>","PeriodicalId":20992,"journal":{"name":"Review of Managerial Science","volume":"12 1","pages":""},"PeriodicalIF":9.6000,"publicationDate":"2024-01-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Forecasting EUA futures volatility with geopolitical risk: evidence from GARCH-MIDAS models\",\"authors\":\"Hengzhen Lu, Qiujin Gao, Ling Xiao, Gurjeet Dhesi\",\"doi\":\"10.1007/s11846-023-00722-0\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper examines whether the information contained in geopolitical risk (<i>GPR</i>) can improve the forecasting power of price volatility for carbon futures traded in the EU Emission Trading System. We employ the GARCH-MIDAS model and its extended forms to estimate and forecast the price volatility of carbon futures using the most informative <i>GPR</i> indicators. The models are examined for both statistical and economic significance. According to the results of the Model Confidence Set tests for the full-sample and sub-sample data, we find that the extended model, which accounts for the threat of geopolitical risk, exhibits superior forecasting ability for the full-sample data, while the model that includes drastic changes in geopolitical risk in Phase II and the model that considers serious geopolitical risk in Phase III have the best predictive power. Moreover, all <i>GPR</i>-related variables we use contribute to increasing economic gains. In particular, the threat of geopolitical risk contains valuable information for future EUA futures volatility and can provide the highest economic gains. Therefore, carbon market investors and policymakers should pay great attention to geopolitical risk, especially its threat, in risk and portfolio management.</p>\",\"PeriodicalId\":20992,\"journal\":{\"name\":\"Review of Managerial Science\",\"volume\":\"12 1\",\"pages\":\"\"},\"PeriodicalIF\":9.6000,\"publicationDate\":\"2024-01-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Managerial Science\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s11846-023-00722-0\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"MANAGEMENT\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Managerial Science","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11846-023-00722-0","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MANAGEMENT","Score":null,"Total":0}

Forecasting EUA futures volatility with geopolitical risk: evidence from GARCH-MIDAS models

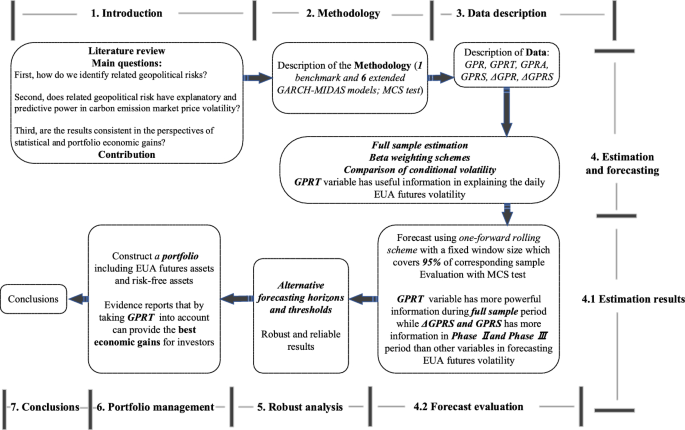

This paper examines whether the information contained in geopolitical risk (GPR) can improve the forecasting power of price volatility for carbon futures traded in the EU Emission Trading System. We employ the GARCH-MIDAS model and its extended forms to estimate and forecast the price volatility of carbon futures using the most informative GPR indicators. The models are examined for both statistical and economic significance. According to the results of the Model Confidence Set tests for the full-sample and sub-sample data, we find that the extended model, which accounts for the threat of geopolitical risk, exhibits superior forecasting ability for the full-sample data, while the model that includes drastic changes in geopolitical risk in Phase II and the model that considers serious geopolitical risk in Phase III have the best predictive power. Moreover, all GPR-related variables we use contribute to increasing economic gains. In particular, the threat of geopolitical risk contains valuable information for future EUA futures volatility and can provide the highest economic gains. Therefore, carbon market investors and policymakers should pay great attention to geopolitical risk, especially its threat, in risk and portfolio management.

期刊介绍:

Review of Managerial Science (RMS) provides a forum for innovative research from all scientific areas of business administration. The journal publishes original research of high quality and is open to various methodological approaches (analytical modeling, empirical research, experimental work, methodological reasoning etc.). The scope of RMS encompasses – but is not limited to – accounting, auditing, banking, business strategy, corporate governance, entrepreneurship, financial structure and capital markets, health economics, human resources management, information systems, innovation management, insurance, marketing, organization, production and logistics, risk management and taxation. RMS also encourages the submission of papers combining ideas and/or approaches from different areas in an innovative way. Review papers presenting the state of the art of a research area and pointing out new directions for further research are also welcome. The scientific standards of RMS are guaranteed by a rigorous, double-blind peer review process with ad hoc referees and the journal´s internationally composed editorial board.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: