{"title":"全球金融周期的替代措施:它们有区别吗?","authors":"Xin Tian, Jan P. A. M. Jacobs, Jakob de Haan","doi":"10.1002/ijfe.2884","DOIUrl":null,"url":null,"abstract":"<p>We developed several measures to analyze the global financial cycle employing dynamic factor models and data for 25 advanced and emerging countries spanning 1980 to 2019. These measures were assessed using the similarity and synchronicity metrics proposed by Mink et al. (<i>Oxford Economic Papers 64, 217–236, 2012</i>). The findings indicate a strong similarity and synchronization of global cycles in asset prices and capital flows, particularly evident during crisis episodes. Furthermore, we observe significant co-movement between our financial cycle measures and two literature-based measures that utilize top-down and bottom-up approaches. However, the VIX index shows a lower level of co-movement with our global financial cycle measures.</p>","PeriodicalId":47461,"journal":{"name":"International Journal of Finance & Economics","volume":"29 4","pages":"4483-4498"},"PeriodicalIF":2.8000,"publicationDate":"2023-09-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2884","citationCount":"0","resultStr":"{\"title\":\"Alternative measures for the global financial cycle: Do they make a difference?\",\"authors\":\"Xin Tian, Jan P. A. M. Jacobs, Jakob de Haan\",\"doi\":\"10.1002/ijfe.2884\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We developed several measures to analyze the global financial cycle employing dynamic factor models and data for 25 advanced and emerging countries spanning 1980 to 2019. These measures were assessed using the similarity and synchronicity metrics proposed by Mink et al. (<i>Oxford Economic Papers 64, 217–236, 2012</i>). The findings indicate a strong similarity and synchronization of global cycles in asset prices and capital flows, particularly evident during crisis episodes. Furthermore, we observe significant co-movement between our financial cycle measures and two literature-based measures that utilize top-down and bottom-up approaches. However, the VIX index shows a lower level of co-movement with our global financial cycle measures.</p>\",\"PeriodicalId\":47461,\"journal\":{\"name\":\"International Journal of Finance & Economics\",\"volume\":\"29 4\",\"pages\":\"4483-4498\"},\"PeriodicalIF\":2.8000,\"publicationDate\":\"2023-09-13\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2884\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Finance & Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2884\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Finance & Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2884","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Alternative measures for the global financial cycle: Do they make a difference?

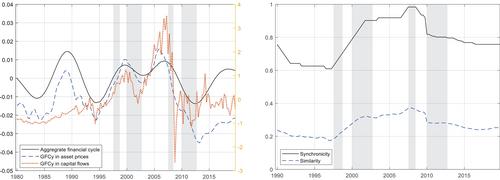

We developed several measures to analyze the global financial cycle employing dynamic factor models and data for 25 advanced and emerging countries spanning 1980 to 2019. These measures were assessed using the similarity and synchronicity metrics proposed by Mink et al. (Oxford Economic Papers 64, 217–236, 2012). The findings indicate a strong similarity and synchronization of global cycles in asset prices and capital flows, particularly evident during crisis episodes. Furthermore, we observe significant co-movement between our financial cycle measures and two literature-based measures that utilize top-down and bottom-up approaches. However, the VIX index shows a lower level of co-movement with our global financial cycle measures.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: