Taehyun Lee, Ioannis C. Moutzouris, Nikos C. Papapostolou, Mahmoud Fatouh

{"title":"利用制度转换模型进行外汇套期保值:英镑案例","authors":"Taehyun Lee, Ioannis C. Moutzouris, Nikos C. Papapostolou, Mahmoud Fatouh","doi":"10.1002/ijfe.2893","DOIUrl":null,"url":null,"abstract":"<p>We develop a four-state regime-switching model for optimal foreign exchange (FX) hedging using forward contracts. The states correspond to four distinct market conditions, each defined by the direction and magnitude of deviation of the prevailing FX spot rate from its long-term trends. The model's performance is evaluated for five currencies against the pound sterling for various horizons. Our examination compares the hedging outcomes of the proposed model to those of other commonly employed hedging methods. The empirical results suggest that our model demonstrates the highest level of risk reduction for the US dollar, euro, Japanese yen and Turkish lira and the second-best performance for the Indian rupee. The risk reduction is significantly higher for lira compared with the other approaches, implying that the proposed model might be able to provide much more effective hedging for highly volatile currencies. The improved performance of the model can be attributed to the adjustability of the estimation horizon for the optimal hedge ratio based on the prevailing market conditions. This, in turn, allows it to better capture fat-tail properties that are frequently observed in FX returns. Our findings suggest that FX investors tend to use short-term memory during low market conditions (relative to trend) and long-term memory in high ones. The results would be also useful to build a better understanding of how investor behaviour depends on market conditions and mitigate the adverse behavioural implications of short-term memory, such as panic.</p>","PeriodicalId":47461,"journal":{"name":"International Journal of Finance & Economics","volume":"29 4","pages":"4813-4835"},"PeriodicalIF":2.8000,"publicationDate":"2023-10-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2893","citationCount":"0","resultStr":"{\"title\":\"Foreign exchange hedging using regime-switching models: The case of pound sterling\",\"authors\":\"Taehyun Lee, Ioannis C. Moutzouris, Nikos C. Papapostolou, Mahmoud Fatouh\",\"doi\":\"10.1002/ijfe.2893\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We develop a four-state regime-switching model for optimal foreign exchange (FX) hedging using forward contracts. The states correspond to four distinct market conditions, each defined by the direction and magnitude of deviation of the prevailing FX spot rate from its long-term trends. The model's performance is evaluated for five currencies against the pound sterling for various horizons. Our examination compares the hedging outcomes of the proposed model to those of other commonly employed hedging methods. The empirical results suggest that our model demonstrates the highest level of risk reduction for the US dollar, euro, Japanese yen and Turkish lira and the second-best performance for the Indian rupee. The risk reduction is significantly higher for lira compared with the other approaches, implying that the proposed model might be able to provide much more effective hedging for highly volatile currencies. The improved performance of the model can be attributed to the adjustability of the estimation horizon for the optimal hedge ratio based on the prevailing market conditions. This, in turn, allows it to better capture fat-tail properties that are frequently observed in FX returns. Our findings suggest that FX investors tend to use short-term memory during low market conditions (relative to trend) and long-term memory in high ones. The results would be also useful to build a better understanding of how investor behaviour depends on market conditions and mitigate the adverse behavioural implications of short-term memory, such as panic.</p>\",\"PeriodicalId\":47461,\"journal\":{\"name\":\"International Journal of Finance & Economics\",\"volume\":\"29 4\",\"pages\":\"4813-4835\"},\"PeriodicalIF\":2.8000,\"publicationDate\":\"2023-10-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2893\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Finance & Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2893\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Finance & Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2893","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Foreign exchange hedging using regime-switching models: The case of pound sterling

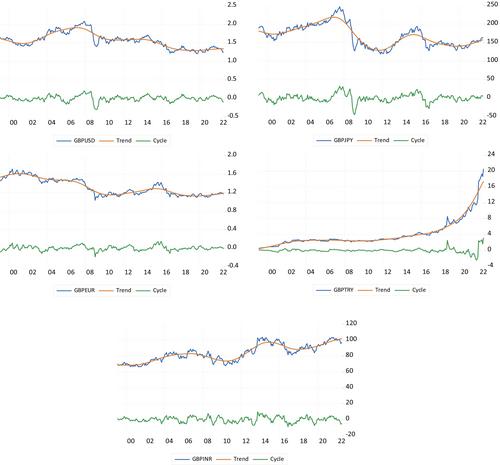

We develop a four-state regime-switching model for optimal foreign exchange (FX) hedging using forward contracts. The states correspond to four distinct market conditions, each defined by the direction and magnitude of deviation of the prevailing FX spot rate from its long-term trends. The model's performance is evaluated for five currencies against the pound sterling for various horizons. Our examination compares the hedging outcomes of the proposed model to those of other commonly employed hedging methods. The empirical results suggest that our model demonstrates the highest level of risk reduction for the US dollar, euro, Japanese yen and Turkish lira and the second-best performance for the Indian rupee. The risk reduction is significantly higher for lira compared with the other approaches, implying that the proposed model might be able to provide much more effective hedging for highly volatile currencies. The improved performance of the model can be attributed to the adjustability of the estimation horizon for the optimal hedge ratio based on the prevailing market conditions. This, in turn, allows it to better capture fat-tail properties that are frequently observed in FX returns. Our findings suggest that FX investors tend to use short-term memory during low market conditions (relative to trend) and long-term memory in high ones. The results would be also useful to build a better understanding of how investor behaviour depends on market conditions and mitigate the adverse behavioural implications of short-term memory, such as panic.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: