{"title":"Bank Culture and Bank Liquidity Creation","authors":"Loan Quynh Thi Nguyen, Luu Duc Toan Huynh","doi":"10.1111/corg.12580","DOIUrl":null,"url":null,"abstract":"<div>\n \n \n <section>\n \n <h3> Research Question/Issue</h3>\n \n <p>This study aimed to understand the impact of bank culture on liquidity creation by applying textual analysis to data from US bank holding companies.</p>\n </section>\n \n <section>\n \n <h3> Research Findings/Insights</h3>\n \n <p>The results indicated a substantial connection between bank culture and liquidity creation. Control and collaborative cultures negatively impacted liquidity creation, whereas a competing culture had a positive effect. The negative impacts were stronger in more diversified, experienced, and profitable banks and weaker in larger banks. In complete culture banks, liquidity creation decreased with increased experience and profitability but increased with size. The influence of culture on the different aspects of liquidity creation was similar across the board for overall liquidity generation.</p>\n </section>\n \n <section>\n \n <h3> Theoretical/Academic Implications</h3>\n \n <p>By introducing a new bank culture index, this study offers a unique contribution to the academic understanding of the interplay between organizational culture and financial performance, particularly liquidity creation.</p>\n </section>\n \n <section>\n \n <h3> Practitioner/Policy Implications</h3>\n \n <p>The insights from this study are valuable for bank managers and regulators as they highlight the aspects of bank culture that can be leveraged or adjusted to optimize liquidity creation, thereby informing strategies and policy decisions.</p>\n </section>\n </div>","PeriodicalId":48209,"journal":{"name":"Corporate Governance-An International Review","volume":"32 6","pages":"1087-1109"},"PeriodicalIF":5.5000,"publicationDate":"2024-05-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/corg.12580","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Corporate Governance-An International Review","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/corg.12580","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

Abstract

Research Question/Issue

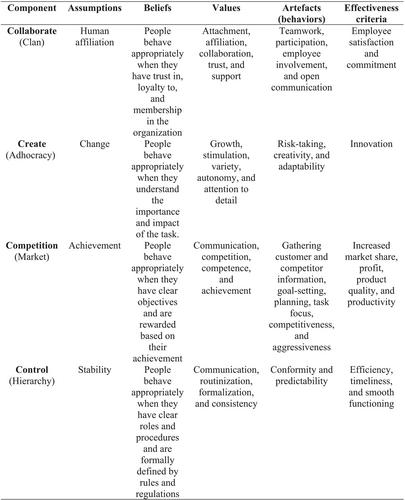

This study aimed to understand the impact of bank culture on liquidity creation by applying textual analysis to data from US bank holding companies.

Research Findings/Insights

The results indicated a substantial connection between bank culture and liquidity creation. Control and collaborative cultures negatively impacted liquidity creation, whereas a competing culture had a positive effect. The negative impacts were stronger in more diversified, experienced, and profitable banks and weaker in larger banks. In complete culture banks, liquidity creation decreased with increased experience and profitability but increased with size. The influence of culture on the different aspects of liquidity creation was similar across the board for overall liquidity generation.

Theoretical/Academic Implications

By introducing a new bank culture index, this study offers a unique contribution to the academic understanding of the interplay between organizational culture and financial performance, particularly liquidity creation.

Practitioner/Policy Implications

The insights from this study are valuable for bank managers and regulators as they highlight the aspects of bank culture that can be leveraged or adjusted to optimize liquidity creation, thereby informing strategies and policy decisions.

期刊介绍:

The mission of Corporate Governance: An International Review is to publish cutting-edge international business research on the phenomena of comparative corporate governance throughout the global economy. Our ultimate goal is a rigorous and relevant global theory of corporate governance. We define corporate governance broadly as the exercise of power over corporate entities so as to increase the value provided to the organization"s various stakeholders, as well as making those stakeholders accountable for acting responsibly with regard to the protection, generation, and distribution of wealth invested in the firm. Because of this broad conceptualization, a wide variety of academic disciplines can contribute to our understanding.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: