Long-term value versus short-term profits: When do index funds recall loaned shares for voting?

Abstract

Research Question/Issue

In this paper, we examine the effects of share lending or recall on proxy voting, with a particular focus on the role of index funds.

Research Findings/Insights

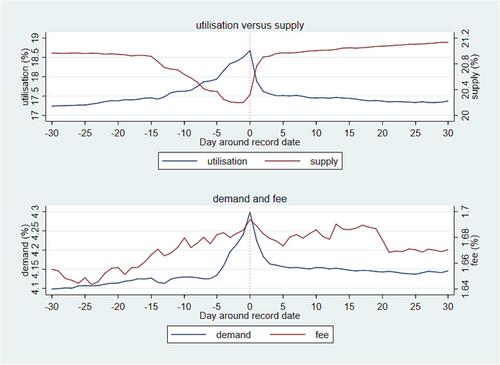

Our study reveals that higher index ownership in a firm is associated with an increased likelihood of share recall, particularly in the presence of higher institutional ownership, lower past return performance, smaller firm size, and when more shares are held by younger fund families with higher turnover ratios or higher management fees. Using the Russell 1000/2000 Index reconstitution as an exogenous shock, we establish a causal relationship between index ownership and share recall through instrumental variable (IV) analysis. Furthermore, we find a positive correlation between index ownership and share recall for proxy voting proposals related to compensation, director election, and those sponsored by management. In subsequent proxy votes, shareholder-sponsored proposals and environmental, social, and governance (ESG) proposals receive more support in firms with higher index ownership, especially when share recall is more prevalent. Our analysis does not provide evidence to support the conjecture that firms with higher index ownership are more vulnerable to empty voting issues.

Theoretical/Academic Implications

Our study enhances the understanding of how index funds recall shares during proxy voting and the impact of index ownership on voting outcomes. The findings support the practice of index funds recalling shares to actively engage in proxy voting, effectively addressing the conflict between short-term profit-seeking through securities lending and long-term governance responsibilities.

Practitioner/Policy Implications

We contribute to a better understanding of the role of index funds in corporate governance and shed light on the consequences of securities lending in proxy votes. These findings have important implications for investors, policymakers, and market participants in managing the potential conflicts arising from securities lending activities and promoting effective corporate governance practices.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: