{"title":"Robust mean-to-CVaR optimization under ambiguity in distributions means and covariance","authors":"Somayyeh Lotfi, Stavros A. Zenios","doi":"10.1007/s11846-023-00715-z","DOIUrl":null,"url":null,"abstract":"<p>We develop a robust mean-to-CVaR portfolio optimization model under interval ambiguity in returns means and covariance. The robust model satisfies second-order stochastic dominance consistency and is formulated as a semi-definite cone program. We use two controlled experiments to document the sensitivity of the optimal allocations to the ambiguity when asset correlation varies, and to the ambiguity intervals. We find that means ambiguity has a higher impact than covariance ambiguity. We apply the model to US equities data to corroborate works showing that ambiguity in mean returns induces a home bias; it can explain the puzzle in a two-country setting but not with three countries. We further establish that covariance ambiguity also induces bias, but with lower impact that can not explain the puzzle. Our results suggest what is needed for the ambiguity channel to provide a full explanation of the puzzle. The findings are robust to alternative model specifications and outliers.</p>","PeriodicalId":20992,"journal":{"name":"Review of Managerial Science","volume":"20 1","pages":""},"PeriodicalIF":9.6000,"publicationDate":"2024-01-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Managerial Science","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11846-023-00715-z","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MANAGEMENT","Score":null,"Total":0}

引用次数: 0

Abstract

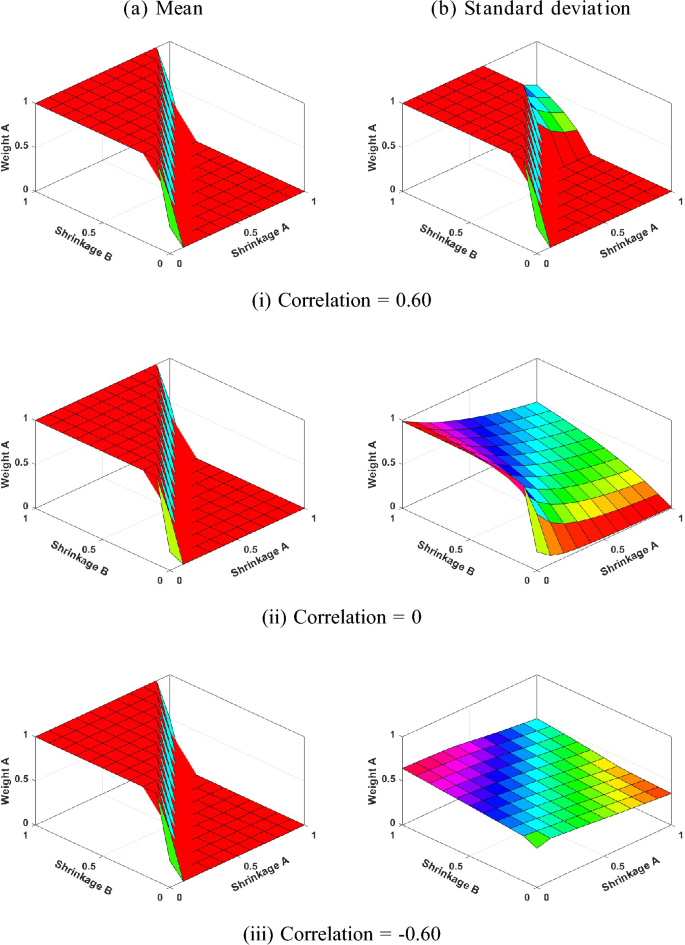

We develop a robust mean-to-CVaR portfolio optimization model under interval ambiguity in returns means and covariance. The robust model satisfies second-order stochastic dominance consistency and is formulated as a semi-definite cone program. We use two controlled experiments to document the sensitivity of the optimal allocations to the ambiguity when asset correlation varies, and to the ambiguity intervals. We find that means ambiguity has a higher impact than covariance ambiguity. We apply the model to US equities data to corroborate works showing that ambiguity in mean returns induces a home bias; it can explain the puzzle in a two-country setting but not with three countries. We further establish that covariance ambiguity also induces bias, but with lower impact that can not explain the puzzle. Our results suggest what is needed for the ambiguity channel to provide a full explanation of the puzzle. The findings are robust to alternative model specifications and outliers.

期刊介绍:

Review of Managerial Science (RMS) provides a forum for innovative research from all scientific areas of business administration. The journal publishes original research of high quality and is open to various methodological approaches (analytical modeling, empirical research, experimental work, methodological reasoning etc.). The scope of RMS encompasses – but is not limited to – accounting, auditing, banking, business strategy, corporate governance, entrepreneurship, financial structure and capital markets, health economics, human resources management, information systems, innovation management, insurance, marketing, organization, production and logistics, risk management and taxation. RMS also encourages the submission of papers combining ideas and/or approaches from different areas in an innovative way. Review papers presenting the state of the art of a research area and pointing out new directions for further research are also welcome. The scientific standards of RMS are guaranteed by a rigorous, double-blind peer review process with ad hoc referees and the journal´s internationally composed editorial board.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: