{"title":"The effect of CEO-to-worker pay disparities on CEO compensation: The mediating role of shareholder say on pay votes","authors":"Etienne Develay, Yan Wang, Stephanie Giamporcaro","doi":"10.1002/ijfe.2866","DOIUrl":null,"url":null,"abstract":"<p>In response to large pay disparities caused by rising CEO compensation and stagnant employee pay, US financial regulators have taken several initiatives to mobilise shareholders. However, the ability of these initiatives to enhance shareholder engagement and reduce excessive CEO compensation has been questioned. Using a large sample of 1594 non-financial firms from the Russell 3000 index over 2013–2019, we disentangle the complex role that shareholder engagement towards CEO-to-worker pay disparities plays on CEO compensation. We find that higher CEO-to-worker pay disparities increase shareholder dissent say on pay votes and that, paradoxically, shareholder dissent say on pay votes increase CEO compensation. Furthermore, we provide evidence that shareholder engagement mediates the relationship between CEO-to-worker pay disparities and CEO compensation through their say on pay votes. Our findings are consistent with the relative deprivation theory as shareholders react to large pay disparities to avoid the negative consequences of a feeling of deprivation on employees. They are also in line with the agency theory, as shareholder reactions to large CEO-to-worker pay disparities trigger reactions from the remuneration committee to better align CEO pay with their interests. Overall, our findings support the existence of a shareholder engagement channel driven by social comparison mechanisms and agency responses. This study has important implications for regulators by unpacking the usefulness of these regulatory initiatives to shareholders and also documenting their unintended consequences on CEO compensation.</p>","PeriodicalId":47461,"journal":{"name":"International Journal of Finance & Economics","volume":"29 4","pages":"3933-3950"},"PeriodicalIF":2.8000,"publicationDate":"2023-07-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ijfe.2866","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Finance & Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ijfe.2866","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

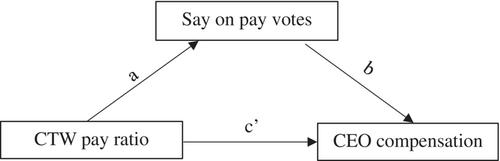

Abstract

In response to large pay disparities caused by rising CEO compensation and stagnant employee pay, US financial regulators have taken several initiatives to mobilise shareholders. However, the ability of these initiatives to enhance shareholder engagement and reduce excessive CEO compensation has been questioned. Using a large sample of 1594 non-financial firms from the Russell 3000 index over 2013–2019, we disentangle the complex role that shareholder engagement towards CEO-to-worker pay disparities plays on CEO compensation. We find that higher CEO-to-worker pay disparities increase shareholder dissent say on pay votes and that, paradoxically, shareholder dissent say on pay votes increase CEO compensation. Furthermore, we provide evidence that shareholder engagement mediates the relationship between CEO-to-worker pay disparities and CEO compensation through their say on pay votes. Our findings are consistent with the relative deprivation theory as shareholders react to large pay disparities to avoid the negative consequences of a feeling of deprivation on employees. They are also in line with the agency theory, as shareholder reactions to large CEO-to-worker pay disparities trigger reactions from the remuneration committee to better align CEO pay with their interests. Overall, our findings support the existence of a shareholder engagement channel driven by social comparison mechanisms and agency responses. This study has important implications for regulators by unpacking the usefulness of these regulatory initiatives to shareholders and also documenting their unintended consequences on CEO compensation.

针对首席执行官薪酬上涨而员工薪酬停滞不前所造成的巨大薪酬差距,美国金融监管机构采取了多项举措来调动股东的积极性。然而,这些举措能否提高股东参与度并减少 CEO 薪酬过高的问题一直备受质疑。我们利用罗素 3000 指数 2013-2019 年间 1594 家非金融企业的大量样本,分析了股东参与 CEO 与员工薪酬差距对 CEO 薪酬的复杂影响。我们发现,CEO 与员工薪酬差距越大,股东对薪酬投票的异议就越多,而矛盾的是,股东对薪酬投票的异议会增加 CEO 的薪酬。此外,我们还提供了证据,证明股东参与通过其对薪酬的 "说 "的投票,在 CEO 与员工薪酬差距和 CEO 薪酬之间起到了中介作用。我们的研究结果与相对剥夺理论是一致的,因为股东会对巨大的薪酬差距做出反应,以避免员工产生被剥夺感的负面影响。这些发现也符合代理理论,因为股东对首席执行官与员工之间巨大薪酬差距的反应会引发薪酬委员会的反应,使首席执行官的薪酬与他们的利益更加一致。总之,我们的研究结果支持了由社会比较机制和代理反应驱动的股东参与渠道的存在。本研究揭示了这些监管举措对股东的益处,同时也记录了这些举措对首席执行官薪酬的意外后果,因此对监管机构具有重要意义。

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: