Demetrio Lacava, Giampiero M. Gallo, Edoardo Otranto

{"title":"非常规政策对股市波动的影响:MAP方法","authors":"Demetrio Lacava, Giampiero M. Gallo, Edoardo Otranto","doi":"10.1111/rssc.12574","DOIUrl":null,"url":null,"abstract":"<p>Taking the European Central Bank unconventional policies as a reference, we suggest a class of multiplicative error models (MEMs) tailored to analyse the impact such policies have on stock market volatility. The new set of models, called MEM with asymmetry and policy effects, keeps the base volatility dynamics separate from a component reproducing policy effects, with an increase in volatility on announcement days and a decrease unfolding implementation effects. When applied to four Eurozone markets, a model confidence set approach finds a significant improvement of the forecasting power of the proxy after the expanded asset purchase programme implementation. A multi-step ahead forecasting exercise estimates the duration of the effect; by shocking the policy variable, we are able to quantify the reduction in volatility which is more marked for debt-troubled countries.</p>","PeriodicalId":1,"journal":{"name":"Accounts of Chemical Research","volume":null,"pages":null},"PeriodicalIF":16.4000,"publicationDate":"2022-06-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://rss.onlinelibrary.wiley.com/doi/epdf/10.1111/rssc.12574","citationCount":"0","resultStr":"{\"title\":\"Unconventional policies effects on stock market volatility: The MAP approach\",\"authors\":\"Demetrio Lacava, Giampiero M. Gallo, Edoardo Otranto\",\"doi\":\"10.1111/rssc.12574\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Taking the European Central Bank unconventional policies as a reference, we suggest a class of multiplicative error models (MEMs) tailored to analyse the impact such policies have on stock market volatility. The new set of models, called MEM with asymmetry and policy effects, keeps the base volatility dynamics separate from a component reproducing policy effects, with an increase in volatility on announcement days and a decrease unfolding implementation effects. When applied to four Eurozone markets, a model confidence set approach finds a significant improvement of the forecasting power of the proxy after the expanded asset purchase programme implementation. A multi-step ahead forecasting exercise estimates the duration of the effect; by shocking the policy variable, we are able to quantify the reduction in volatility which is more marked for debt-troubled countries.</p>\",\"PeriodicalId\":1,\"journal\":{\"name\":\"Accounts of Chemical Research\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":16.4000,\"publicationDate\":\"2022-06-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://rss.onlinelibrary.wiley.com/doi/epdf/10.1111/rssc.12574\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Accounts of Chemical Research\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/rssc.12574\",\"RegionNum\":1,\"RegionCategory\":\"化学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"CHEMISTRY, MULTIDISCIPLINARY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Accounts of Chemical Research","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/rssc.12574","RegionNum":1,"RegionCategory":"化学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"CHEMISTRY, MULTIDISCIPLINARY","Score":null,"Total":0}

Unconventional policies effects on stock market volatility: The MAP approach

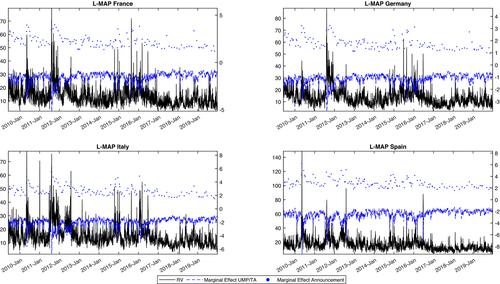

Taking the European Central Bank unconventional policies as a reference, we suggest a class of multiplicative error models (MEMs) tailored to analyse the impact such policies have on stock market volatility. The new set of models, called MEM with asymmetry and policy effects, keeps the base volatility dynamics separate from a component reproducing policy effects, with an increase in volatility on announcement days and a decrease unfolding implementation effects. When applied to four Eurozone markets, a model confidence set approach finds a significant improvement of the forecasting power of the proxy after the expanded asset purchase programme implementation. A multi-step ahead forecasting exercise estimates the duration of the effect; by shocking the policy variable, we are able to quantify the reduction in volatility which is more marked for debt-troubled countries.

期刊介绍:

Accounts of Chemical Research presents short, concise and critical articles offering easy-to-read overviews of basic research and applications in all areas of chemistry and biochemistry. These short reviews focus on research from the author’s own laboratory and are designed to teach the reader about a research project. In addition, Accounts of Chemical Research publishes commentaries that give an informed opinion on a current research problem. Special Issues online are devoted to a single topic of unusual activity and significance.

Accounts of Chemical Research replaces the traditional article abstract with an article "Conspectus." These entries synopsize the research affording the reader a closer look at the content and significance of an article. Through this provision of a more detailed description of the article contents, the Conspectus enhances the article's discoverability by search engines and the exposure for the research.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: