{"title":"全球石油市场的时频依赖性和连通性:来自高阶矩视角的新证据","authors":"Jinxin Cui , Aktham Maghyereh","doi":"10.1016/j.jcomm.2023.100323","DOIUrl":null,"url":null,"abstract":"<div><p>Investigating the dependence and connectedness among global oil markets is of great significance for cross-market investors and regulators. However, most of the existing studies are confined to lower-order moments and the time domain. This paper is the first to examine the time-frequency dependence and connectedness among global oil markets from the higher-order moment perspective by applying the wavelet coherence method and the newly proposed time-varying parameter vector autoregression-based frequency connectedness approach. The empirical results demonstrate that higher-order moment dependence among oil markets is weaker than return and volatility dependence. In general, Dubai, Minas, and Tapis oil exhibit relatively higher wavelet coherence with Daqing oil at all moments. The lead-lag relationships are heterogeneous during most sample intervals. The total return and volatility connectedness indices are higher than the skewness and kurtosis. The return connectedness mainly occurs in the short term (1–5 days) whereas the volatility, skewness, and kurtosis connectedness occur in the long run (22-Inf days). West Texas Intermediate oil dominates the return, volatility, and skewness connectedness network while Dubai oil dominates the kurtosis connectedness network. Furthermore, the dynamic total, net, and net-pairwise connectedness indices are all time-varying and event-dependent with the higher-order moment connectedness illustrating more volatile features. Several practical implications are provided for various market agents.</p></div>","PeriodicalId":45111,"journal":{"name":"Journal of Commodity Markets","volume":"30 ","pages":"Article 100323"},"PeriodicalIF":3.7000,"publicationDate":"2023-06-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"4","resultStr":"{\"title\":\"Time-frequency dependence and connectedness among global oil markets: Fresh evidence from higher-order moment perspective\",\"authors\":\"Jinxin Cui , Aktham Maghyereh\",\"doi\":\"10.1016/j.jcomm.2023.100323\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Investigating the dependence and connectedness among global oil markets is of great significance for cross-market investors and regulators. However, most of the existing studies are confined to lower-order moments and the time domain. This paper is the first to examine the time-frequency dependence and connectedness among global oil markets from the higher-order moment perspective by applying the wavelet coherence method and the newly proposed time-varying parameter vector autoregression-based frequency connectedness approach. The empirical results demonstrate that higher-order moment dependence among oil markets is weaker than return and volatility dependence. In general, Dubai, Minas, and Tapis oil exhibit relatively higher wavelet coherence with Daqing oil at all moments. The lead-lag relationships are heterogeneous during most sample intervals. The total return and volatility connectedness indices are higher than the skewness and kurtosis. The return connectedness mainly occurs in the short term (1–5 days) whereas the volatility, skewness, and kurtosis connectedness occur in the long run (22-Inf days). West Texas Intermediate oil dominates the return, volatility, and skewness connectedness network while Dubai oil dominates the kurtosis connectedness network. Furthermore, the dynamic total, net, and net-pairwise connectedness indices are all time-varying and event-dependent with the higher-order moment connectedness illustrating more volatile features. Several practical implications are provided for various market agents.</p></div>\",\"PeriodicalId\":45111,\"journal\":{\"name\":\"Journal of Commodity Markets\",\"volume\":\"30 \",\"pages\":\"Article 100323\"},\"PeriodicalIF\":3.7000,\"publicationDate\":\"2023-06-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"4\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Commodity Markets\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S2405851323000132\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Commodity Markets","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S2405851323000132","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Time-frequency dependence and connectedness among global oil markets: Fresh evidence from higher-order moment perspective

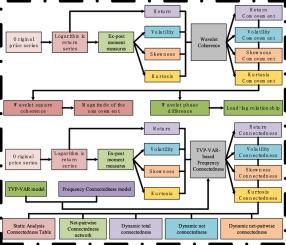

Investigating the dependence and connectedness among global oil markets is of great significance for cross-market investors and regulators. However, most of the existing studies are confined to lower-order moments and the time domain. This paper is the first to examine the time-frequency dependence and connectedness among global oil markets from the higher-order moment perspective by applying the wavelet coherence method and the newly proposed time-varying parameter vector autoregression-based frequency connectedness approach. The empirical results demonstrate that higher-order moment dependence among oil markets is weaker than return and volatility dependence. In general, Dubai, Minas, and Tapis oil exhibit relatively higher wavelet coherence with Daqing oil at all moments. The lead-lag relationships are heterogeneous during most sample intervals. The total return and volatility connectedness indices are higher than the skewness and kurtosis. The return connectedness mainly occurs in the short term (1–5 days) whereas the volatility, skewness, and kurtosis connectedness occur in the long run (22-Inf days). West Texas Intermediate oil dominates the return, volatility, and skewness connectedness network while Dubai oil dominates the kurtosis connectedness network. Furthermore, the dynamic total, net, and net-pairwise connectedness indices are all time-varying and event-dependent with the higher-order moment connectedness illustrating more volatile features. Several practical implications are provided for various market agents.

期刊介绍:

The purpose of the journal is also to stimulate international dialog among academics, industry participants, traders, investors, and policymakers with mutual interests in commodity markets. The mandate for the journal is to present ongoing work within commodity economics and finance. Topics can be related to financialization of commodity markets; pricing, hedging, and risk analysis of commodity derivatives; risk premia in commodity markets; real option analysis for commodity project investment and production; portfolio allocation including commodities; forecasting in commodity markets; corporate finance for commodity-exposed corporations; econometric/statistical analysis of commodity markets; organization of commodity markets; regulation of commodity markets; local and global commodity trading; and commodity supply chains. Commodity markets in this context are energy markets (including renewables), metal markets, mineral markets, agricultural markets, livestock and fish markets, markets for weather derivatives, emission markets, shipping markets, water, and related markets. This interdisciplinary and trans-disciplinary journal will cover all commodity markets and is thus relevant for a broad audience. Commodity markets are not only of academic interest but also highly relevant for many practitioners, including asset managers, industrial managers, investment bankers, risk managers, and also policymakers in governments, central banks, and supranational institutions.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: