{"title":"在有控股股东的公司中,董事会的独立性是否重要?","authors":"Jay Dahya, Orlin Dimitrov, John J. McConnell","doi":"10.1111/jacf.12543","DOIUrl":null,"url":null,"abstract":"<p>Studies have reported valuation discounts for publicly traded companies based in countries that provide weak legal protection for minority shareholders.1 Such discounts are often attributed to the ability of controlling shareholders to extract “private benefits” that come at the expense of minority shareholders. Without sufficient legal deterrents, controlling shareholders have both the incentive and the ability to transfer corporate resources to themselves for personal consumption or gain. These transfers take a number of forms, including related-party “tunneling” transactions as well as corporate perks and, in some cases, outright theft.</p><p>But under certain circumstances—notably, when their companies want to raise capital by selling shares—the controlling shareholders may face a stronger incentive to reduce this value discount by providing credible commitments to outside investors to forgo this diversion of corporate resources. Various commitment mechanisms have been proposed in the literature, including cross-listing on U.S. exchanges as well as general improvements in overall corporate governance systems.2 But another possible solution is more effective oversight of controlling shareholders by corporate boards.</p><p>We recently published a study that investigated the effects of appointing more independent directors on the value discounts of companies controlled by a dominant shareholder.3 Using biographical data on nearly 8000 directors of 799 closely held companies in 22 countries, we found a significant positive correlation between corporate value and the fraction of the board made up of independent directors. Moreover, we found this relation to be especially pronounced in countries that afford investors weak legal protection—countries where controlling shareholders presumably have then greatest opportunity to increase corporate values by submitting to greater oversight.</p><p>Thus, the findings of our study are consistent with the possibility that the appointment of directors with no ties to the controlling shareholder can be a powerful mechanism to reduce the threat of resource diversion and transfer of value from minority shareholders. But how reliable is this interpretation, given that the same controlling shareholders that have the power to appoint the board members also have the power—perhaps if they do too good a job—to dismiss them?</p><p>To address this issue, we performed several additional tests designed to detect the ability of independent directors to monitor the actions of the controlling shareholder. One such test revealed that 71% of independent directors in our sample sat on multiple corporate boards. We reasoned that multiple appointments are more likely to be a proxy for “reputational capital,” and that directors with multiple appointments should be less willing to jeopardize those reputations by proving to be ineffective monitors. As a second check on whether independent directors help reduce the threat of transfers of corporate resources, we also found that the frequency of related-party transactions was significantly lower in companies with larger fractions of independent directors, and that this reduced frequency was associated with higher corporate values.</p><p>A third set of tests investigated the possibility that an increase in the value of corporate shares would be most beneficial to controlling shareholders that plan either to issue equity on behalf of the firm or to sell equity on personal account. The tradeoff faced by such shareholders in these circumstances is between a higher value for their shares and reduced private control benefits. In other words, controlling shareholders are likely to appoint independent directors when their expected gains from higher share values outweigh their sacrifice of private benefits. Consistent with this argument, we found that the companies in our sample that issued equity had larger fractions of independent directors.</p><p>In the pages that follow, we explore each of the questions raised here in greater depth, report the relevant results of our recent study, and present representative case studies.</p><p>Because the board is appointed and dismissed by the controlling shareholder, the question arises as to whether such directors can perform their duties effectively. After all, directors appointed by controlling shareholders may be subject to various pressures, including the threat of dismissal at any time, for opposing the interests of those shareholders.</p><p>We believe there are three necessary conditions for boards of directors to be effective monitors of controlling shareholders. First, independent directors must be able to raise the cost to the controlling shareholder of diverting resources for personal benefit. It is worth noting that independent directors do not have to monitor the controlling shareholder's actions perfectly. To the extent they make it more difficult and costly for the controlling shareholder to extract private benefits, independent directors can help preserve value for minority shareholders.</p><p>Second, independent directors must have the incentive to monitor the controlling shareholder. As Eugene Fama and Michael Jensen argued in a classic corporate governance paper in the early 1980s, this incentive is provided by the mere existence of a well-functioning market for the services of independent directors.4 Thanks to such a market, independent directors have “human” or “reputational” capital at stake that can be lost “when internal control breaks down” and the companies under their oversight perform badly. To assess the reputational capital of independent directors, we gathered information on the number of directorships held by such directors. Finding that more than 70% of the over 4000 independent directors in our sample served on multiple boards, we concluded that there is a robust market for the services of independent directors.</p><p>But having the incentive to monitor may not be enough. Independent directors must also have the power to perform their duties well. In examining the extent to which this condition for effective monitoring is likely to hold, we started by noting the finding of previous research that, in 20 of the 22 countries in our sample, directors have a legal responsibility to curb self-dealing actions by the controlling shareholder, and can be held legally accountable for failing to do so.5 This mandate gives independent directors the legal authority to act on behalf of minority shareholders. Along with such authority, such directors also routinely seek and obtain assurances from the controlling shareholders that they will have the freedom and power to perform their duties effectively.</p><p>We gathered data on share ownership and boards of directors for companies from 22 countries as of the end of 2002. These are predominantly countries with well-developed economies, for whose companies we were able to locate data on both share ownership and board composition. Our initial sample included the 70 largest publicly traded companies based on market capitalization from each country.</p><p>Before we could determine director affiliation, our first task was to identify companies with a controlling shareholder. We defined a controlling shareholder as the largest single owner of voting rights in any company where that owner controlled at least 10% of the firm's votes.6 Figure 1 provides information on the identity of the controlling shareholder by country. Of all controlling shareholders in our sample, 347 were individuals or families, 226 were privately held operating or holding companies, 101 were privately held financial institutions, and 108 were governments.</p><p>The last 20 years have seen the issuance of corporate governance codes, mandates, recommendations, and listing requirements in more than 70 countries worldwide. The vast majority of them place significant emphasis on director independence.7 We used those publications as a guide in arriving at our own definition of what constitutes an independent director. We considered directors to be affiliated with the controlling shareholder (i.e., not independent) if they (1) had the same family name as the controlling shareholder, (2) were employees of the firm, (3) were employees of any company or subsidiary of any company that was positioned “above” the sample firm in the ownership tree, (4) were employees of another firm in which the controlling shareholder had at least a 10% ownership position regardless of whether the second firm was in the ownership tree, (5) were politicians or employees of a government agency when the controlling shareholder was a government, or (6) in cases of a foreign controlling shareholder, were employed by a company domiciled in the same country as the controlling shareholder. Directors who were not identified as being affiliated with the controlling shareholder in any of these ways were designated as “independent.”8</p><p>Figure 2 provides information on directors who are affiliated and unaffiliated with (i.e., independent of) the controlling shareholder. An inspection of this chart reveals that the fraction of independent directors varies significantly across countries, with the highest fraction in the U.S. and the lowest in Japan.</p><p>Because the share of voting rights held by controlling shareholders often exceeds their proportionate claims on cash flows,9 we also gathered information about the voting and ownership rights of the controlling shareholders. A large disparity between voting and cash-flow rights amplifies the incentives of controlling shareholders to exploit minority shareholders.10 For each company with a pyramidal ownership structure in our sample, we determined the fraction of cash-flow rights owned by the controlling shareholder by multiplying his fraction of cash-flow rights held in a sample firm by the fraction of shares owned in each firm along the control chain in the ownership tree. For example, if individual X owned 10% of the shares in company A, which in turn owned 20% in company B, and there were no other large shareholders in B, we considered X to be the controlling shareholder in B with 20% of the voting and 2% (20% times 10%) of the cash-flow rights.</p><p>While it is customary in U.S.-based studies to compute Tobin's Q as a measure of corporate value, international datasets generally lack the depth needed to calculate this measure accurately. As the primary dependent variable in our study, we accordingly used the following variation of Tobin's Q: the market value of equity plus the book value of liabilities (i.e., book assets less book equity) divided by the book value of assets. For each of our sample companies, we calculated and averaged this market-to-book ratio as of the end of 2002 and 2003. To limit the effect of outliers on our findings, we trimmed the top and bottom one percent of the sample ranked by our Tobin's Q proxy, which left a final sample of 782 firms.</p><p>In Table 1, we report the number of firms and other important characteristics of our sample classified by individual countries. Because we extracted only the closely held companies from the 70 largest firms in each country, the number of companies differs across countries. For example, the U.S. and Japan are considerably underrepresented because, among the 70 largest U.S. and Japanese companies, only 16 and 10 firms, respectively, had controlling shareholders. In Italy, by contrast, the number of closely held companies was 56, the highest of all countries in the sample.</p><p>Also reported in Table 1 is our measure of investor protection for each country. We refer to this measure as “LEGAL.” The quality of legal protection afforded to minority shareholders can be thought of as comprising two elements: (1) the statutory rules and provisions (also called de jure protection) and (2) the degree of enforcement of these statutes (de facto protection). LEGAL is the product of the two indices that capture de jure and de facto protection. These are the “Anti-director rights” index, which ranges from 0 to 6, and the “Law and Order” enforcement index from the International Country Risk Guide, which we have rescaled to range from 0 to 10.11</p><p>As can be seen in Table 1, despite our focus on mostly developed countries, we observed significant variation in the degree of protection afforded to minority shareholders. The variable LEGAL ranged from a low of 3.3 in Mexico to a high of 50 in Canada, the U.S., and the U.K. Also worth noting in Table 1 is the significant variation in ownership, board composition, and corporate value (Tobin's Q), both among country averages and among different companies in the same country. In terms of cross-country variation, the percentage of independent directors was highest in the U.S. (75%) and lowest in Japan (38%). As for within-country variation, the minimum and maximum percentages of independent directors in a firm were 45% and 93% in the U.S., and 0.0% and 100% in France, Germany, and Brazil.</p><p>In our first-pass analysis, we compared our version of Tobin's Q against the LEGAL index. For this comparison, countries were classified into three groups with the eight countries having LEGAL ≥ 30 in group 1, the five countries with 30 > LEGAL ≥ 20 in group 2, and the nine countries with LEGAL < 20 in group 3. We found that Qs varied systematically across these three different levels of legal shareholder protection, with higher protection associated with higher Qs: the mean Q of 1.58 for group 1 was significantly greater than the meanQ of 1.38 in group 3 (<i>p</i>-value = 0.01). This analysis served to confirm the generally accepted view that the stronger country-level legal shareholder protection is associated with higher firm values. A more interesting finding emerged when we split the entire sample of companies into three groups according to the percentage of independent directors. The mean and median Qs increase monotonically with the increase in the percentage of independent directors and the differences in means and medians between groups 1 and 3 were statistically significant (<i>p</i>-values < 0.01). The mean Tobin's Q was 1.32 for companies where less than one third of the board was independent directors and 1.57 for those with more than two-thirds.</p><p>To add rigor to our descriptive statistics, we then estimated a series of regressions designed to show the effect of the fraction of independent directors on Tobin's Q.16</p><p>The key coefficients from our regression tests are reproduced in Table 2. Column 1 presents the results of what can be thought of as our “base case” regression. It serves to compare our results to results from previous studies. However, this regression excludes the primary independent variable of interest, the fraction of independent directors on the board (“INDDIR%”). Consistent with prior studies, the nationwide coefficient of LEGAL was positive (and significant with a <i>p</i>-value = 0.01), suggesting that stronger shareholder protection increases firm value. There was also some indication that a higher fraction of cash-flow rights owned by the controlling shareholder enhances corporate value (though the corresponding coefficient is significant at the 10% level only). In subsequent regressions, moreover, these base case results remained essentially unchanged. All in all, in companies with a controlling shareholder, firm value was shown to be positively correlated with the country-level of legal shareholder protection and with the fraction of cash-flow rights held by the controlling shareholder.17</p><p>Having estimated the base-case regression, we then added the key variable of interest, INDDIR%—again, the fraction of independent directors—to the base case regression. As reported in column 2 of the table, the coefficient on INDDIR% in this column was positive and statistically significant (<i>p</i>-value = 0.01). This coefficient could be interpreted as saying that, in the case of a representative company in our sample, a 10% increase in the fraction of a company's independent directors (in other words, for each additional independent director on a board with ten members) is generally associated with a 4% increase in its Tobin's Q ratio. And thus, for each additional $1 billion of assets (in terms of book value), each additional independent director translates into an additional $40 million of value.</p><p>Next, to test the limits of the “linearity” of this relationship, we replaced INDIRR% with a natural log and nonlinear specification of INDDIR%. In that regression, the coefficient (reported in column 3) was not only positive and statistically significant (<i>p</i>-value = 0.02), but the adjusted R<sup>2</sup> increased relative to the linear specification. The better “fit” associated with this logarithmic specification of INDDIR% can be interpreted as saying that although firm value increases with the fraction of independent directors, it increases at a decreasing rate as that fraction increases (and thus adding the fifth independent director adds less value than the third or the fourth).</p><p>Given our assumption that controlling shareholders are more likely to appoint independent directors when their companies issue equity, we set out to examine the relation between the frequency of seasoned equity offerings (SEOs) and board composition. We found that, during the period 2002–2004, 198, or about one in four, of our 799 sample companies undertook one or more SEOs that raised at least $10 million.</p><p>As a first pass, we identified those sample firms that had issued equity and those that had not, and calculated the mean percentage of independent directors, INDDIR%, for the two groups. The average INDDIR% for firms that had issued equity was 56.1%, while the average INDDIR% for non-issuing firms was 50.2% (The difference in means between the two groups was statistically significant with a <i>p</i>-value < 0.01).</p><p>Next we undertook a regression analysis intended to investigate the extent to which SEOs have systematic effects on board composition. The dependent variable in this model was INDDIR% and the key independent variable was a 1/0 indicator of an SEO (not including rights offerings).22 As reported in the first column of Table 3, the coefficient of SEO was positive and statistically significant (at the 0.01 level or less),23 supporting our conjecture that the issuance of outside equity is an important determinant of board composition in companies with controlling shareholders.</p><p>One of the primary means by which controlling shareholders are alleged to take advantage of minority shareholders is through transactions with related companies that transfer corporate resources and value to firms in which the controlling shareholder has a majority ownership position. Such transactions are frequently referred to as tunneling.24</p><p>Although such transactions cannot be directly observed,25 we assumed that much of this activity is accomplished through related party transactions (RPTs). Strong boards have the potential to limit such wealth transfers by monitoring the terms of RPTs and preventing those that are clearly against the interests of minority holders. Following this line of reasoning, we hypothesized that RPTs should occur less frequently in firms with more independent directors; and when RPTs do occur, they should have more advantageous terms for the minority shareholders than in firms with mostly affiliated directors. Though we have no way of knowing the terms of RPTs, we can observe their frequency because each of our sample countries requires disclosure of RPTs in periodic filings.</p><p>To classify a transaction as a RPT, we borrowed a classification scheme adopted by prior research studies.26 We considered five types of dealings to be RPTs: (1) acquisition by the sample firm of assets and/or stock from the controlling shareholder or from any other firm affiliated with the controlling shareholder; (2) asset sales by the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; (3) asset swaps between the sample firm and the controlling shareholder or any other firm-affiliated with the controlling shareholder; (4) debt and/or loan relief from the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; and (5) sales and/or purchases of merchandise from and/or to the sample firm from and/or to the controlling shareholder or any other firm affiliated with the controlling shareholder.27 A search of filings for RPTs yielded information on RPTs conducted by 148 sample firms in 2002.</p><p>For those of our sample companies that reported RPTs, the mean percentage of independent directors (INDDIR%) was 49.4%, as compared to 53.2% for those companies that did not (The difference in means was 3.8%, with a <i>p</i>-value of 0.14; the difference in median INDDIR% values between the groups revealed a difference of 7.1% with a <i>p</i>-value of 0.03).</p><p>To control for other factors that could affect the likelihood of RPTs, we estimated a logit regression in which the dependent variable was a 1/0 indicator for the occurrence of an RPT and the key independent variable was ln (INDDIR%). As reported in Table 4, the coefficient of ln (INDDIR%) was negative and statistically significant, implying that a higher fraction of independent directors on the board reduces the likelihood of RPTs. For a typical firm in our sample, holding everything else at a fixed value, increasing the fraction of independent directors from 40% to 60% will reduce the odds of observing an RPT by 19%, and increasing the fraction of independent directors from 40% to 80% will reduce those odds by approximately 30%.</p><p>To supplement our logit analysis on RPTs and ln (INDIRR%) we estimated a country random effects regression in which the dependent variable was the average Tobin's Q for 2002–2003 and the key independent variable was RPT.</p><p>The other independent variables were the same as in the second column of Table 2 except that we excluded the two board variables ln (INDDIR%) and ln (board size). In this regression, presented in column 2 of Table 4, the coefficient of RPT is negative (with a <i>p</i>-value of 0.06), while the coefficient of LEGAL is positive (with a <i>p</i>-value of 0.04). Thus RPTs appear to have a negative effect on corporate value, even after controlling for the legal environment.</p><p>In sum, the results of our regression analyses are consistent with the interpretation that independent directors can reduce the threat of wealth transfers to the controlling shareholder by limiting disadvantageous RPTs.</p><p>Our findings indicate that controlling shareholders intent on increasing the value of their companies can do so by appointing independent directors. For example, our results can be interpreted as saying that, in the case of a representative company in a country with an average level of protection for minority shareholders, a 10% increase in the fraction of a company's independent directors is associated with a 4% increase in its Tobin's Q ratio. But, as our findings also suggest, such effects on value are expected to be considerably larger in countries with limited minority shareholder rights. For example, by increasing the percentage of unaffiliated directors from 10% to 90%, a controlling shareholder of a company in a country such as Mexico can expect to see the Q ratio of his company increase by almost 15% (from 1.41 to 1.60). Nevertheless, that percentage increase in value would not be enough to make up the full loss in value associated with weak country-level shareholder legal protection. Our analysis suggests that the same company, if based say in the U.K., would be expected to have a Q ratio of about 1.90 even with a board composed of no more than 10% independent directors.</p><p>But what about controlling shareholders of companies in a country with moderate legal protection? Can they benefit from appointing a strong board? Our analysis suggests that for a controlling shareholder in a country such as India, with a LEGAL index of 20, increasing the percentage of independent directors from 10% to 90% will raise the firm's Q from 1.58 to 1.80.</p><p>At the same time, our findings also suggest that this increase in Q is equivalent to the expected effect of raising a country's legal protection score from 20 to 40 (the score in Australia). Thus, in countries like India, appointing independent boards can be an effective, though probably not a complete, substitute for strengthening a country's legal system.</p><p>In sum, independent directors can make a big difference, particularly in countries where legal protection for shareholders is weak.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"35 1","pages":"72-82"},"PeriodicalIF":1.4000,"publicationDate":"2023-04-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12543","citationCount":"0","resultStr":"{\"title\":\"Does board independence matter in companies with a controlling shareholder?\",\"authors\":\"Jay Dahya, Orlin Dimitrov, John J. McConnell\",\"doi\":\"10.1111/jacf.12543\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Studies have reported valuation discounts for publicly traded companies based in countries that provide weak legal protection for minority shareholders.1 Such discounts are often attributed to the ability of controlling shareholders to extract “private benefits” that come at the expense of minority shareholders. Without sufficient legal deterrents, controlling shareholders have both the incentive and the ability to transfer corporate resources to themselves for personal consumption or gain. These transfers take a number of forms, including related-party “tunneling” transactions as well as corporate perks and, in some cases, outright theft.</p><p>But under certain circumstances—notably, when their companies want to raise capital by selling shares—the controlling shareholders may face a stronger incentive to reduce this value discount by providing credible commitments to outside investors to forgo this diversion of corporate resources. Various commitment mechanisms have been proposed in the literature, including cross-listing on U.S. exchanges as well as general improvements in overall corporate governance systems.2 But another possible solution is more effective oversight of controlling shareholders by corporate boards.</p><p>We recently published a study that investigated the effects of appointing more independent directors on the value discounts of companies controlled by a dominant shareholder.3 Using biographical data on nearly 8000 directors of 799 closely held companies in 22 countries, we found a significant positive correlation between corporate value and the fraction of the board made up of independent directors. Moreover, we found this relation to be especially pronounced in countries that afford investors weak legal protection—countries where controlling shareholders presumably have then greatest opportunity to increase corporate values by submitting to greater oversight.</p><p>Thus, the findings of our study are consistent with the possibility that the appointment of directors with no ties to the controlling shareholder can be a powerful mechanism to reduce the threat of resource diversion and transfer of value from minority shareholders. But how reliable is this interpretation, given that the same controlling shareholders that have the power to appoint the board members also have the power—perhaps if they do too good a job—to dismiss them?</p><p>To address this issue, we performed several additional tests designed to detect the ability of independent directors to monitor the actions of the controlling shareholder. One such test revealed that 71% of independent directors in our sample sat on multiple corporate boards. We reasoned that multiple appointments are more likely to be a proxy for “reputational capital,” and that directors with multiple appointments should be less willing to jeopardize those reputations by proving to be ineffective monitors. As a second check on whether independent directors help reduce the threat of transfers of corporate resources, we also found that the frequency of related-party transactions was significantly lower in companies with larger fractions of independent directors, and that this reduced frequency was associated with higher corporate values.</p><p>A third set of tests investigated the possibility that an increase in the value of corporate shares would be most beneficial to controlling shareholders that plan either to issue equity on behalf of the firm or to sell equity on personal account. The tradeoff faced by such shareholders in these circumstances is between a higher value for their shares and reduced private control benefits. In other words, controlling shareholders are likely to appoint independent directors when their expected gains from higher share values outweigh their sacrifice of private benefits. Consistent with this argument, we found that the companies in our sample that issued equity had larger fractions of independent directors.</p><p>In the pages that follow, we explore each of the questions raised here in greater depth, report the relevant results of our recent study, and present representative case studies.</p><p>Because the board is appointed and dismissed by the controlling shareholder, the question arises as to whether such directors can perform their duties effectively. After all, directors appointed by controlling shareholders may be subject to various pressures, including the threat of dismissal at any time, for opposing the interests of those shareholders.</p><p>We believe there are three necessary conditions for boards of directors to be effective monitors of controlling shareholders. First, independent directors must be able to raise the cost to the controlling shareholder of diverting resources for personal benefit. It is worth noting that independent directors do not have to monitor the controlling shareholder's actions perfectly. To the extent they make it more difficult and costly for the controlling shareholder to extract private benefits, independent directors can help preserve value for minority shareholders.</p><p>Second, independent directors must have the incentive to monitor the controlling shareholder. As Eugene Fama and Michael Jensen argued in a classic corporate governance paper in the early 1980s, this incentive is provided by the mere existence of a well-functioning market for the services of independent directors.4 Thanks to such a market, independent directors have “human” or “reputational” capital at stake that can be lost “when internal control breaks down” and the companies under their oversight perform badly. To assess the reputational capital of independent directors, we gathered information on the number of directorships held by such directors. Finding that more than 70% of the over 4000 independent directors in our sample served on multiple boards, we concluded that there is a robust market for the services of independent directors.</p><p>But having the incentive to monitor may not be enough. Independent directors must also have the power to perform their duties well. In examining the extent to which this condition for effective monitoring is likely to hold, we started by noting the finding of previous research that, in 20 of the 22 countries in our sample, directors have a legal responsibility to curb self-dealing actions by the controlling shareholder, and can be held legally accountable for failing to do so.5 This mandate gives independent directors the legal authority to act on behalf of minority shareholders. Along with such authority, such directors also routinely seek and obtain assurances from the controlling shareholders that they will have the freedom and power to perform their duties effectively.</p><p>We gathered data on share ownership and boards of directors for companies from 22 countries as of the end of 2002. These are predominantly countries with well-developed economies, for whose companies we were able to locate data on both share ownership and board composition. Our initial sample included the 70 largest publicly traded companies based on market capitalization from each country.</p><p>Before we could determine director affiliation, our first task was to identify companies with a controlling shareholder. We defined a controlling shareholder as the largest single owner of voting rights in any company where that owner controlled at least 10% of the firm's votes.6 Figure 1 provides information on the identity of the controlling shareholder by country. Of all controlling shareholders in our sample, 347 were individuals or families, 226 were privately held operating or holding companies, 101 were privately held financial institutions, and 108 were governments.</p><p>The last 20 years have seen the issuance of corporate governance codes, mandates, recommendations, and listing requirements in more than 70 countries worldwide. The vast majority of them place significant emphasis on director independence.7 We used those publications as a guide in arriving at our own definition of what constitutes an independent director. We considered directors to be affiliated with the controlling shareholder (i.e., not independent) if they (1) had the same family name as the controlling shareholder, (2) were employees of the firm, (3) were employees of any company or subsidiary of any company that was positioned “above” the sample firm in the ownership tree, (4) were employees of another firm in which the controlling shareholder had at least a 10% ownership position regardless of whether the second firm was in the ownership tree, (5) were politicians or employees of a government agency when the controlling shareholder was a government, or (6) in cases of a foreign controlling shareholder, were employed by a company domiciled in the same country as the controlling shareholder. Directors who were not identified as being affiliated with the controlling shareholder in any of these ways were designated as “independent.”8</p><p>Figure 2 provides information on directors who are affiliated and unaffiliated with (i.e., independent of) the controlling shareholder. An inspection of this chart reveals that the fraction of independent directors varies significantly across countries, with the highest fraction in the U.S. and the lowest in Japan.</p><p>Because the share of voting rights held by controlling shareholders often exceeds their proportionate claims on cash flows,9 we also gathered information about the voting and ownership rights of the controlling shareholders. A large disparity between voting and cash-flow rights amplifies the incentives of controlling shareholders to exploit minority shareholders.10 For each company with a pyramidal ownership structure in our sample, we determined the fraction of cash-flow rights owned by the controlling shareholder by multiplying his fraction of cash-flow rights held in a sample firm by the fraction of shares owned in each firm along the control chain in the ownership tree. For example, if individual X owned 10% of the shares in company A, which in turn owned 20% in company B, and there were no other large shareholders in B, we considered X to be the controlling shareholder in B with 20% of the voting and 2% (20% times 10%) of the cash-flow rights.</p><p>While it is customary in U.S.-based studies to compute Tobin's Q as a measure of corporate value, international datasets generally lack the depth needed to calculate this measure accurately. As the primary dependent variable in our study, we accordingly used the following variation of Tobin's Q: the market value of equity plus the book value of liabilities (i.e., book assets less book equity) divided by the book value of assets. For each of our sample companies, we calculated and averaged this market-to-book ratio as of the end of 2002 and 2003. To limit the effect of outliers on our findings, we trimmed the top and bottom one percent of the sample ranked by our Tobin's Q proxy, which left a final sample of 782 firms.</p><p>In Table 1, we report the number of firms and other important characteristics of our sample classified by individual countries. Because we extracted only the closely held companies from the 70 largest firms in each country, the number of companies differs across countries. For example, the U.S. and Japan are considerably underrepresented because, among the 70 largest U.S. and Japanese companies, only 16 and 10 firms, respectively, had controlling shareholders. In Italy, by contrast, the number of closely held companies was 56, the highest of all countries in the sample.</p><p>Also reported in Table 1 is our measure of investor protection for each country. We refer to this measure as “LEGAL.” The quality of legal protection afforded to minority shareholders can be thought of as comprising two elements: (1) the statutory rules and provisions (also called de jure protection) and (2) the degree of enforcement of these statutes (de facto protection). LEGAL is the product of the two indices that capture de jure and de facto protection. These are the “Anti-director rights” index, which ranges from 0 to 6, and the “Law and Order” enforcement index from the International Country Risk Guide, which we have rescaled to range from 0 to 10.11</p><p>As can be seen in Table 1, despite our focus on mostly developed countries, we observed significant variation in the degree of protection afforded to minority shareholders. The variable LEGAL ranged from a low of 3.3 in Mexico to a high of 50 in Canada, the U.S., and the U.K. Also worth noting in Table 1 is the significant variation in ownership, board composition, and corporate value (Tobin's Q), both among country averages and among different companies in the same country. In terms of cross-country variation, the percentage of independent directors was highest in the U.S. (75%) and lowest in Japan (38%). As for within-country variation, the minimum and maximum percentages of independent directors in a firm were 45% and 93% in the U.S., and 0.0% and 100% in France, Germany, and Brazil.</p><p>In our first-pass analysis, we compared our version of Tobin's Q against the LEGAL index. For this comparison, countries were classified into three groups with the eight countries having LEGAL ≥ 30 in group 1, the five countries with 30 > LEGAL ≥ 20 in group 2, and the nine countries with LEGAL < 20 in group 3. We found that Qs varied systematically across these three different levels of legal shareholder protection, with higher protection associated with higher Qs: the mean Q of 1.58 for group 1 was significantly greater than the meanQ of 1.38 in group 3 (<i>p</i>-value = 0.01). This analysis served to confirm the generally accepted view that the stronger country-level legal shareholder protection is associated with higher firm values. A more interesting finding emerged when we split the entire sample of companies into three groups according to the percentage of independent directors. The mean and median Qs increase monotonically with the increase in the percentage of independent directors and the differences in means and medians between groups 1 and 3 were statistically significant (<i>p</i>-values < 0.01). The mean Tobin's Q was 1.32 for companies where less than one third of the board was independent directors and 1.57 for those with more than two-thirds.</p><p>To add rigor to our descriptive statistics, we then estimated a series of regressions designed to show the effect of the fraction of independent directors on Tobin's Q.16</p><p>The key coefficients from our regression tests are reproduced in Table 2. Column 1 presents the results of what can be thought of as our “base case” regression. It serves to compare our results to results from previous studies. However, this regression excludes the primary independent variable of interest, the fraction of independent directors on the board (“INDDIR%”). Consistent with prior studies, the nationwide coefficient of LEGAL was positive (and significant with a <i>p</i>-value = 0.01), suggesting that stronger shareholder protection increases firm value. There was also some indication that a higher fraction of cash-flow rights owned by the controlling shareholder enhances corporate value (though the corresponding coefficient is significant at the 10% level only). In subsequent regressions, moreover, these base case results remained essentially unchanged. All in all, in companies with a controlling shareholder, firm value was shown to be positively correlated with the country-level of legal shareholder protection and with the fraction of cash-flow rights held by the controlling shareholder.17</p><p>Having estimated the base-case regression, we then added the key variable of interest, INDDIR%—again, the fraction of independent directors—to the base case regression. As reported in column 2 of the table, the coefficient on INDDIR% in this column was positive and statistically significant (<i>p</i>-value = 0.01). This coefficient could be interpreted as saying that, in the case of a representative company in our sample, a 10% increase in the fraction of a company's independent directors (in other words, for each additional independent director on a board with ten members) is generally associated with a 4% increase in its Tobin's Q ratio. And thus, for each additional $1 billion of assets (in terms of book value), each additional independent director translates into an additional $40 million of value.</p><p>Next, to test the limits of the “linearity” of this relationship, we replaced INDIRR% with a natural log and nonlinear specification of INDDIR%. In that regression, the coefficient (reported in column 3) was not only positive and statistically significant (<i>p</i>-value = 0.02), but the adjusted R<sup>2</sup> increased relative to the linear specification. The better “fit” associated with this logarithmic specification of INDDIR% can be interpreted as saying that although firm value increases with the fraction of independent directors, it increases at a decreasing rate as that fraction increases (and thus adding the fifth independent director adds less value than the third or the fourth).</p><p>Given our assumption that controlling shareholders are more likely to appoint independent directors when their companies issue equity, we set out to examine the relation between the frequency of seasoned equity offerings (SEOs) and board composition. We found that, during the period 2002–2004, 198, or about one in four, of our 799 sample companies undertook one or more SEOs that raised at least $10 million.</p><p>As a first pass, we identified those sample firms that had issued equity and those that had not, and calculated the mean percentage of independent directors, INDDIR%, for the two groups. The average INDDIR% for firms that had issued equity was 56.1%, while the average INDDIR% for non-issuing firms was 50.2% (The difference in means between the two groups was statistically significant with a <i>p</i>-value < 0.01).</p><p>Next we undertook a regression analysis intended to investigate the extent to which SEOs have systematic effects on board composition. The dependent variable in this model was INDDIR% and the key independent variable was a 1/0 indicator of an SEO (not including rights offerings).22 As reported in the first column of Table 3, the coefficient of SEO was positive and statistically significant (at the 0.01 level or less),23 supporting our conjecture that the issuance of outside equity is an important determinant of board composition in companies with controlling shareholders.</p><p>One of the primary means by which controlling shareholders are alleged to take advantage of minority shareholders is through transactions with related companies that transfer corporate resources and value to firms in which the controlling shareholder has a majority ownership position. Such transactions are frequently referred to as tunneling.24</p><p>Although such transactions cannot be directly observed,25 we assumed that much of this activity is accomplished through related party transactions (RPTs). Strong boards have the potential to limit such wealth transfers by monitoring the terms of RPTs and preventing those that are clearly against the interests of minority holders. Following this line of reasoning, we hypothesized that RPTs should occur less frequently in firms with more independent directors; and when RPTs do occur, they should have more advantageous terms for the minority shareholders than in firms with mostly affiliated directors. Though we have no way of knowing the terms of RPTs, we can observe their frequency because each of our sample countries requires disclosure of RPTs in periodic filings.</p><p>To classify a transaction as a RPT, we borrowed a classification scheme adopted by prior research studies.26 We considered five types of dealings to be RPTs: (1) acquisition by the sample firm of assets and/or stock from the controlling shareholder or from any other firm affiliated with the controlling shareholder; (2) asset sales by the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; (3) asset swaps between the sample firm and the controlling shareholder or any other firm-affiliated with the controlling shareholder; (4) debt and/or loan relief from the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; and (5) sales and/or purchases of merchandise from and/or to the sample firm from and/or to the controlling shareholder or any other firm affiliated with the controlling shareholder.27 A search of filings for RPTs yielded information on RPTs conducted by 148 sample firms in 2002.</p><p>For those of our sample companies that reported RPTs, the mean percentage of independent directors (INDDIR%) was 49.4%, as compared to 53.2% for those companies that did not (The difference in means was 3.8%, with a <i>p</i>-value of 0.14; the difference in median INDDIR% values between the groups revealed a difference of 7.1% with a <i>p</i>-value of 0.03).</p><p>To control for other factors that could affect the likelihood of RPTs, we estimated a logit regression in which the dependent variable was a 1/0 indicator for the occurrence of an RPT and the key independent variable was ln (INDDIR%). As reported in Table 4, the coefficient of ln (INDDIR%) was negative and statistically significant, implying that a higher fraction of independent directors on the board reduces the likelihood of RPTs. For a typical firm in our sample, holding everything else at a fixed value, increasing the fraction of independent directors from 40% to 60% will reduce the odds of observing an RPT by 19%, and increasing the fraction of independent directors from 40% to 80% will reduce those odds by approximately 30%.</p><p>To supplement our logit analysis on RPTs and ln (INDIRR%) we estimated a country random effects regression in which the dependent variable was the average Tobin's Q for 2002–2003 and the key independent variable was RPT.</p><p>The other independent variables were the same as in the second column of Table 2 except that we excluded the two board variables ln (INDDIR%) and ln (board size). In this regression, presented in column 2 of Table 4, the coefficient of RPT is negative (with a <i>p</i>-value of 0.06), while the coefficient of LEGAL is positive (with a <i>p</i>-value of 0.04). Thus RPTs appear to have a negative effect on corporate value, even after controlling for the legal environment.</p><p>In sum, the results of our regression analyses are consistent with the interpretation that independent directors can reduce the threat of wealth transfers to the controlling shareholder by limiting disadvantageous RPTs.</p><p>Our findings indicate that controlling shareholders intent on increasing the value of their companies can do so by appointing independent directors. For example, our results can be interpreted as saying that, in the case of a representative company in a country with an average level of protection for minority shareholders, a 10% increase in the fraction of a company's independent directors is associated with a 4% increase in its Tobin's Q ratio. But, as our findings also suggest, such effects on value are expected to be considerably larger in countries with limited minority shareholder rights. For example, by increasing the percentage of unaffiliated directors from 10% to 90%, a controlling shareholder of a company in a country such as Mexico can expect to see the Q ratio of his company increase by almost 15% (from 1.41 to 1.60). Nevertheless, that percentage increase in value would not be enough to make up the full loss in value associated with weak country-level shareholder legal protection. Our analysis suggests that the same company, if based say in the U.K., would be expected to have a Q ratio of about 1.90 even with a board composed of no more than 10% independent directors.</p><p>But what about controlling shareholders of companies in a country with moderate legal protection? Can they benefit from appointing a strong board? Our analysis suggests that for a controlling shareholder in a country such as India, with a LEGAL index of 20, increasing the percentage of independent directors from 10% to 90% will raise the firm's Q from 1.58 to 1.80.</p><p>At the same time, our findings also suggest that this increase in Q is equivalent to the expected effect of raising a country's legal protection score from 20 to 40 (the score in Australia). Thus, in countries like India, appointing independent boards can be an effective, though probably not a complete, substitute for strengthening a country's legal system.</p><p>In sum, independent directors can make a big difference, particularly in countries where legal protection for shareholders is weak.</p>\",\"PeriodicalId\":46789,\"journal\":{\"name\":\"Journal of Applied Corporate Finance\",\"volume\":\"35 1\",\"pages\":\"72-82\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-04-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12543\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Applied Corporate Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12543\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12543","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Does board independence matter in companies with a controlling shareholder?

Studies have reported valuation discounts for publicly traded companies based in countries that provide weak legal protection for minority shareholders.1 Such discounts are often attributed to the ability of controlling shareholders to extract “private benefits” that come at the expense of minority shareholders. Without sufficient legal deterrents, controlling shareholders have both the incentive and the ability to transfer corporate resources to themselves for personal consumption or gain. These transfers take a number of forms, including related-party “tunneling” transactions as well as corporate perks and, in some cases, outright theft.

But under certain circumstances—notably, when their companies want to raise capital by selling shares—the controlling shareholders may face a stronger incentive to reduce this value discount by providing credible commitments to outside investors to forgo this diversion of corporate resources. Various commitment mechanisms have been proposed in the literature, including cross-listing on U.S. exchanges as well as general improvements in overall corporate governance systems.2 But another possible solution is more effective oversight of controlling shareholders by corporate boards.

We recently published a study that investigated the effects of appointing more independent directors on the value discounts of companies controlled by a dominant shareholder.3 Using biographical data on nearly 8000 directors of 799 closely held companies in 22 countries, we found a significant positive correlation between corporate value and the fraction of the board made up of independent directors. Moreover, we found this relation to be especially pronounced in countries that afford investors weak legal protection—countries where controlling shareholders presumably have then greatest opportunity to increase corporate values by submitting to greater oversight.

Thus, the findings of our study are consistent with the possibility that the appointment of directors with no ties to the controlling shareholder can be a powerful mechanism to reduce the threat of resource diversion and transfer of value from minority shareholders. But how reliable is this interpretation, given that the same controlling shareholders that have the power to appoint the board members also have the power—perhaps if they do too good a job—to dismiss them?

To address this issue, we performed several additional tests designed to detect the ability of independent directors to monitor the actions of the controlling shareholder. One such test revealed that 71% of independent directors in our sample sat on multiple corporate boards. We reasoned that multiple appointments are more likely to be a proxy for “reputational capital,” and that directors with multiple appointments should be less willing to jeopardize those reputations by proving to be ineffective monitors. As a second check on whether independent directors help reduce the threat of transfers of corporate resources, we also found that the frequency of related-party transactions was significantly lower in companies with larger fractions of independent directors, and that this reduced frequency was associated with higher corporate values.

A third set of tests investigated the possibility that an increase in the value of corporate shares would be most beneficial to controlling shareholders that plan either to issue equity on behalf of the firm or to sell equity on personal account. The tradeoff faced by such shareholders in these circumstances is between a higher value for their shares and reduced private control benefits. In other words, controlling shareholders are likely to appoint independent directors when their expected gains from higher share values outweigh their sacrifice of private benefits. Consistent with this argument, we found that the companies in our sample that issued equity had larger fractions of independent directors.

In the pages that follow, we explore each of the questions raised here in greater depth, report the relevant results of our recent study, and present representative case studies.

Because the board is appointed and dismissed by the controlling shareholder, the question arises as to whether such directors can perform their duties effectively. After all, directors appointed by controlling shareholders may be subject to various pressures, including the threat of dismissal at any time, for opposing the interests of those shareholders.

We believe there are three necessary conditions for boards of directors to be effective monitors of controlling shareholders. First, independent directors must be able to raise the cost to the controlling shareholder of diverting resources for personal benefit. It is worth noting that independent directors do not have to monitor the controlling shareholder's actions perfectly. To the extent they make it more difficult and costly for the controlling shareholder to extract private benefits, independent directors can help preserve value for minority shareholders.

Second, independent directors must have the incentive to monitor the controlling shareholder. As Eugene Fama and Michael Jensen argued in a classic corporate governance paper in the early 1980s, this incentive is provided by the mere existence of a well-functioning market for the services of independent directors.4 Thanks to such a market, independent directors have “human” or “reputational” capital at stake that can be lost “when internal control breaks down” and the companies under their oversight perform badly. To assess the reputational capital of independent directors, we gathered information on the number of directorships held by such directors. Finding that more than 70% of the over 4000 independent directors in our sample served on multiple boards, we concluded that there is a robust market for the services of independent directors.

But having the incentive to monitor may not be enough. Independent directors must also have the power to perform their duties well. In examining the extent to which this condition for effective monitoring is likely to hold, we started by noting the finding of previous research that, in 20 of the 22 countries in our sample, directors have a legal responsibility to curb self-dealing actions by the controlling shareholder, and can be held legally accountable for failing to do so.5 This mandate gives independent directors the legal authority to act on behalf of minority shareholders. Along with such authority, such directors also routinely seek and obtain assurances from the controlling shareholders that they will have the freedom and power to perform their duties effectively.

We gathered data on share ownership and boards of directors for companies from 22 countries as of the end of 2002. These are predominantly countries with well-developed economies, for whose companies we were able to locate data on both share ownership and board composition. Our initial sample included the 70 largest publicly traded companies based on market capitalization from each country.

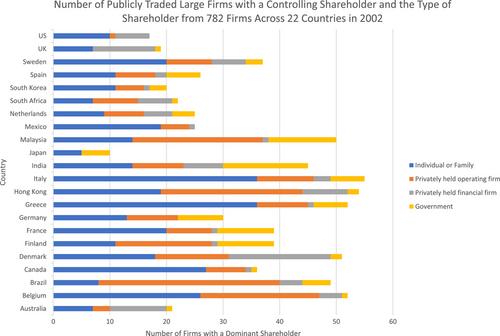

Before we could determine director affiliation, our first task was to identify companies with a controlling shareholder. We defined a controlling shareholder as the largest single owner of voting rights in any company where that owner controlled at least 10% of the firm's votes.6 Figure 1 provides information on the identity of the controlling shareholder by country. Of all controlling shareholders in our sample, 347 were individuals or families, 226 were privately held operating or holding companies, 101 were privately held financial institutions, and 108 were governments.

The last 20 years have seen the issuance of corporate governance codes, mandates, recommendations, and listing requirements in more than 70 countries worldwide. The vast majority of them place significant emphasis on director independence.7 We used those publications as a guide in arriving at our own definition of what constitutes an independent director. We considered directors to be affiliated with the controlling shareholder (i.e., not independent) if they (1) had the same family name as the controlling shareholder, (2) were employees of the firm, (3) were employees of any company or subsidiary of any company that was positioned “above” the sample firm in the ownership tree, (4) were employees of another firm in which the controlling shareholder had at least a 10% ownership position regardless of whether the second firm was in the ownership tree, (5) were politicians or employees of a government agency when the controlling shareholder was a government, or (6) in cases of a foreign controlling shareholder, were employed by a company domiciled in the same country as the controlling shareholder. Directors who were not identified as being affiliated with the controlling shareholder in any of these ways were designated as “independent.”8

Figure 2 provides information on directors who are affiliated and unaffiliated with (i.e., independent of) the controlling shareholder. An inspection of this chart reveals that the fraction of independent directors varies significantly across countries, with the highest fraction in the U.S. and the lowest in Japan.

Because the share of voting rights held by controlling shareholders often exceeds their proportionate claims on cash flows,9 we also gathered information about the voting and ownership rights of the controlling shareholders. A large disparity between voting and cash-flow rights amplifies the incentives of controlling shareholders to exploit minority shareholders.10 For each company with a pyramidal ownership structure in our sample, we determined the fraction of cash-flow rights owned by the controlling shareholder by multiplying his fraction of cash-flow rights held in a sample firm by the fraction of shares owned in each firm along the control chain in the ownership tree. For example, if individual X owned 10% of the shares in company A, which in turn owned 20% in company B, and there were no other large shareholders in B, we considered X to be the controlling shareholder in B with 20% of the voting and 2% (20% times 10%) of the cash-flow rights.

While it is customary in U.S.-based studies to compute Tobin's Q as a measure of corporate value, international datasets generally lack the depth needed to calculate this measure accurately. As the primary dependent variable in our study, we accordingly used the following variation of Tobin's Q: the market value of equity plus the book value of liabilities (i.e., book assets less book equity) divided by the book value of assets. For each of our sample companies, we calculated and averaged this market-to-book ratio as of the end of 2002 and 2003. To limit the effect of outliers on our findings, we trimmed the top and bottom one percent of the sample ranked by our Tobin's Q proxy, which left a final sample of 782 firms.

In Table 1, we report the number of firms and other important characteristics of our sample classified by individual countries. Because we extracted only the closely held companies from the 70 largest firms in each country, the number of companies differs across countries. For example, the U.S. and Japan are considerably underrepresented because, among the 70 largest U.S. and Japanese companies, only 16 and 10 firms, respectively, had controlling shareholders. In Italy, by contrast, the number of closely held companies was 56, the highest of all countries in the sample.

Also reported in Table 1 is our measure of investor protection for each country. We refer to this measure as “LEGAL.” The quality of legal protection afforded to minority shareholders can be thought of as comprising two elements: (1) the statutory rules and provisions (also called de jure protection) and (2) the degree of enforcement of these statutes (de facto protection). LEGAL is the product of the two indices that capture de jure and de facto protection. These are the “Anti-director rights” index, which ranges from 0 to 6, and the “Law and Order” enforcement index from the International Country Risk Guide, which we have rescaled to range from 0 to 10.11

As can be seen in Table 1, despite our focus on mostly developed countries, we observed significant variation in the degree of protection afforded to minority shareholders. The variable LEGAL ranged from a low of 3.3 in Mexico to a high of 50 in Canada, the U.S., and the U.K. Also worth noting in Table 1 is the significant variation in ownership, board composition, and corporate value (Tobin's Q), both among country averages and among different companies in the same country. In terms of cross-country variation, the percentage of independent directors was highest in the U.S. (75%) and lowest in Japan (38%). As for within-country variation, the minimum and maximum percentages of independent directors in a firm were 45% and 93% in the U.S., and 0.0% and 100% in France, Germany, and Brazil.

In our first-pass analysis, we compared our version of Tobin's Q against the LEGAL index. For this comparison, countries were classified into three groups with the eight countries having LEGAL ≥ 30 in group 1, the five countries with 30 > LEGAL ≥ 20 in group 2, and the nine countries with LEGAL < 20 in group 3. We found that Qs varied systematically across these three different levels of legal shareholder protection, with higher protection associated with higher Qs: the mean Q of 1.58 for group 1 was significantly greater than the meanQ of 1.38 in group 3 (p-value = 0.01). This analysis served to confirm the generally accepted view that the stronger country-level legal shareholder protection is associated with higher firm values. A more interesting finding emerged when we split the entire sample of companies into three groups according to the percentage of independent directors. The mean and median Qs increase monotonically with the increase in the percentage of independent directors and the differences in means and medians between groups 1 and 3 were statistically significant (p-values < 0.01). The mean Tobin's Q was 1.32 for companies where less than one third of the board was independent directors and 1.57 for those with more than two-thirds.

To add rigor to our descriptive statistics, we then estimated a series of regressions designed to show the effect of the fraction of independent directors on Tobin's Q.16

The key coefficients from our regression tests are reproduced in Table 2. Column 1 presents the results of what can be thought of as our “base case” regression. It serves to compare our results to results from previous studies. However, this regression excludes the primary independent variable of interest, the fraction of independent directors on the board (“INDDIR%”). Consistent with prior studies, the nationwide coefficient of LEGAL was positive (and significant with a p-value = 0.01), suggesting that stronger shareholder protection increases firm value. There was also some indication that a higher fraction of cash-flow rights owned by the controlling shareholder enhances corporate value (though the corresponding coefficient is significant at the 10% level only). In subsequent regressions, moreover, these base case results remained essentially unchanged. All in all, in companies with a controlling shareholder, firm value was shown to be positively correlated with the country-level of legal shareholder protection and with the fraction of cash-flow rights held by the controlling shareholder.17

Having estimated the base-case regression, we then added the key variable of interest, INDDIR%—again, the fraction of independent directors—to the base case regression. As reported in column 2 of the table, the coefficient on INDDIR% in this column was positive and statistically significant (p-value = 0.01). This coefficient could be interpreted as saying that, in the case of a representative company in our sample, a 10% increase in the fraction of a company's independent directors (in other words, for each additional independent director on a board with ten members) is generally associated with a 4% increase in its Tobin's Q ratio. And thus, for each additional $1 billion of assets (in terms of book value), each additional independent director translates into an additional $40 million of value.

Next, to test the limits of the “linearity” of this relationship, we replaced INDIRR% with a natural log and nonlinear specification of INDDIR%. In that regression, the coefficient (reported in column 3) was not only positive and statistically significant (p-value = 0.02), but the adjusted R2 increased relative to the linear specification. The better “fit” associated with this logarithmic specification of INDDIR% can be interpreted as saying that although firm value increases with the fraction of independent directors, it increases at a decreasing rate as that fraction increases (and thus adding the fifth independent director adds less value than the third or the fourth).

Given our assumption that controlling shareholders are more likely to appoint independent directors when their companies issue equity, we set out to examine the relation between the frequency of seasoned equity offerings (SEOs) and board composition. We found that, during the period 2002–2004, 198, or about one in four, of our 799 sample companies undertook one or more SEOs that raised at least $10 million.

As a first pass, we identified those sample firms that had issued equity and those that had not, and calculated the mean percentage of independent directors, INDDIR%, for the two groups. The average INDDIR% for firms that had issued equity was 56.1%, while the average INDDIR% for non-issuing firms was 50.2% (The difference in means between the two groups was statistically significant with a p-value < 0.01).

Next we undertook a regression analysis intended to investigate the extent to which SEOs have systematic effects on board composition. The dependent variable in this model was INDDIR% and the key independent variable was a 1/0 indicator of an SEO (not including rights offerings).22 As reported in the first column of Table 3, the coefficient of SEO was positive and statistically significant (at the 0.01 level or less),23 supporting our conjecture that the issuance of outside equity is an important determinant of board composition in companies with controlling shareholders.

One of the primary means by which controlling shareholders are alleged to take advantage of minority shareholders is through transactions with related companies that transfer corporate resources and value to firms in which the controlling shareholder has a majority ownership position. Such transactions are frequently referred to as tunneling.24

Although such transactions cannot be directly observed,25 we assumed that much of this activity is accomplished through related party transactions (RPTs). Strong boards have the potential to limit such wealth transfers by monitoring the terms of RPTs and preventing those that are clearly against the interests of minority holders. Following this line of reasoning, we hypothesized that RPTs should occur less frequently in firms with more independent directors; and when RPTs do occur, they should have more advantageous terms for the minority shareholders than in firms with mostly affiliated directors. Though we have no way of knowing the terms of RPTs, we can observe their frequency because each of our sample countries requires disclosure of RPTs in periodic filings.

To classify a transaction as a RPT, we borrowed a classification scheme adopted by prior research studies.26 We considered five types of dealings to be RPTs: (1) acquisition by the sample firm of assets and/or stock from the controlling shareholder or from any other firm affiliated with the controlling shareholder; (2) asset sales by the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; (3) asset swaps between the sample firm and the controlling shareholder or any other firm-affiliated with the controlling shareholder; (4) debt and/or loan relief from the sample firm to the controlling shareholder or any other firm affiliated with the controlling shareholder; and (5) sales and/or purchases of merchandise from and/or to the sample firm from and/or to the controlling shareholder or any other firm affiliated with the controlling shareholder.27 A search of filings for RPTs yielded information on RPTs conducted by 148 sample firms in 2002.

For those of our sample companies that reported RPTs, the mean percentage of independent directors (INDDIR%) was 49.4%, as compared to 53.2% for those companies that did not (The difference in means was 3.8%, with a p-value of 0.14; the difference in median INDDIR% values between the groups revealed a difference of 7.1% with a p-value of 0.03).

To control for other factors that could affect the likelihood of RPTs, we estimated a logit regression in which the dependent variable was a 1/0 indicator for the occurrence of an RPT and the key independent variable was ln (INDDIR%). As reported in Table 4, the coefficient of ln (INDDIR%) was negative and statistically significant, implying that a higher fraction of independent directors on the board reduces the likelihood of RPTs. For a typical firm in our sample, holding everything else at a fixed value, increasing the fraction of independent directors from 40% to 60% will reduce the odds of observing an RPT by 19%, and increasing the fraction of independent directors from 40% to 80% will reduce those odds by approximately 30%.

To supplement our logit analysis on RPTs and ln (INDIRR%) we estimated a country random effects regression in which the dependent variable was the average Tobin's Q for 2002–2003 and the key independent variable was RPT.

The other independent variables were the same as in the second column of Table 2 except that we excluded the two board variables ln (INDDIR%) and ln (board size). In this regression, presented in column 2 of Table 4, the coefficient of RPT is negative (with a p-value of 0.06), while the coefficient of LEGAL is positive (with a p-value of 0.04). Thus RPTs appear to have a negative effect on corporate value, even after controlling for the legal environment.

In sum, the results of our regression analyses are consistent with the interpretation that independent directors can reduce the threat of wealth transfers to the controlling shareholder by limiting disadvantageous RPTs.

Our findings indicate that controlling shareholders intent on increasing the value of their companies can do so by appointing independent directors. For example, our results can be interpreted as saying that, in the case of a representative company in a country with an average level of protection for minority shareholders, a 10% increase in the fraction of a company's independent directors is associated with a 4% increase in its Tobin's Q ratio. But, as our findings also suggest, such effects on value are expected to be considerably larger in countries with limited minority shareholder rights. For example, by increasing the percentage of unaffiliated directors from 10% to 90%, a controlling shareholder of a company in a country such as Mexico can expect to see the Q ratio of his company increase by almost 15% (from 1.41 to 1.60). Nevertheless, that percentage increase in value would not be enough to make up the full loss in value associated with weak country-level shareholder legal protection. Our analysis suggests that the same company, if based say in the U.K., would be expected to have a Q ratio of about 1.90 even with a board composed of no more than 10% independent directors.

But what about controlling shareholders of companies in a country with moderate legal protection? Can they benefit from appointing a strong board? Our analysis suggests that for a controlling shareholder in a country such as India, with a LEGAL index of 20, increasing the percentage of independent directors from 10% to 90% will raise the firm's Q from 1.58 to 1.80.

At the same time, our findings also suggest that this increase in Q is equivalent to the expected effect of raising a country's legal protection score from 20 to 40 (the score in Australia). Thus, in countries like India, appointing independent boards can be an effective, though probably not a complete, substitute for strengthening a country's legal system.

In sum, independent directors can make a big difference, particularly in countries where legal protection for shareholders is weak.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: