异构Agent模型的估计:一种似然方法

IF 1.5

3区 经济学

Q2 ECONOMICS

引用次数: 0

摘要

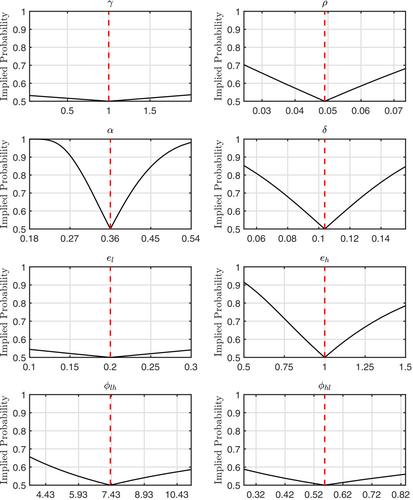

使用Bewley-Hugget-Aiyagari模型,我们展示了如何在异构代理(HA)模型中使用Fokker-Planck方程进行似然推理。我们利用财富和收入的横截面数据研究了蒙特卡罗实验中最大似然估计量(MLE)的有限样本性质。我们使用Kullback–Leibler分歧来研究可能影响推理的识别问题。不受限制的MLE会导致某些参数存在相当大的偏差。校准弱识别参数被证明有助于确定剩余的结构参数。我们通过使用消费者金融调查来估计美国经济的模型来说明我们的方法。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Estimation of Heterogeneous Agent Models: A Likelihood Approach

Using a Bewley-Hugget-Aiyagari model we show how to use the Fokker-Planck equation for likelihood inference in heterogeneous agent (HA) models. We study the finite sample properties of the maximum likelihood estimator (MLE) in Monte Carlo experiments using cross-sectional data on wealth and income. We use the Kullback–Leibler divergence to investigate identification problems that may affect inference. Unrestricted MLE leads to considerable biases of some parameters. Calibrating weakly identified parameters is shown to be useful to pin down the remaining structural parameters. We illustrate our approach by estimating the model for the US economy using the Survey of Consumer Finances.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Oxford Bulletin of Economics and Statistics

管理科学-统计学与概率论

CiteScore

5.10

自引率

0.00%

发文量

54

审稿时长

>12 weeks

期刊介绍:

Whilst the Oxford Bulletin of Economics and Statistics publishes papers in all areas of applied economics, emphasis is placed on the practical importance, theoretical interest and policy-relevance of their substantive results, as well as on the methodology and technical competence of the research.

Contributions on the topical issues of economic policy and the testing of currently controversial economic theories are encouraged, as well as more empirical research on both developed and developing countries.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: