Madeleine J. Fuerst, Christoph Luetge, Raphael Max, Alexander Kriebitz

{"title":"组织完整性度量:建立组织完整性的理论模型","authors":"Madeleine J. Fuerst, Christoph Luetge, Raphael Max, Alexander Kriebitz","doi":"10.1111/basr.12329","DOIUrl":null,"url":null,"abstract":"<p>Organizational integrity is a key concept with and through which a company can assume its responsibility for ethical and societal issues. It is a basic premise for sustainable corporate success, as ethical risks ultimately become economic risks for a company. Recent research shows the potential of integrity-based governance models to reduce corporate risks and to improve business performance. However, companies are not yet able to assess nor evaluate their level of organizational integrity in a sound and systematic way. We aim to develop a theoretical model as a basis for the measurement of organizational integrity by conceptualizing the construct and sizing the theoretical model's scope. We suggest that the theoretical model follows a holistic approach and involves three types of dimensions: prerequisite dimensions, independent dimensions, and dependent dimensions. The organizational integrity triad—consisting of active commitments to self-imposed norms and principles, their transparent institutionalization into corporate processes and structures, and their implementation into action—plays a key role in this context.</p>","PeriodicalId":46747,"journal":{"name":"BUSINESS AND SOCIETY REVIEW","volume":"128 3","pages":"417-435"},"PeriodicalIF":1.8000,"publicationDate":"2023-09-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/basr.12329","citationCount":"0","resultStr":"{\"title\":\"Toward organizational integrity measurement: Developing a theoretical model of organizational integrity\",\"authors\":\"Madeleine J. Fuerst, Christoph Luetge, Raphael Max, Alexander Kriebitz\",\"doi\":\"10.1111/basr.12329\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Organizational integrity is a key concept with and through which a company can assume its responsibility for ethical and societal issues. It is a basic premise for sustainable corporate success, as ethical risks ultimately become economic risks for a company. Recent research shows the potential of integrity-based governance models to reduce corporate risks and to improve business performance. However, companies are not yet able to assess nor evaluate their level of organizational integrity in a sound and systematic way. We aim to develop a theoretical model as a basis for the measurement of organizational integrity by conceptualizing the construct and sizing the theoretical model's scope. We suggest that the theoretical model follows a holistic approach and involves three types of dimensions: prerequisite dimensions, independent dimensions, and dependent dimensions. The organizational integrity triad—consisting of active commitments to self-imposed norms and principles, their transparent institutionalization into corporate processes and structures, and their implementation into action—plays a key role in this context.</p>\",\"PeriodicalId\":46747,\"journal\":{\"name\":\"BUSINESS AND SOCIETY REVIEW\",\"volume\":\"128 3\",\"pages\":\"417-435\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-09-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/basr.12329\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"BUSINESS AND SOCIETY REVIEW\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/basr.12329\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"BUSINESS AND SOCIETY REVIEW","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/basr.12329","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS","Score":null,"Total":0}

Toward organizational integrity measurement: Developing a theoretical model of organizational integrity

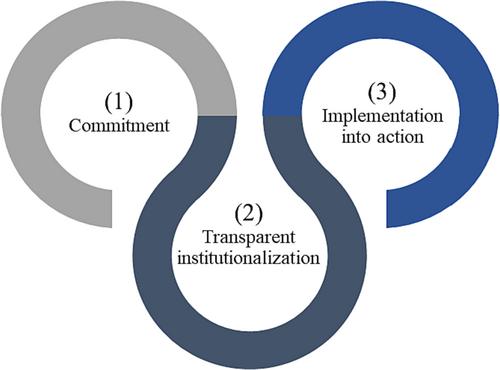

Organizational integrity is a key concept with and through which a company can assume its responsibility for ethical and societal issues. It is a basic premise for sustainable corporate success, as ethical risks ultimately become economic risks for a company. Recent research shows the potential of integrity-based governance models to reduce corporate risks and to improve business performance. However, companies are not yet able to assess nor evaluate their level of organizational integrity in a sound and systematic way. We aim to develop a theoretical model as a basis for the measurement of organizational integrity by conceptualizing the construct and sizing the theoretical model's scope. We suggest that the theoretical model follows a holistic approach and involves three types of dimensions: prerequisite dimensions, independent dimensions, and dependent dimensions. The organizational integrity triad—consisting of active commitments to self-imposed norms and principles, their transparent institutionalization into corporate processes and structures, and their implementation into action—plays a key role in this context.

期刊介绍:

Business and Society Review addresses a wide range of ethical issues concerning the relationships between business, society, and the public good. Its contents are of vital concern to business people, academics, and others involved in the contemporary debate about the proper role of business in society. The journal publishes papers from all those working in this important area, including researchers and business professionals, members of the legal profession, government administrators and many others.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: