{"title":"金融市场能预测宏观经济表现吗?基于风险的措施的美国证据","authors":"David G. McMillan","doi":"10.1111/manc.12451","DOIUrl":null,"url":null,"abstract":"<p>Financial markets are expected to predict macroeconomic conditions as movement in the former depends upon expectations of future performance for the latter. However, existing evidence is mixed. We argue that this arises because the stock return and term structure series typically used in studies, fail to sufficiently capture investor risk preferences. For US data, we use the variance risk premium (VRP) and default yield (DFY) to better capture such a risk measure and demonstrate that these variables exhibit greater evidence of predictive power for key macroeconomic series. In addition to VRP and DFY, we include further variables that may also capture market risk. Given similar dynamics between different risk measures and the potential for multicollinearity in estimation, we consider variable combinations. Using results obtained through predictive regressions, out-of-sample forecasting and a probit model designed to capture periods of expansion and contraction, we show that these combination variables can predict future movements in macroeconomic conditions as well as results using individual variables. Of key interest, combinations that include the VRP and DFY are preferred across all macro-series.</p>","PeriodicalId":47546,"journal":{"name":"Manchester School","volume":"91 5","pages":"439-466"},"PeriodicalIF":0.7000,"publicationDate":"2023-07-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/manc.12451","citationCount":"0","resultStr":"{\"title\":\"Do financial markets predict macroeconomic performance? US evidence from risk-based measures\",\"authors\":\"David G. McMillan\",\"doi\":\"10.1111/manc.12451\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Financial markets are expected to predict macroeconomic conditions as movement in the former depends upon expectations of future performance for the latter. However, existing evidence is mixed. We argue that this arises because the stock return and term structure series typically used in studies, fail to sufficiently capture investor risk preferences. For US data, we use the variance risk premium (VRP) and default yield (DFY) to better capture such a risk measure and demonstrate that these variables exhibit greater evidence of predictive power for key macroeconomic series. In addition to VRP and DFY, we include further variables that may also capture market risk. Given similar dynamics between different risk measures and the potential for multicollinearity in estimation, we consider variable combinations. Using results obtained through predictive regressions, out-of-sample forecasting and a probit model designed to capture periods of expansion and contraction, we show that these combination variables can predict future movements in macroeconomic conditions as well as results using individual variables. Of key interest, combinations that include the VRP and DFY are preferred across all macro-series.</p>\",\"PeriodicalId\":47546,\"journal\":{\"name\":\"Manchester School\",\"volume\":\"91 5\",\"pages\":\"439-466\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2023-07-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/manc.12451\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Manchester School\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/manc.12451\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Manchester School","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/manc.12451","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Do financial markets predict macroeconomic performance? US evidence from risk-based measures

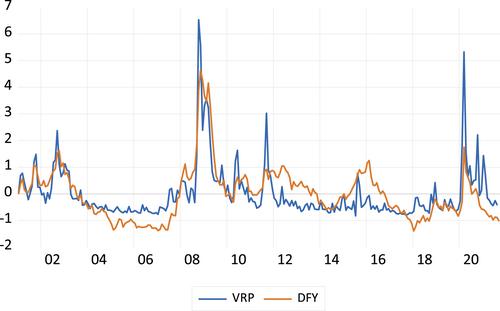

Financial markets are expected to predict macroeconomic conditions as movement in the former depends upon expectations of future performance for the latter. However, existing evidence is mixed. We argue that this arises because the stock return and term structure series typically used in studies, fail to sufficiently capture investor risk preferences. For US data, we use the variance risk premium (VRP) and default yield (DFY) to better capture such a risk measure and demonstrate that these variables exhibit greater evidence of predictive power for key macroeconomic series. In addition to VRP and DFY, we include further variables that may also capture market risk. Given similar dynamics between different risk measures and the potential for multicollinearity in estimation, we consider variable combinations. Using results obtained through predictive regressions, out-of-sample forecasting and a probit model designed to capture periods of expansion and contraction, we show that these combination variables can predict future movements in macroeconomic conditions as well as results using individual variables. Of key interest, combinations that include the VRP and DFY are preferred across all macro-series.

期刊介绍:

The Manchester School was first published more than seventy years ago and has become a distinguished, internationally recognised, general economics journal. The Manchester School publishes high-quality research covering all areas of the economics discipline, although the editors particularly encourage original contributions, or authoritative surveys, in the fields of microeconomics (including industrial organisation and game theory), macroeconomics, econometrics (both theory and applied) and labour economics.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: