{"title":"审计报告的变化和审计委员会的力量对银行董事的看法和决定的影响:一项实验调查","authors":"Michelle Höfmann, Christiane Pott, Reiner Quick","doi":"10.1111/ijau.12308","DOIUrl":null,"url":null,"abstract":"<p>This study investigates the impact of two changes to the auditor's report—a separate section addressing going concern uncertainties (GCU section [GCUsec]) and information on management and auditor responsibilities—and the characteristics of the audit committee on bank directors' perceptions and decisions. In a 2 × 2 × 2 between-subjects experimental design with 85 German bank directors, we observe that a GCUsec in the auditor's report leads to more unfavourable decisions. Contrarily, explanations of responsibilities and different characteristics of the audit committee do not significantly impact on bank directors' perceptions and decisions. We thus confirm the effectiveness of the International Auditing and Assurance Standards Board (IAASB)'s revision of the International Standard on Auditing (ISA) 570 to enhance the informational value and decision usefulness of the auditor's report.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"28 2","pages":"408-431"},"PeriodicalIF":1.4000,"publicationDate":"2023-03-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12308","citationCount":"0","resultStr":"{\"title\":\"The impact of changes to auditors' reporting and audit committee strength on bank directors' perceptions and decisions: An experimental investigation\",\"authors\":\"Michelle Höfmann, Christiane Pott, Reiner Quick\",\"doi\":\"10.1111/ijau.12308\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study investigates the impact of two changes to the auditor's report—a separate section addressing going concern uncertainties (GCU section [GCUsec]) and information on management and auditor responsibilities—and the characteristics of the audit committee on bank directors' perceptions and decisions. In a 2 × 2 × 2 between-subjects experimental design with 85 German bank directors, we observe that a GCUsec in the auditor's report leads to more unfavourable decisions. Contrarily, explanations of responsibilities and different characteristics of the audit committee do not significantly impact on bank directors' perceptions and decisions. We thus confirm the effectiveness of the International Auditing and Assurance Standards Board (IAASB)'s revision of the International Standard on Auditing (ISA) 570 to enhance the informational value and decision usefulness of the auditor's report.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"28 2\",\"pages\":\"408-431\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-03-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12308\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12308\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12308","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The impact of changes to auditors' reporting and audit committee strength on bank directors' perceptions and decisions: An experimental investigation

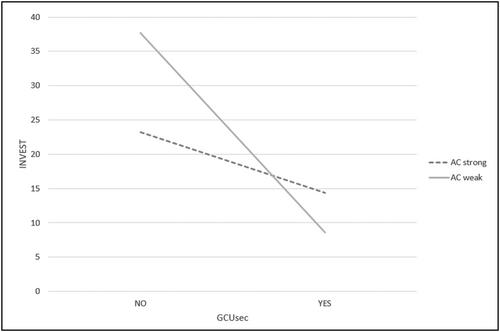

This study investigates the impact of two changes to the auditor's report—a separate section addressing going concern uncertainties (GCU section [GCUsec]) and information on management and auditor responsibilities—and the characteristics of the audit committee on bank directors' perceptions and decisions. In a 2 × 2 × 2 between-subjects experimental design with 85 German bank directors, we observe that a GCUsec in the auditor's report leads to more unfavourable decisions. Contrarily, explanations of responsibilities and different characteristics of the audit committee do not significantly impact on bank directors' perceptions and decisions. We thus confirm the effectiveness of the International Auditing and Assurance Standards Board (IAASB)'s revision of the International Standard on Auditing (ISA) 570 to enhance the informational value and decision usefulness of the auditor's report.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: