Gintautas Silinskas, Arto K. Ahonen, Terhi-Anna Wilska

{"title":"学校和家庭环境促进青少年的财务信心:芬兰PISA 2018金融素养的间接途径","authors":"Gintautas Silinskas, Arto K. Ahonen, Terhi-Anna Wilska","doi":"10.1111/joca.12513","DOIUrl":null,"url":null,"abstract":"<p>This study investigates the associations of adolescents' financial socialization factors—financial education in school and families—with financial confidence (i.e., confidence in using financial and digital financial services). In addition, we examine how financial socialization factors indirectly relate to financial literacy skills through financial confidence and the role of demographic factors (adolescent gender, grade level, parental education, family wealth) on financial socialization, financial confidence, and financial literacy scores. We used data on the 4328 Finnish 15-year-olds participating in the 2018 Programme for International Student Assessment (PISA). We measured financial literacy by cognitive test items and assessed financial socialization and financial confidence by adolescent questionnaires. First, the results showed that financial education in school positively predicted adolescents' confidence in using financial and digital financial services. Second, financial education at schools and in families indirectly predicted students' financial literacy through confidence in using digital financial services. Third, older adolescents were more exposed to financial education at school and in families, whereas adolescents from wealthier families and girls (vs. boys) were exposed to a more frequent discussion of financial matters with parents at home. Furthermore, the boys were more confident in using financial services than the girls, although the financial literacy score did not differ by gender; older adolescents were more confident in using financial services and achieved better financial literacy than younger ones. Finally, higher parental education in the family related to higher financial literacy but not to higher financial confidence, whereas family wealth was related to higher financial confidence but not financial literacy.</p>","PeriodicalId":47976,"journal":{"name":"Journal of Consumer Affairs","volume":"57 1","pages":"593-618"},"PeriodicalIF":2.5000,"publicationDate":"2023-01-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/joca.12513","citationCount":"0","resultStr":"{\"title\":\"School and family environments promote adolescents' financial confidence: Indirect paths to financial literacy skills in Finnish PISA 2018\",\"authors\":\"Gintautas Silinskas, Arto K. Ahonen, Terhi-Anna Wilska\",\"doi\":\"10.1111/joca.12513\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study investigates the associations of adolescents' financial socialization factors—financial education in school and families—with financial confidence (i.e., confidence in using financial and digital financial services). In addition, we examine how financial socialization factors indirectly relate to financial literacy skills through financial confidence and the role of demographic factors (adolescent gender, grade level, parental education, family wealth) on financial socialization, financial confidence, and financial literacy scores. We used data on the 4328 Finnish 15-year-olds participating in the 2018 Programme for International Student Assessment (PISA). We measured financial literacy by cognitive test items and assessed financial socialization and financial confidence by adolescent questionnaires. First, the results showed that financial education in school positively predicted adolescents' confidence in using financial and digital financial services. Second, financial education at schools and in families indirectly predicted students' financial literacy through confidence in using digital financial services. Third, older adolescents were more exposed to financial education at school and in families, whereas adolescents from wealthier families and girls (vs. boys) were exposed to a more frequent discussion of financial matters with parents at home. Furthermore, the boys were more confident in using financial services than the girls, although the financial literacy score did not differ by gender; older adolescents were more confident in using financial services and achieved better financial literacy than younger ones. Finally, higher parental education in the family related to higher financial literacy but not to higher financial confidence, whereas family wealth was related to higher financial confidence but not financial literacy.</p>\",\"PeriodicalId\":47976,\"journal\":{\"name\":\"Journal of Consumer Affairs\",\"volume\":\"57 1\",\"pages\":\"593-618\"},\"PeriodicalIF\":2.5000,\"publicationDate\":\"2023-01-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/joca.12513\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Consumer Affairs\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/joca.12513\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Consumer Affairs","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/joca.12513","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS","Score":null,"Total":0}

School and family environments promote adolescents' financial confidence: Indirect paths to financial literacy skills in Finnish PISA 2018

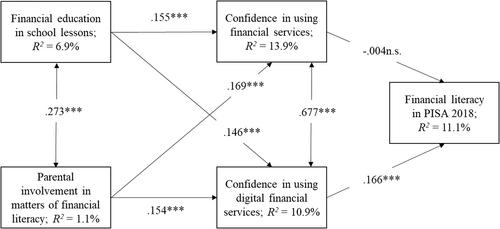

This study investigates the associations of adolescents' financial socialization factors—financial education in school and families—with financial confidence (i.e., confidence in using financial and digital financial services). In addition, we examine how financial socialization factors indirectly relate to financial literacy skills through financial confidence and the role of demographic factors (adolescent gender, grade level, parental education, family wealth) on financial socialization, financial confidence, and financial literacy scores. We used data on the 4328 Finnish 15-year-olds participating in the 2018 Programme for International Student Assessment (PISA). We measured financial literacy by cognitive test items and assessed financial socialization and financial confidence by adolescent questionnaires. First, the results showed that financial education in school positively predicted adolescents' confidence in using financial and digital financial services. Second, financial education at schools and in families indirectly predicted students' financial literacy through confidence in using digital financial services. Third, older adolescents were more exposed to financial education at school and in families, whereas adolescents from wealthier families and girls (vs. boys) were exposed to a more frequent discussion of financial matters with parents at home. Furthermore, the boys were more confident in using financial services than the girls, although the financial literacy score did not differ by gender; older adolescents were more confident in using financial services and achieved better financial literacy than younger ones. Finally, higher parental education in the family related to higher financial literacy but not to higher financial confidence, whereas family wealth was related to higher financial confidence but not financial literacy.

期刊介绍:

The ISI impact score of Journal of Consumer Affairs now places it among the leading business journals and one of the top handful of marketing- related publications. The immediacy index score, showing how swiftly the published studies are cited or applied in other publications, places JCA seventh of those same 77 journals. More importantly, in these difficult economic times, JCA is the leading journal whose focus for over four decades has been on the interests of consumers in the marketplace. With the journal"s origins in the consumer movement and consumer protection concerns, the focus for papers in terms of both research questions and implications must involve the consumer"s interest and topics must be addressed from the consumers point of view.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: