通过稀疏性识别和解释因素模型中的因素:不同的方法

IF 2.3

3区 经济学

Q2 ECONOMICS

引用次数: 5

摘要

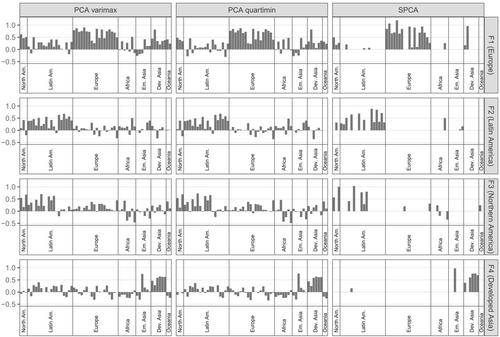

本文考虑了不同的方法来识别因子结构和解释因子,而不通过限制施加它们的解释:稀疏主成分分析和因子旋转。我们对稀疏主成分分析估计的因子建立了新的一致性结果。蒙特卡罗模拟表明,即使在小样本中,我们的方法也能准确地估计因子结构。我们将它们应用于有关国际商业周期和美国经济的大型数据集。对于每个实证应用,他们都确定了相同的因素结构,提供了清晰的经济解释。这些探索性方法可以特别证明或补充那些强加先验因素结构的方法。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Identifying and interpreting the factors in factor models via sparsity: Different approaches

This paper considers different approaches for identifying the factor structure and interpreting the factors without imposing their interpretation via restrictions: sparse PCA and factor rotations. We establish a new consistency result for the factors estimated by sparse PCA. Monte Carlo simulations show that our methods accurately estimate the factor structure, even in small samples. We apply them to large datasets about international business cycles and the US economy. For each empirical application, they identify the same factor structure, offering a clear economic interpretation. These exploratory methods can in particular justify or complement approaches that impose the factor structure a priori.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Applied Econometrics

Multiple-

CiteScore

3.70

自引率

4.80%

发文量

63

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: