{"title":"全球金融危机与新冠肺炎-19:来自情绪分析的证据","authors":"Aktham Maghyereh, Hussein Abdoh","doi":"10.1111/infi.12412","DOIUrl":null,"url":null,"abstract":"<p>This study examines the relationship between sentiment and the realized volatility of returns for different asset classes (stocks, bonds, foreign currency, and commodities). Specifically, we aim to answer two key questions: first, how does sentiment relate to volatility during crises (mainly during the global financial crisis [GFC] and the COVID-19 pandemic)? Second, can sentiment be used to forecast volatility during crises? Using two nonparametric methods, mutual information and transfer entropy, we find that information sharing and transfer increased during the pandemic. We also find that sentiment information transfer to the volatility of assets differed between the GFC and the COVID-19 crisis. Since sentiment can reduce uncertainty around the realized variance of assets, we investigate the forecasting ability of sentiment during crises. We find that sentiment has a greater predictive power on realized volatility during crises, with a differential impact on volatility depending on the asset class. Our findings carry important implications for hedging, risk management and building models to predict variance during crises.</p>","PeriodicalId":46336,"journal":{"name":"International Finance","volume":"25 2","pages":"218-248"},"PeriodicalIF":1.5000,"publicationDate":"2022-04-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/infi.12412","citationCount":"3","resultStr":"{\"title\":\"Global financial crisis versus COVID-19: Evidence from sentiment analysis\",\"authors\":\"Aktham Maghyereh, Hussein Abdoh\",\"doi\":\"10.1111/infi.12412\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study examines the relationship between sentiment and the realized volatility of returns for different asset classes (stocks, bonds, foreign currency, and commodities). Specifically, we aim to answer two key questions: first, how does sentiment relate to volatility during crises (mainly during the global financial crisis [GFC] and the COVID-19 pandemic)? Second, can sentiment be used to forecast volatility during crises? Using two nonparametric methods, mutual information and transfer entropy, we find that information sharing and transfer increased during the pandemic. We also find that sentiment information transfer to the volatility of assets differed between the GFC and the COVID-19 crisis. Since sentiment can reduce uncertainty around the realized variance of assets, we investigate the forecasting ability of sentiment during crises. We find that sentiment has a greater predictive power on realized volatility during crises, with a differential impact on volatility depending on the asset class. Our findings carry important implications for hedging, risk management and building models to predict variance during crises.</p>\",\"PeriodicalId\":46336,\"journal\":{\"name\":\"International Finance\",\"volume\":\"25 2\",\"pages\":\"218-248\"},\"PeriodicalIF\":1.5000,\"publicationDate\":\"2022-04-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/infi.12412\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/infi.12412\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/infi.12412","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Global financial crisis versus COVID-19: Evidence from sentiment analysis

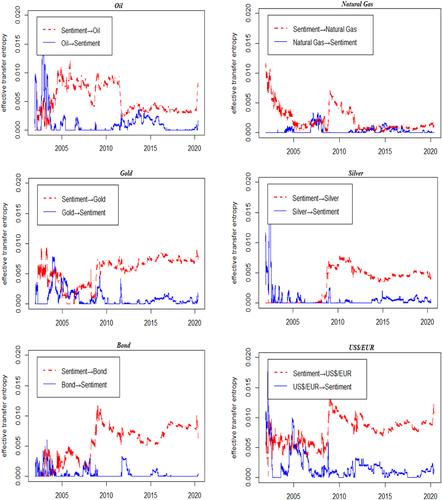

This study examines the relationship between sentiment and the realized volatility of returns for different asset classes (stocks, bonds, foreign currency, and commodities). Specifically, we aim to answer two key questions: first, how does sentiment relate to volatility during crises (mainly during the global financial crisis [GFC] and the COVID-19 pandemic)? Second, can sentiment be used to forecast volatility during crises? Using two nonparametric methods, mutual information and transfer entropy, we find that information sharing and transfer increased during the pandemic. We also find that sentiment information transfer to the volatility of assets differed between the GFC and the COVID-19 crisis. Since sentiment can reduce uncertainty around the realized variance of assets, we investigate the forecasting ability of sentiment during crises. We find that sentiment has a greater predictive power on realized volatility during crises, with a differential impact on volatility depending on the asset class. Our findings carry important implications for hedging, risk management and building models to predict variance during crises.

期刊介绍:

International Finance is a highly selective ISI-accredited journal featuring literate and policy-relevant analysis in macroeconomics and finance. Specific areas of focus include: · Exchange rates · Monetary policy · Political economy · Financial markets · Corporate finance The journal''s readership extends well beyond academia into national treasuries and corporate treasuries, central banks and investment banks, and major international organizations. International Finance publishes lucid, policy-relevant writing in macroeconomics and finance backed by rigorous theory and empirical analysis. In addition to the core double-refereed articles, the journal publishes non-refereed themed book reviews by invited authors and commentary pieces by major policy figures. The editor delivers the vast majority of first-round decisions within three months.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: