Conrad F. J. Beyers, Allan De Freitas, Kojo A. Essel-Mensah, Reyno Seymore, Dimitrios P. Tsomocos

{"title":"南非银行业风险评估的可计算一般均衡模型","authors":"Conrad F. J. Beyers, Allan De Freitas, Kojo A. Essel-Mensah, Reyno Seymore, Dimitrios P. Tsomocos","doi":"10.1007/s10436-020-00362-4","DOIUrl":null,"url":null,"abstract":"<div><p>In this article a banking sector Computable general equilibrium (CGE) model for South Africa is developed. The model is used to estimate the potential effect of regulatory policy on the economy and as a risk assessment tool to assess how changes in regulation affect the economy. The model provides a methodology for regulators of the banking sector and policy makers in South Africa to deal with risk assessment and future regulatory planning. The CGE model allows interactions amongst various entities of the economy so that policy makers could detect the risks in the banking sector. The CGE model used in this paper performed well as a risk assessment tool for the South African banking sector. The results of the various shocks from the model are consistent with the results obtained from similar shocks done in the UK. We establish that default penalty has a higher effect on the banks’ profits and the interest rates than capital requirement infringement penalty. Our results also suggest that interest rate targeting has more controlled effects than monetary base targeting since pecuniary externalities are reduced.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":null,"pages":null},"PeriodicalIF":0.8000,"publicationDate":"2020-03-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s10436-020-00362-4","citationCount":"0","resultStr":"{\"title\":\"A computable general equilibrium model for banking sector risk assessment in South Africa\",\"authors\":\"Conrad F. J. Beyers, Allan De Freitas, Kojo A. Essel-Mensah, Reyno Seymore, Dimitrios P. Tsomocos\",\"doi\":\"10.1007/s10436-020-00362-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>In this article a banking sector Computable general equilibrium (CGE) model for South Africa is developed. The model is used to estimate the potential effect of regulatory policy on the economy and as a risk assessment tool to assess how changes in regulation affect the economy. The model provides a methodology for regulators of the banking sector and policy makers in South Africa to deal with risk assessment and future regulatory planning. The CGE model allows interactions amongst various entities of the economy so that policy makers could detect the risks in the banking sector. The CGE model used in this paper performed well as a risk assessment tool for the South African banking sector. The results of the various shocks from the model are consistent with the results obtained from similar shocks done in the UK. We establish that default penalty has a higher effect on the banks’ profits and the interest rates than capital requirement infringement penalty. Our results also suggest that interest rate targeting has more controlled effects than monetary base targeting since pecuniary externalities are reduced.</p></div>\",\"PeriodicalId\":45289,\"journal\":{\"name\":\"Annals of Finance\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":0.8000,\"publicationDate\":\"2020-03-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1007/s10436-020-00362-4\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10436-020-00362-4\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-020-00362-4","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

A computable general equilibrium model for banking sector risk assessment in South Africa

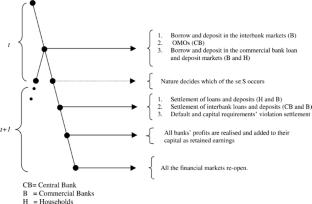

In this article a banking sector Computable general equilibrium (CGE) model for South Africa is developed. The model is used to estimate the potential effect of regulatory policy on the economy and as a risk assessment tool to assess how changes in regulation affect the economy. The model provides a methodology for regulators of the banking sector and policy makers in South Africa to deal with risk assessment and future regulatory planning. The CGE model allows interactions amongst various entities of the economy so that policy makers could detect the risks in the banking sector. The CGE model used in this paper performed well as a risk assessment tool for the South African banking sector. The results of the various shocks from the model are consistent with the results obtained from similar shocks done in the UK. We establish that default penalty has a higher effect on the banks’ profits and the interest rates than capital requirement infringement penalty. Our results also suggest that interest rate targeting has more controlled effects than monetary base targeting since pecuniary externalities are reduced.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: