Jean Bédard, Carl Brousseau, Louis-Philippe Sirois

{"title":"审计业务合伙人识别格式和审计质量","authors":"Jean Bédard, Carl Brousseau, Louis-Philippe Sirois","doi":"10.1111/ijau.12315","DOIUrl":null,"url":null,"abstract":"<p>Exploiting the staggered adoption of three key regulations that implemented distinct engagement partner identification (EPI) formats for separate groups of Canadian firms over a 10-year period, we investigate the association between eight audit quality proxies and three EPI formats: two indirect (auditor permit number in the report, Form AP) and one direct (partner name in the report). This unique setting not only enables us to examine the short-term association between three different EPI formats and audit quality but also to investigate the long-term association for one EPI format (auditor permit number). In the main analysis, out of 32 results of interest, only three are significant and indicate a positive association. Hence, our results show no widespread effect of EPI on audit quality, suggesting that the inconsistent results reported in prior studies may not be driven by the different formats explored or the short window investigated.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"28 1","pages":"97-124"},"PeriodicalIF":1.4000,"publicationDate":"2023-06-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12315","citationCount":"0","resultStr":"{\"title\":\"Engagement partner identification format and audit quality\",\"authors\":\"Jean Bédard, Carl Brousseau, Louis-Philippe Sirois\",\"doi\":\"10.1111/ijau.12315\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Exploiting the staggered adoption of three key regulations that implemented distinct engagement partner identification (EPI) formats for separate groups of Canadian firms over a 10-year period, we investigate the association between eight audit quality proxies and three EPI formats: two indirect (auditor permit number in the report, Form AP) and one direct (partner name in the report). This unique setting not only enables us to examine the short-term association between three different EPI formats and audit quality but also to investigate the long-term association for one EPI format (auditor permit number). In the main analysis, out of 32 results of interest, only three are significant and indicate a positive association. Hence, our results show no widespread effect of EPI on audit quality, suggesting that the inconsistent results reported in prior studies may not be driven by the different formats explored or the short window investigated.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"28 1\",\"pages\":\"97-124\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-06-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12315\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12315\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12315","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Engagement partner identification format and audit quality

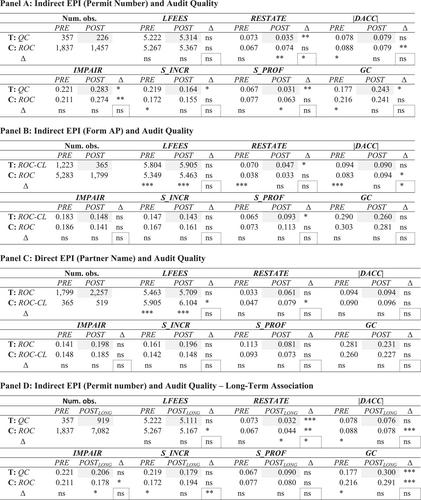

Exploiting the staggered adoption of three key regulations that implemented distinct engagement partner identification (EPI) formats for separate groups of Canadian firms over a 10-year period, we investigate the association between eight audit quality proxies and three EPI formats: two indirect (auditor permit number in the report, Form AP) and one direct (partner name in the report). This unique setting not only enables us to examine the short-term association between three different EPI formats and audit quality but also to investigate the long-term association for one EPI format (auditor permit number). In the main analysis, out of 32 results of interest, only three are significant and indicate a positive association. Hence, our results show no widespread effect of EPI on audit quality, suggesting that the inconsistent results reported in prior studies may not be driven by the different formats explored or the short window investigated.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: