{"title":"管理层盈余预测的准确性和信息量:回顾与统一框架*","authors":"Nicolai A. Preussner, Ewald Aschauer","doi":"10.1111/1911-3838.12294","DOIUrl":null,"url":null,"abstract":"<p>This paper synthesizes the literature on management earnings forecasts (MFs) and adaption mechanisms, combines existing theories into a unifying framework, and discusses the primary determinants of MF accuracy and informativeness. The proposed model refines existing theories by emphasizing the dynamics and multiperiod interactions among firm management, financial analysts, and investors, thereby simplifying the assessment of the complex relations within the forecast cycle. Furthermore, we analyze when and to what extent financial analysts and investors anticipate bias and misleading information. Overall, the literature review provides strong support for a positive correlation between the extent and credibility of MFs, on the one hand, and stock returns, share liquidity, and analyst coverage, on the other hand. Earnings forecasts tend to be optimistically biased, with a positive correlation with forecast uncertainty, earnings flexibility, financial distress, investor sentiment, and the share price dependency of managers' remuneration. Firm growth, legal liability, and litigation risk are significantly associated with forecast pessimism. We also find that MF accuracy increases with previous forecast accuracy, firm size, analyst coverage, analyst agreement, management qualifications, and corporate governance level. Moreover, investors do not anticipate the full extent of predictable forecast bias, leading to systematic share price drifts after the announcement of earnings forecasts and actual earnings. The study's results have substantial implications for researchers, firm managers, investors, financial analysts, and regulators. Although managers may enhance their forecasts' credibility by providing precise, bundled, and disaggregated forecasts, external stakeholders should carefully analyze forecast antecedents and characteristics to assess the direction and magnitude of expected MF bias.</p>","PeriodicalId":43435,"journal":{"name":"Accounting Perspectives","volume":"21 2","pages":"273-330"},"PeriodicalIF":1.6000,"publicationDate":"2022-03-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3838.12294","citationCount":"4","resultStr":"{\"title\":\"The Accuracy and Informativeness of Management Earnings Forecasts: A Review and Unifying Framework*\",\"authors\":\"Nicolai A. Preussner, Ewald Aschauer\",\"doi\":\"10.1111/1911-3838.12294\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper synthesizes the literature on management earnings forecasts (MFs) and adaption mechanisms, combines existing theories into a unifying framework, and discusses the primary determinants of MF accuracy and informativeness. The proposed model refines existing theories by emphasizing the dynamics and multiperiod interactions among firm management, financial analysts, and investors, thereby simplifying the assessment of the complex relations within the forecast cycle. Furthermore, we analyze when and to what extent financial analysts and investors anticipate bias and misleading information. Overall, the literature review provides strong support for a positive correlation between the extent and credibility of MFs, on the one hand, and stock returns, share liquidity, and analyst coverage, on the other hand. Earnings forecasts tend to be optimistically biased, with a positive correlation with forecast uncertainty, earnings flexibility, financial distress, investor sentiment, and the share price dependency of managers' remuneration. Firm growth, legal liability, and litigation risk are significantly associated with forecast pessimism. We also find that MF accuracy increases with previous forecast accuracy, firm size, analyst coverage, analyst agreement, management qualifications, and corporate governance level. Moreover, investors do not anticipate the full extent of predictable forecast bias, leading to systematic share price drifts after the announcement of earnings forecasts and actual earnings. The study's results have substantial implications for researchers, firm managers, investors, financial analysts, and regulators. Although managers may enhance their forecasts' credibility by providing precise, bundled, and disaggregated forecasts, external stakeholders should carefully analyze forecast antecedents and characteristics to assess the direction and magnitude of expected MF bias.</p>\",\"PeriodicalId\":43435,\"journal\":{\"name\":\"Accounting Perspectives\",\"volume\":\"21 2\",\"pages\":\"273-330\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2022-03-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3838.12294\",\"citationCount\":\"4\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Accounting Perspectives\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3838.12294\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Accounting Perspectives","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3838.12294","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The Accuracy and Informativeness of Management Earnings Forecasts: A Review and Unifying Framework*

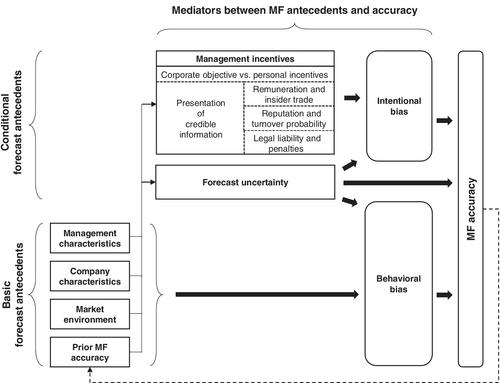

This paper synthesizes the literature on management earnings forecasts (MFs) and adaption mechanisms, combines existing theories into a unifying framework, and discusses the primary determinants of MF accuracy and informativeness. The proposed model refines existing theories by emphasizing the dynamics and multiperiod interactions among firm management, financial analysts, and investors, thereby simplifying the assessment of the complex relations within the forecast cycle. Furthermore, we analyze when and to what extent financial analysts and investors anticipate bias and misleading information. Overall, the literature review provides strong support for a positive correlation between the extent and credibility of MFs, on the one hand, and stock returns, share liquidity, and analyst coverage, on the other hand. Earnings forecasts tend to be optimistically biased, with a positive correlation with forecast uncertainty, earnings flexibility, financial distress, investor sentiment, and the share price dependency of managers' remuneration. Firm growth, legal liability, and litigation risk are significantly associated with forecast pessimism. We also find that MF accuracy increases with previous forecast accuracy, firm size, analyst coverage, analyst agreement, management qualifications, and corporate governance level. Moreover, investors do not anticipate the full extent of predictable forecast bias, leading to systematic share price drifts after the announcement of earnings forecasts and actual earnings. The study's results have substantial implications for researchers, firm managers, investors, financial analysts, and regulators. Although managers may enhance their forecasts' credibility by providing precise, bundled, and disaggregated forecasts, external stakeholders should carefully analyze forecast antecedents and characteristics to assess the direction and magnitude of expected MF bias.

期刊介绍:

Accounting Perspectives provides a forum for peer-reviewed applied research, analysis, synthesis and commentary on issues of interest to academics, practitioners, financial analysts, financial executives, regulators, accounting policy makers and accounting students. Articles are sought from academics and practitioners that address relevant issues in any and all areas of accounting and related fields, including financial accounting and reporting, auditing and other assurance services, management accounting and performance measurement, information systems and related technologies, tax policy and practice, professional ethics, accounting education, and related topics. Without limiting the generality of the foregoing.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: