共同基金的报告频率和公司对低估值的反应:股票回购的作用†

IF 3.2

3区 管理学

Q1 BUSINESS, FINANCE

引用次数: 0

摘要

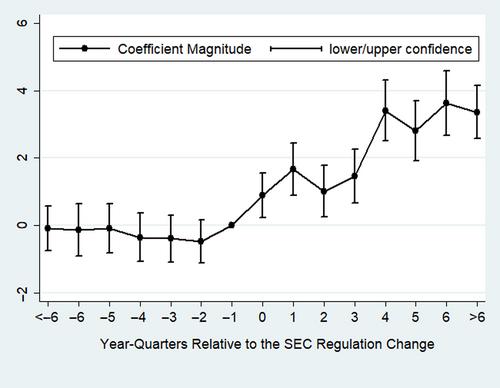

我们研究了增加共同基金投资组合报告频率的监管变化。采用差异中差异设计,我们发现共同基金持股比例较高的公司在监管变化后增加了股票回购。我们的研究表明,这些股票回购是企业对估值过低的理性反应,因为基金经理在监管下变得目光短浅,并出售具有良好长期前景的公司。总的来说,我们的结果揭示了在委托资产管理框架中更频繁报告的意想不到的后果。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Mutual funds' reporting frequency and firms' responses to undervaluation: The role of share repurchases

We examine a regulatory change that increased the reporting frequency of mutual funds' portfolios. Using a difference-in-differences design, we find that firms with greater ownership by mutual funds increase share repurchases following the regulatory change. We show that these share repurchases are a firm's rational response to undervaluation, which occurs because fund managers become shortsighted following the regulation and sell companies with good long-term prospects. Collectively, our results shed light on an unintended consequence of more frequent reporting in a delegated asset management framework.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Contemporary Accounting Research

BUSINESS, FINANCE-

CiteScore

6.20

自引率

11.10%

发文量

97

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: