{"title":"隔夜利率超过随机连续性的期限结构建模","authors":"Claudio Fontana, Zorana Grbac, Thorsten Schmidt","doi":"10.1111/mafi.12415","DOIUrl":null,"url":null,"abstract":"<p>Overnight rates, such as the Secured Overnight Financing Rate (SOFR) in the United States, are central to the current reform of interest rate benchmarks. A striking feature of overnight rates is the presence of jumps and spikes occurring at predetermined dates due to monetary policy interventions and liquidity constraints. This corresponds to stochastic discontinuities (i.e., discontinuities occurring at ex ante known points in time) in their dynamics. In this work, we propose a term structure modeling framework based on overnight rates and characterize absence of arbitrage in a generalized Heath–Jarrow–Morton (HJM) setting. We extend the classical short-rate approach to accommodate stochastic discontinuities, developing a tractable setup driven by affine semimartingales. In this context, we show that simple specifications allow to capture stylized facts of the jump behavior of overnight rates. In a Gaussian setting, we provide explicit valuation formulas for bonds and caplets. Furthermore, we investigate hedging in the sense of local risk-minimization when the underlying term structures feature stochastic discontinuities.</p>","PeriodicalId":49867,"journal":{"name":"Mathematical Finance","volume":"34 1","pages":"151-189"},"PeriodicalIF":2.4000,"publicationDate":"2023-08-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/mafi.12415","citationCount":"0","resultStr":"{\"title\":\"Term structure modeling with overnight rates beyond stochastic continuity\",\"authors\":\"Claudio Fontana, Zorana Grbac, Thorsten Schmidt\",\"doi\":\"10.1111/mafi.12415\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Overnight rates, such as the Secured Overnight Financing Rate (SOFR) in the United States, are central to the current reform of interest rate benchmarks. A striking feature of overnight rates is the presence of jumps and spikes occurring at predetermined dates due to monetary policy interventions and liquidity constraints. This corresponds to stochastic discontinuities (i.e., discontinuities occurring at ex ante known points in time) in their dynamics. In this work, we propose a term structure modeling framework based on overnight rates and characterize absence of arbitrage in a generalized Heath–Jarrow–Morton (HJM) setting. We extend the classical short-rate approach to accommodate stochastic discontinuities, developing a tractable setup driven by affine semimartingales. In this context, we show that simple specifications allow to capture stylized facts of the jump behavior of overnight rates. In a Gaussian setting, we provide explicit valuation formulas for bonds and caplets. Furthermore, we investigate hedging in the sense of local risk-minimization when the underlying term structures feature stochastic discontinuities.</p>\",\"PeriodicalId\":49867,\"journal\":{\"name\":\"Mathematical Finance\",\"volume\":\"34 1\",\"pages\":\"151-189\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2023-08-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/mafi.12415\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Mathematical Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/mafi.12415\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematical Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/mafi.12415","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Term structure modeling with overnight rates beyond stochastic continuity

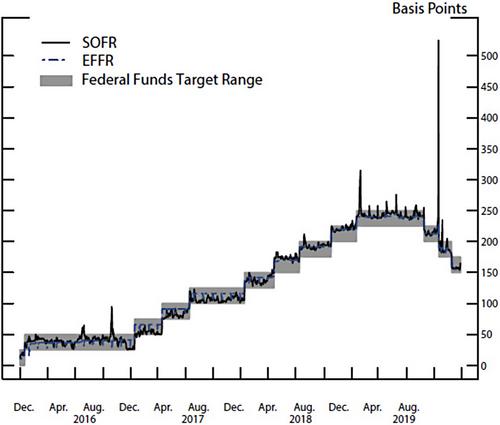

Overnight rates, such as the Secured Overnight Financing Rate (SOFR) in the United States, are central to the current reform of interest rate benchmarks. A striking feature of overnight rates is the presence of jumps and spikes occurring at predetermined dates due to monetary policy interventions and liquidity constraints. This corresponds to stochastic discontinuities (i.e., discontinuities occurring at ex ante known points in time) in their dynamics. In this work, we propose a term structure modeling framework based on overnight rates and characterize absence of arbitrage in a generalized Heath–Jarrow–Morton (HJM) setting. We extend the classical short-rate approach to accommodate stochastic discontinuities, developing a tractable setup driven by affine semimartingales. In this context, we show that simple specifications allow to capture stylized facts of the jump behavior of overnight rates. In a Gaussian setting, we provide explicit valuation formulas for bonds and caplets. Furthermore, we investigate hedging in the sense of local risk-minimization when the underlying term structures feature stochastic discontinuities.

期刊介绍:

Mathematical Finance seeks to publish original research articles focused on the development and application of novel mathematical and statistical methods for the analysis of financial problems.

The journal welcomes contributions on new statistical methods for the analysis of financial problems. Empirical results will be appropriate to the extent that they illustrate a statistical technique, validate a model or provide insight into a financial problem. Papers whose main contribution rests on empirical results derived with standard approaches will not be considered.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: