{"title":"基于情绪的房地产市场压力和系统性风险指标:国际证据","authors":"Mikhail Stolbov, Maria Shchepeleva","doi":"10.1007/s10436-023-00429-y","DOIUrl":null,"url":null,"abstract":"<div><p>We propose sentiment-based indicators of real estate market stress for the USA, the UK, Canada, Australia, India, and on the global scale. The global and country-level indicators are based on a novel methodology synthesizing textual analysis of real estate research and Google search data. Using mixed frequency vector autoregressions, we show that in the USA, the UK, Australia and India, the sentiment-based indicators are found to mediate the relationship between real estate prices and systemic financial risk. In particular, for the UK, there is a vicious circle involving the interaction among the three variables: the sentiment-based indicator of real estate market stress unidirectionally leads systemic risk, the latter impacts real estate prices, whereas the prices drive the stress sentiment. Canada appears the only sample country where real estate market stress sentiment is unrelated to real estate prices and systemic risk. On the global scale, there is a bi-directional linkage between the stress sentiment and real estate prices. Overall, our empirical findings suggest that policymakers and real estate market participants should account for sentiment regarding real estate market stress in their decision-making.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"19 3","pages":"355 - 382"},"PeriodicalIF":0.7000,"publicationDate":"2023-06-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Sentiment-based indicators of real estate market stress and systemic risk: international evidence\",\"authors\":\"Mikhail Stolbov, Maria Shchepeleva\",\"doi\":\"10.1007/s10436-023-00429-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>We propose sentiment-based indicators of real estate market stress for the USA, the UK, Canada, Australia, India, and on the global scale. The global and country-level indicators are based on a novel methodology synthesizing textual analysis of real estate research and Google search data. Using mixed frequency vector autoregressions, we show that in the USA, the UK, Australia and India, the sentiment-based indicators are found to mediate the relationship between real estate prices and systemic financial risk. In particular, for the UK, there is a vicious circle involving the interaction among the three variables: the sentiment-based indicator of real estate market stress unidirectionally leads systemic risk, the latter impacts real estate prices, whereas the prices drive the stress sentiment. Canada appears the only sample country where real estate market stress sentiment is unrelated to real estate prices and systemic risk. On the global scale, there is a bi-directional linkage between the stress sentiment and real estate prices. Overall, our empirical findings suggest that policymakers and real estate market participants should account for sentiment regarding real estate market stress in their decision-making.</p></div>\",\"PeriodicalId\":45289,\"journal\":{\"name\":\"Annals of Finance\",\"volume\":\"19 3\",\"pages\":\"355 - 382\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2023-06-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10436-023-00429-y\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-023-00429-y","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Sentiment-based indicators of real estate market stress and systemic risk: international evidence

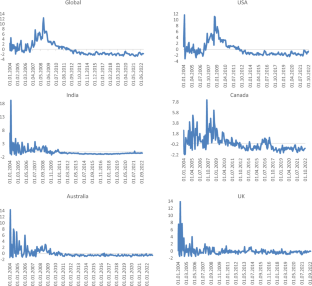

We propose sentiment-based indicators of real estate market stress for the USA, the UK, Canada, Australia, India, and on the global scale. The global and country-level indicators are based on a novel methodology synthesizing textual analysis of real estate research and Google search data. Using mixed frequency vector autoregressions, we show that in the USA, the UK, Australia and India, the sentiment-based indicators are found to mediate the relationship between real estate prices and systemic financial risk. In particular, for the UK, there is a vicious circle involving the interaction among the three variables: the sentiment-based indicator of real estate market stress unidirectionally leads systemic risk, the latter impacts real estate prices, whereas the prices drive the stress sentiment. Canada appears the only sample country where real estate market stress sentiment is unrelated to real estate prices and systemic risk. On the global scale, there is a bi-directional linkage between the stress sentiment and real estate prices. Overall, our empirical findings suggest that policymakers and real estate market participants should account for sentiment regarding real estate market stress in their decision-making.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: