{"title":"小型慈善机构财务报表审计及复核的决定因素及质素","authors":"Yitang (Jenny) Yang, Roger Simnett","doi":"10.1111/ijau.12310","DOIUrl":null,"url":null,"abstract":"<p>Using a random sample of 500 Australian small charities, we first identified the determinants for the 56 charities disclosing audit/review reports (53 audits and three reviews) from the 110 voluntarily lodging annual reports. Sequential logistic regression showed that lodging charities are larger, rely more on government grants and use accrual accounting, while factors explaining the disclosure of audit/review reports are charities' deductible gift recipient status, organizational age, and again the use of accrual accounting. Second, for the 53 audit engagements identified, we examined audit quality using five measures and identified significant concerns, including only 34% fully complying with the reporting requirements of Australian/International Auditing Standard 700. Third, tracing the 500 charities from 2014 to 2018, plus 100 more of the largest public-interest small charities, little change was identified in provision of audits versus reviews. The implications of our findings for charities, audit firms, regulators and standard-setters were considered.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"27 4","pages":"220-240"},"PeriodicalIF":1.4000,"publicationDate":"2023-03-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12310","citationCount":"1","resultStr":"{\"title\":\"Determinants and quality of audits and reviews of small charities financial statements\",\"authors\":\"Yitang (Jenny) Yang, Roger Simnett\",\"doi\":\"10.1111/ijau.12310\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Using a random sample of 500 Australian small charities, we first identified the determinants for the 56 charities disclosing audit/review reports (53 audits and three reviews) from the 110 voluntarily lodging annual reports. Sequential logistic regression showed that lodging charities are larger, rely more on government grants and use accrual accounting, while factors explaining the disclosure of audit/review reports are charities' deductible gift recipient status, organizational age, and again the use of accrual accounting. Second, for the 53 audit engagements identified, we examined audit quality using five measures and identified significant concerns, including only 34% fully complying with the reporting requirements of Australian/International Auditing Standard 700. Third, tracing the 500 charities from 2014 to 2018, plus 100 more of the largest public-interest small charities, little change was identified in provision of audits versus reviews. The implications of our findings for charities, audit firms, regulators and standard-setters were considered.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"27 4\",\"pages\":\"220-240\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-03-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12310\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12310\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12310","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Determinants and quality of audits and reviews of small charities financial statements

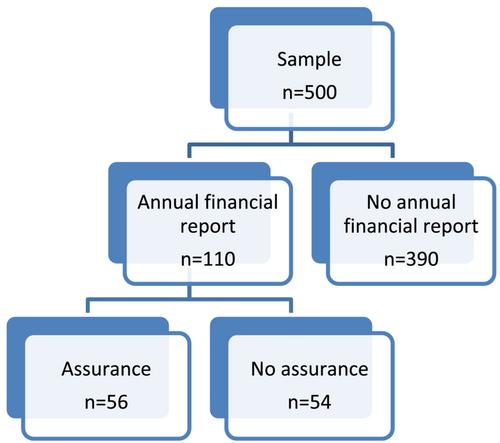

Using a random sample of 500 Australian small charities, we first identified the determinants for the 56 charities disclosing audit/review reports (53 audits and three reviews) from the 110 voluntarily lodging annual reports. Sequential logistic regression showed that lodging charities are larger, rely more on government grants and use accrual accounting, while factors explaining the disclosure of audit/review reports are charities' deductible gift recipient status, organizational age, and again the use of accrual accounting. Second, for the 53 audit engagements identified, we examined audit quality using five measures and identified significant concerns, including only 34% fully complying with the reporting requirements of Australian/International Auditing Standard 700. Third, tracing the 500 charities from 2014 to 2018, plus 100 more of the largest public-interest small charities, little change was identified in provision of audits versus reviews. The implications of our findings for charities, audit firms, regulators and standard-setters were considered.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: