{"title":"哈罗德•苏黎世(Harold Zurcher)到底是不是近视了?复制Rust的引擎更换估算","authors":"Christopher Ferrall","doi":"10.1002/jae.3001","DOIUrl":null,"url":null,"abstract":"<p>Rust (1987) studies the dynamic decision making under uncertainty made by Harold Zurcher to replace bus engines. In the decades since, the model has been applied, extended, and used as an example multiple times. This paper resolves some discrepancies in how data were transformed in the original and subsequent archives. Using a package that standardizes computation of estimated dynamic programming, it replicates the 12 original maximum likelihood estimates and the six main hypothesis tests of whether Zurcher's decisions were myopic or not. The discrepancy in the data processing results in modest differences in estimates and log-likelihoods, but the <i>p</i>-values are essentially the same because the differences are very similar across values of the discount factor in the tests.</p>","PeriodicalId":48363,"journal":{"name":"Journal of Applied Econometrics","volume":"38 7","pages":"1093-1100"},"PeriodicalIF":2.3000,"publicationDate":"2023-08-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3001","citationCount":"1","resultStr":"{\"title\":\"Was Harold Zurcher myopic after all? Replicating Rust's engine replacement estimates\",\"authors\":\"Christopher Ferrall\",\"doi\":\"10.1002/jae.3001\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Rust (1987) studies the dynamic decision making under uncertainty made by Harold Zurcher to replace bus engines. In the decades since, the model has been applied, extended, and used as an example multiple times. This paper resolves some discrepancies in how data were transformed in the original and subsequent archives. Using a package that standardizes computation of estimated dynamic programming, it replicates the 12 original maximum likelihood estimates and the six main hypothesis tests of whether Zurcher's decisions were myopic or not. The discrepancy in the data processing results in modest differences in estimates and log-likelihoods, but the <i>p</i>-values are essentially the same because the differences are very similar across values of the discount factor in the tests.</p>\",\"PeriodicalId\":48363,\"journal\":{\"name\":\"Journal of Applied Econometrics\",\"volume\":\"38 7\",\"pages\":\"1093-1100\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2023-08-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3001\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Applied Econometrics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jae.3001\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Econometrics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jae.3001","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Was Harold Zurcher myopic after all? Replicating Rust's engine replacement estimates

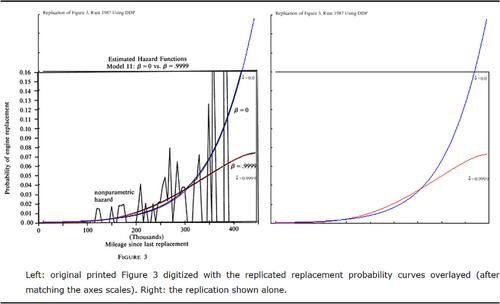

Rust (1987) studies the dynamic decision making under uncertainty made by Harold Zurcher to replace bus engines. In the decades since, the model has been applied, extended, and used as an example multiple times. This paper resolves some discrepancies in how data were transformed in the original and subsequent archives. Using a package that standardizes computation of estimated dynamic programming, it replicates the 12 original maximum likelihood estimates and the six main hypothesis tests of whether Zurcher's decisions were myopic or not. The discrepancy in the data processing results in modest differences in estimates and log-likelihoods, but the p-values are essentially the same because the differences are very similar across values of the discount factor in the tests.

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: