{"title":"企业声誉和利益相关者参与:保证质量和保证属性重要吗?","authors":"Isabel-María García-Sánchez, Nicola Raimo, María-Victoria Uribe-Bohorquez, Filippo Vitolla","doi":"10.1111/ijau.12287","DOIUrl":null,"url":null,"abstract":"<p>The objective of this research is to determine the impact that sustainability assurance services have on corporate reputation and stakeholder engagement, delving into the differentiating effect of certain attributes of the assurer and the quality level of the assurance. After an initial exploratory analysis in which the added value that the assurance service has on the external business image and on the relationships with stakeholders is evidenced, the results obtained for a sample of 604 multinational corporations for the period 2011–2017 show the existence of a reputational advantage for those companies that have contracted for a higher quality assurance service. On the contrary, the attributes of the assurer have no direct and indirect effect on corporate reputation unless the assurer is an auditor, which favours a higher quality of assurance service and indirectly affects the probability that the company will be included in a reputation ranking. The intrinsic characteristics of this service do not translate into active stakeholder engagement. From a theoretical and practical point of view, this evidence contributes to the knowledge of the effect of assurance on stakeholder engagement and corporate reputation by improving the climate of trust around the company's disclosure.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"26 3","pages":"388-403"},"PeriodicalIF":1.4000,"publicationDate":"2022-06-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12287","citationCount":"7","resultStr":"{\"title\":\"Corporate reputation and stakeholder engagement: Do assurance quality and assurer attributes matter?\",\"authors\":\"Isabel-María García-Sánchez, Nicola Raimo, María-Victoria Uribe-Bohorquez, Filippo Vitolla\",\"doi\":\"10.1111/ijau.12287\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The objective of this research is to determine the impact that sustainability assurance services have on corporate reputation and stakeholder engagement, delving into the differentiating effect of certain attributes of the assurer and the quality level of the assurance. After an initial exploratory analysis in which the added value that the assurance service has on the external business image and on the relationships with stakeholders is evidenced, the results obtained for a sample of 604 multinational corporations for the period 2011–2017 show the existence of a reputational advantage for those companies that have contracted for a higher quality assurance service. On the contrary, the attributes of the assurer have no direct and indirect effect on corporate reputation unless the assurer is an auditor, which favours a higher quality of assurance service and indirectly affects the probability that the company will be included in a reputation ranking. The intrinsic characteristics of this service do not translate into active stakeholder engagement. From a theoretical and practical point of view, this evidence contributes to the knowledge of the effect of assurance on stakeholder engagement and corporate reputation by improving the climate of trust around the company's disclosure.</p>\",\"PeriodicalId\":47092,\"journal\":{\"name\":\"International Journal of Auditing\",\"volume\":\"26 3\",\"pages\":\"388-403\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2022-06-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12287\",\"citationCount\":\"7\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Journal of Auditing\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12287\",\"RegionNum\":4,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12287","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Corporate reputation and stakeholder engagement: Do assurance quality and assurer attributes matter?

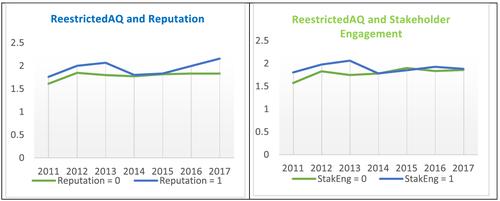

The objective of this research is to determine the impact that sustainability assurance services have on corporate reputation and stakeholder engagement, delving into the differentiating effect of certain attributes of the assurer and the quality level of the assurance. After an initial exploratory analysis in which the added value that the assurance service has on the external business image and on the relationships with stakeholders is evidenced, the results obtained for a sample of 604 multinational corporations for the period 2011–2017 show the existence of a reputational advantage for those companies that have contracted for a higher quality assurance service. On the contrary, the attributes of the assurer have no direct and indirect effect on corporate reputation unless the assurer is an auditor, which favours a higher quality of assurance service and indirectly affects the probability that the company will be included in a reputation ranking. The intrinsic characteristics of this service do not translate into active stakeholder engagement. From a theoretical and practical point of view, this evidence contributes to the knowledge of the effect of assurance on stakeholder engagement and corporate reputation by improving the climate of trust around the company's disclosure.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: