Lori Shefchik Bhaskar, Tracie M. Majors, Adam Vitalis

{"title":"损耗如何与审计师的怀疑倾向相互作用,从而影响审计师在谈判中对管理者的挑战?","authors":"Lori Shefchik Bhaskar, Tracie M. Majors, Adam Vitalis","doi":"10.1111/1911-3846.12891","DOIUrl":null,"url":null,"abstract":"<p>We use multiple methods to examine how depletion and auditors' skeptical dispositions interact to affect auditors' challenging of managers in negotiations over financial statement amounts. We expect auditors are likely depleted from effortfully exercising self-regulation during the busy times when these negotiations occur. Individuals in a depleted state tilt toward natural, less effortful behaviors. Thus, we posit that the effects of depletion will diverge depending on the auditor's skeptical disposition—a determinant of how natural or effortful they will find the skeptical behaviors (e.g., challenging) versus client service behaviors (e.g., maintaining the client relationship and audit efficiency) required for negotiations. We predict that client service auditors (i.e., low skeptics) will challenge managers less in negotiations when depleted versus non-depleted, while high skeptic auditors will challenge more when depleted. We test this interactive prediction in an abstract experiment where we manipulate depletion and measure auditors' skeptical dispositions using trait skepticism. Findings support our predictions. We also develop a new measure of auditors' client service–skeptic disposition based on the skepticism literature that adds nuance to the traditional lower versus higher skeptic labels. In a second study, interviews with audit partners validate the realism of our depletion and client service–skeptic constructs and corroborate our experimental findings. Our study sheds light on depletion effects in auditors' negotiations with their clients and how the effects differ based on auditor personalities.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"40 4","pages":"2288-2313"},"PeriodicalIF":3.2000,"publicationDate":"2023-08-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12891","citationCount":"0","resultStr":"{\"title\":\"How does depletion interact with auditors' skeptical dispositions to affect auditors' challenging of managers in negotiations?\",\"authors\":\"Lori Shefchik Bhaskar, Tracie M. Majors, Adam Vitalis\",\"doi\":\"10.1111/1911-3846.12891\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We use multiple methods to examine how depletion and auditors' skeptical dispositions interact to affect auditors' challenging of managers in negotiations over financial statement amounts. We expect auditors are likely depleted from effortfully exercising self-regulation during the busy times when these negotiations occur. Individuals in a depleted state tilt toward natural, less effortful behaviors. Thus, we posit that the effects of depletion will diverge depending on the auditor's skeptical disposition—a determinant of how natural or effortful they will find the skeptical behaviors (e.g., challenging) versus client service behaviors (e.g., maintaining the client relationship and audit efficiency) required for negotiations. We predict that client service auditors (i.e., low skeptics) will challenge managers less in negotiations when depleted versus non-depleted, while high skeptic auditors will challenge more when depleted. We test this interactive prediction in an abstract experiment where we manipulate depletion and measure auditors' skeptical dispositions using trait skepticism. Findings support our predictions. We also develop a new measure of auditors' client service–skeptic disposition based on the skepticism literature that adds nuance to the traditional lower versus higher skeptic labels. In a second study, interviews with audit partners validate the realism of our depletion and client service–skeptic constructs and corroborate our experimental findings. Our study sheds light on depletion effects in auditors' negotiations with their clients and how the effects differ based on auditor personalities.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"40 4\",\"pages\":\"2288-2313\"},\"PeriodicalIF\":3.2000,\"publicationDate\":\"2023-08-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12891\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12891\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12891","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

How does depletion interact with auditors' skeptical dispositions to affect auditors' challenging of managers in negotiations?

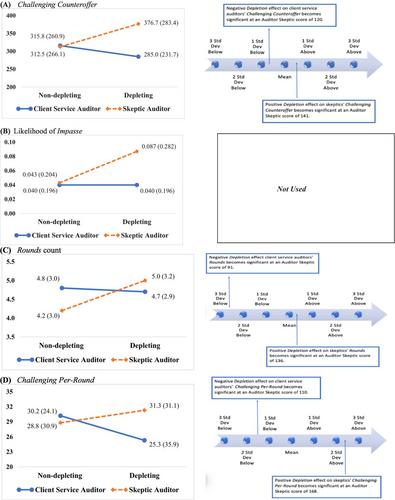

We use multiple methods to examine how depletion and auditors' skeptical dispositions interact to affect auditors' challenging of managers in negotiations over financial statement amounts. We expect auditors are likely depleted from effortfully exercising self-regulation during the busy times when these negotiations occur. Individuals in a depleted state tilt toward natural, less effortful behaviors. Thus, we posit that the effects of depletion will diverge depending on the auditor's skeptical disposition—a determinant of how natural or effortful they will find the skeptical behaviors (e.g., challenging) versus client service behaviors (e.g., maintaining the client relationship and audit efficiency) required for negotiations. We predict that client service auditors (i.e., low skeptics) will challenge managers less in negotiations when depleted versus non-depleted, while high skeptic auditors will challenge more when depleted. We test this interactive prediction in an abstract experiment where we manipulate depletion and measure auditors' skeptical dispositions using trait skepticism. Findings support our predictions. We also develop a new measure of auditors' client service–skeptic disposition based on the skepticism literature that adds nuance to the traditional lower versus higher skeptic labels. In a second study, interviews with audit partners validate the realism of our depletion and client service–skeptic constructs and corroborate our experimental findings. Our study sheds light on depletion effects in auditors' negotiations with their clients and how the effects differ based on auditor personalities.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: