税收抵免有利于慈善机构吗?来自两个州的证据

IF 1.7

4区 经济学

Q2 ECONOMICS

引用次数: 0

摘要

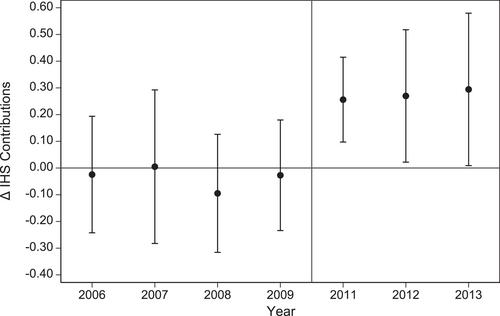

本文考虑了国家慈善捐赠税收抵免对符合条件的慈善机构捐款收入的影响。使用事件研究和990表格数据,我们发现在密歇根州取消每个纳税人100美元的信贷后,对合格非营利组织的捐款没有显著变化。相比之下,我们发现,在北达科他州引入了持续数年的每个纳税人10000美元的信贷后,对合格慈善机构的捐款大幅增加。研究结果表明,对慈善捐赠税收抵免设置较大上限会引发更强烈的捐助者反应。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Do tax credits benefit charities? Evidence from two states

This paper considers the effect of state charitable giving tax credits on the contribution revenues of eligible charities. Using event studies paired with Form 990 data, we detect no significant change in contributions to qualified nonprofits after the elimination of a $100 per taxpayer credit by Michigan. By contrast, we find a significant increase in contributions to qualified charities following the introduction of a $10,000 per taxpayer credit by North Dakota that persists for several years. The results suggest that placing a large cap on charitable giving tax credits induces stronger donor responses.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Contemporary Economic Policy

Multiple-

CiteScore

3.10

自引率

6.70%

发文量

38

期刊介绍:

Contemporary Economic Policy publishes scholarly economic research and analysis on issues of vital concern to business, government, and other decision makers. Leading western scholars, including three Nobel laureates, are among CEP"s authors. The objectives are to communicate results of high quality economic analysis to policymakers, focus high quality research and analysis on current policy issues of widespread concern, increase knowledge among economists of features of the economy key to understanding the impact of policy, and to advance methods of policy analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: