{"title":"投资组合选择中的共同跳跃和递归偏好","authors":"Immacolata Oliva, Ilaria Stefani","doi":"10.1007/s10436-023-00425-2","DOIUrl":null,"url":null,"abstract":"<div><p>This paper investigates a multivariate, dynamic, continuous-time optimal consumption and portfolio allocation problem when the investor faces recursive utilities. The economy we are considering is described through both diffusion and discontinuities in the dynamics. We derive an approximated closed-form solution to optimal rules by exploiting standard dynamic programming techniques. Our findings are manifold. First, we obtain dynamic optimal weights, inversely proportional to volatility. Second, we show that both co-jumps frequency and intensity play a crucial role, as they considerably limit potential losses in the investors’ wealth. Third, we prove that jumps in precision reinforce the effect of jumps in price, further reducing optimal allocation. Finally, we highlight how co-jumps may influence investors’ choices regarding intertemporal consumption.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"19 3","pages":"291 - 324"},"PeriodicalIF":0.7000,"publicationDate":"2023-02-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s10436-023-00425-2.pdf","citationCount":"0","resultStr":"{\"title\":\"Co-jumps and recursive preferences in portfolio choices\",\"authors\":\"Immacolata Oliva, Ilaria Stefani\",\"doi\":\"10.1007/s10436-023-00425-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This paper investigates a multivariate, dynamic, continuous-time optimal consumption and portfolio allocation problem when the investor faces recursive utilities. The economy we are considering is described through both diffusion and discontinuities in the dynamics. We derive an approximated closed-form solution to optimal rules by exploiting standard dynamic programming techniques. Our findings are manifold. First, we obtain dynamic optimal weights, inversely proportional to volatility. Second, we show that both co-jumps frequency and intensity play a crucial role, as they considerably limit potential losses in the investors’ wealth. Third, we prove that jumps in precision reinforce the effect of jumps in price, further reducing optimal allocation. Finally, we highlight how co-jumps may influence investors’ choices regarding intertemporal consumption.</p></div>\",\"PeriodicalId\":45289,\"journal\":{\"name\":\"Annals of Finance\",\"volume\":\"19 3\",\"pages\":\"291 - 324\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2023-02-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://link.springer.com/content/pdf/10.1007/s10436-023-00425-2.pdf\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10436-023-00425-2\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-023-00425-2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Co-jumps and recursive preferences in portfolio choices

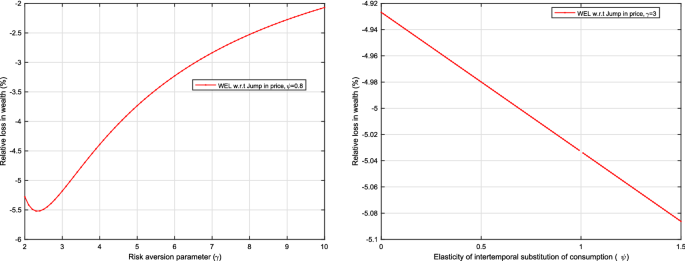

This paper investigates a multivariate, dynamic, continuous-time optimal consumption and portfolio allocation problem when the investor faces recursive utilities. The economy we are considering is described through both diffusion and discontinuities in the dynamics. We derive an approximated closed-form solution to optimal rules by exploiting standard dynamic programming techniques. Our findings are manifold. First, we obtain dynamic optimal weights, inversely proportional to volatility. Second, we show that both co-jumps frequency and intensity play a crucial role, as they considerably limit potential losses in the investors’ wealth. Third, we prove that jumps in precision reinforce the effect of jumps in price, further reducing optimal allocation. Finally, we highlight how co-jumps may influence investors’ choices regarding intertemporal consumption.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: