Katharina Gangl, Eva Hofmann, Barbara Hartl, Mihály Berkics

{"title":"强势当局和守信纳税人的影响:来自奥地利、芬兰和匈牙利的扩展滑坡框架证据。","authors":"Katharina Gangl, Eva Hofmann, Barbara Hartl, Mihály Berkics","doi":"10.1080/01442872.2019.1577375","DOIUrl":null,"url":null,"abstract":"<p><p>Tax authorities utilize a wide range of instruments to motivate honest taxpaying ranging from strict audits to fair procedures or personalized support, differing from country to country. However, little is known about how these different instruments and taxpayers' trust influence the generation of interaction climates between tax authorities and taxpayers, motivations to comply, and particularly, tax compliance. The present research examines the extended slippery slope framework (eSSF), which distinguishes tax authorities' instruments into different qualities of power of authority (coercive and legitimate) and trust in authorities (reason-based and implicit), to shed light on the effect of differences between power and trust. We test eSSF assumptions with survey data from taxpayers from three culturally different countries (<i>N</i> = 700) who also vary concerning their perceptions of power, trust, interaction climates, and tax motivations. Results support assumptions of the eSSF. Across all countries, the relation of coercive power and tax compliance was mediated by implicit trust. The connection from legitimate power to tax compliance is partially mediated by reason-based trust. The relationship between implicit trust and tax compliance is mediated by a confidence climate and committed cooperation. Theoretical and practical implications are discussed.</p>","PeriodicalId":93043,"journal":{"name":"Policy studies (Policy Studies Institute)","volume":"41 1","pages":"98-111"},"PeriodicalIF":2.3000,"publicationDate":"2019-02-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7194257/pdf/","citationCount":"0","resultStr":"{\"title\":\"The impact of powerful authorities and trustful taxpayers: evidence for the extended slippery slope framework from Austria, Finland, and Hungary.\",\"authors\":\"Katharina Gangl, Eva Hofmann, Barbara Hartl, Mihály Berkics\",\"doi\":\"10.1080/01442872.2019.1577375\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Tax authorities utilize a wide range of instruments to motivate honest taxpaying ranging from strict audits to fair procedures or personalized support, differing from country to country. However, little is known about how these different instruments and taxpayers' trust influence the generation of interaction climates between tax authorities and taxpayers, motivations to comply, and particularly, tax compliance. The present research examines the extended slippery slope framework (eSSF), which distinguishes tax authorities' instruments into different qualities of power of authority (coercive and legitimate) and trust in authorities (reason-based and implicit), to shed light on the effect of differences between power and trust. We test eSSF assumptions with survey data from taxpayers from three culturally different countries (<i>N</i> = 700) who also vary concerning their perceptions of power, trust, interaction climates, and tax motivations. Results support assumptions of the eSSF. Across all countries, the relation of coercive power and tax compliance was mediated by implicit trust. The connection from legitimate power to tax compliance is partially mediated by reason-based trust. The relationship between implicit trust and tax compliance is mediated by a confidence climate and committed cooperation. Theoretical and practical implications are discussed.</p>\",\"PeriodicalId\":93043,\"journal\":{\"name\":\"Policy studies (Policy Studies Institute)\",\"volume\":\"41 1\",\"pages\":\"98-111\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2019-02-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7194257/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Policy studies (Policy Studies Institute)\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1080/01442872.2019.1577375\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2020/1/1 0:00:00\",\"PubModel\":\"eCollection\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Policy studies (Policy Studies Institute)","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1080/01442872.2019.1577375","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2020/1/1 0:00:00","PubModel":"eCollection","JCR":"","JCRName":"","Score":null,"Total":0}

The impact of powerful authorities and trustful taxpayers: evidence for the extended slippery slope framework from Austria, Finland, and Hungary.

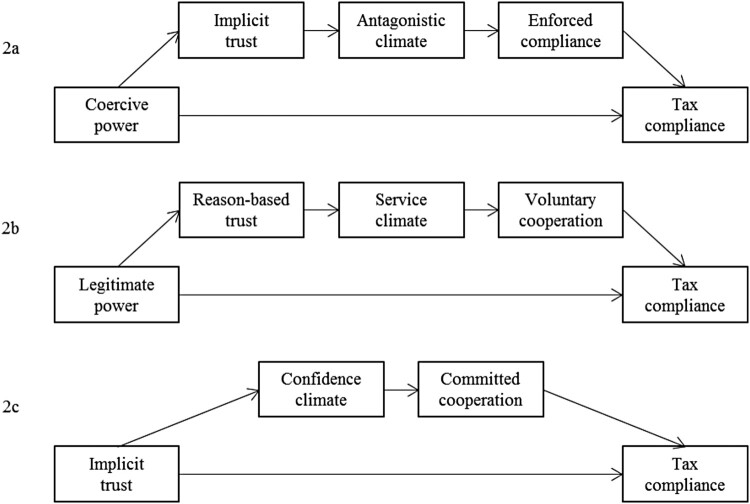

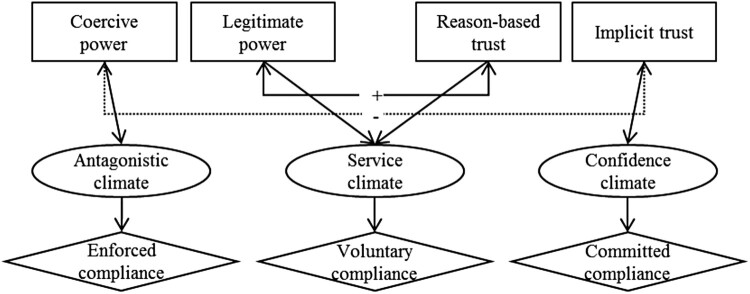

Tax authorities utilize a wide range of instruments to motivate honest taxpaying ranging from strict audits to fair procedures or personalized support, differing from country to country. However, little is known about how these different instruments and taxpayers' trust influence the generation of interaction climates between tax authorities and taxpayers, motivations to comply, and particularly, tax compliance. The present research examines the extended slippery slope framework (eSSF), which distinguishes tax authorities' instruments into different qualities of power of authority (coercive and legitimate) and trust in authorities (reason-based and implicit), to shed light on the effect of differences between power and trust. We test eSSF assumptions with survey data from taxpayers from three culturally different countries (N = 700) who also vary concerning their perceptions of power, trust, interaction climates, and tax motivations. Results support assumptions of the eSSF. Across all countries, the relation of coercive power and tax compliance was mediated by implicit trust. The connection from legitimate power to tax compliance is partially mediated by reason-based trust. The relationship between implicit trust and tax compliance is mediated by a confidence climate and committed cooperation. Theoretical and practical implications are discussed.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: