基于随机PPA组合优化的脱碳玻璃厂绿色制氢成本与减排潜力评估

IF 7.6

Q1 ENERGY & FUELS

引用次数: 0

摘要

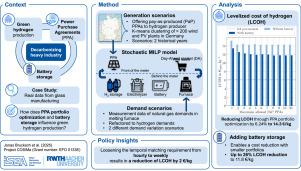

重工业的脱碳需要大量的绿色氢。为了通过电解生产绿色氢,欧盟的可再生能源指令II规定了确保使用可再生电力的规则。氢气生产商可以使用电力购买协议(PPAs)组合来购买可再生电力。这些投资组合必须经济有效地满足氢需求,而电池储能可以通过转移过剩的可再生能源发电来提供帮助。然而,未来电力价格和需求的高度不确定性使最佳投资组合设计复杂化。目前的文献缺乏全面的模型来评估不确定性下包括电池存储在内的现实案例研究的投资组合优化。这项工作通过引入适合工业应用的随机混合整数线性规划模型来解决这一差距。我们使用德国的一个真实的玻璃制造基地来演示该模型。我们的研究结果表明,在欧盟规则下,仅投资组合优化就可以将氢的平准化成本(LCOH)降低6.24%。增加电池进一步降低了成本,实现了11.8€2024 kg - 1的LCOH。探索不同的时间匹配方案表明,每周匹配减少LCOH 2€2024kg - 1,同时保持较高的可再生能源份额。该模型为在各种工业环境中优化PPA组合提供了一个灵活的工具。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Evaluating cost and emission reduction potentials with stochastic PPA portfolio optimization for green hydrogen production in a decarbonized glassworks

The decarbonization of heavy industries demands large volumes of green hydrogen. To produce green hydrogen via electrolysis, the EU’s Renewable Energy Directive II imposes rules to ensure the use of renewable electricity. Hydrogen producers can use portfolios of power purchase agreements (PPAs) to buy renewable electricity. These portfolios must meet hydrogen demand cost-effectively, and battery storage can help by shifting excess renewable generation. However, high uncertainty around future electricity prices and demand complicates optimal portfolio design. Current literature lacks comprehensive models that evaluate such portfolio optimization under uncertainty for real-world case studies including battery storage. This work addresses the gap by introducing a stochastic mixed-integer linear programming model tailored to industrial applications. We demonstrate the model using a real-world glass manufacturing site in Germany. Our findings show that portfolio optimization alone can reduce the levelized cost of hydrogen (LCOH) by 6.24% under EU rules. Adding a battery further cuts costs, achieving an LCOH of 11.8 €2024 kg−1. Exploring different temporal matching schemes reveals that weekly matching reduces LCOH by 2 €2024kg−1 while maintaining a high share of renewable energy. The model offers a flexible tool for optimizing PPA portfolios in various industrial settings.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Energy Conversion and Management-X

Multiple-

CiteScore

8.80

自引率

3.20%

发文量

180

审稿时长

58 days

期刊介绍:

Energy Conversion and Management: X is the open access extension of the reputable journal Energy Conversion and Management, serving as a platform for interdisciplinary research on a wide array of critical energy subjects. The journal is dedicated to publishing original contributions and in-depth technical review articles that present groundbreaking research on topics spanning energy generation, utilization, conversion, storage, transmission, conservation, management, and sustainability.

The scope of Energy Conversion and Management: X encompasses various forms of energy, including mechanical, thermal, nuclear, chemical, electromagnetic, magnetic, and electric energy. It addresses all known energy resources, highlighting both conventional sources like fossil fuels and nuclear power, as well as renewable resources such as solar, biomass, hydro, wind, geothermal, and ocean energy.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: