加密货币、股票、债券、汇率和商品的复杂系统和PS-LSTM预测

IF 3.1

3区 物理与天体物理

Q2 PHYSICS, MULTIDISCIPLINARY

Physica A: Statistical Mechanics and its Applications

Pub Date : 2025-09-18

DOI:10.1016/j.physa.2025.130976

引用次数: 0

摘要

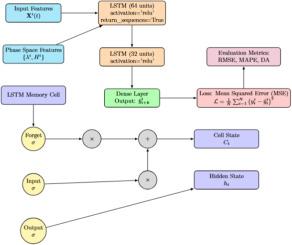

本研究运用相空间重构和相空间LSTM分析了比特币与黄金、标准普尔500指数、美国债券、欧元/美元和原油的相互作用,揭示了金融市场中隐藏的依赖关系和混乱结构。研究实现了一个多方法验证框架,该框架结合了Lyapunov指数估计的Rosenstein算法、混沌的0 - 1检验和BDS检验,为确定性混沌提供了可靠的证据。结果表明,大多数资产表现出确定性混沌,价格演变对流动性条件和宏观经济力量高度敏感。在最佳四维嵌入中进行的相空间分析揭示了比特币与美国债券之间更强的预测联系,加强了其对全球金融状况的日益依赖。PS-LSTM的应用显著提高了预测的准确性,通过严格的验证,包括统计显著性检验和使用风险调整绩效指标的经济显著性评价。这些发现表明,加密货币不是孤立的资产,而是与系统性金融波动深深纠缠在一起,有必要通过统计力学和经济物理学的视角重新评估市场稳定性和风险传播。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Complex system and PS-LSTM prediction of cryptocurrencies, stocks, bonds, exchange rates and commodities

This study applies Phase Space Reconstruction and Phase Space LSTM to analyze Bitcoin’s interactions with Gold, S&P 500, U.S. Bonds, EUR/USD, and Crude Oil, revealing hidden dependencies and chaotic structures in financial markets. Study implement a multi-method validation framework combining the Rosenstein algorithm for Lyapunov exponent estimation, test for chaos and BDS test to provide robust evidence for deterministic chaos. Results indicate that most assets exhibit deterministic chaos, with price evolution highly sensitive to liquidity conditions and macroeconomic forces. Phase space analysis conducted in optimal four-dimensional embeddings uncovers stronger predictive linkages between Bitcoin and U.S. Bonds, reinforcing its growing dependence on global financial conditions. The application of PS-LSTM significantly enhances forecasting accuracy, demonstrated through rigorous validation including statistical significance testing and economic significance evaluation using risk-adjusted performance metrics. These findings suggest that cryptocurrencies are not isolated assets but deeply entangled with systemic financial fluctuations, necessitating a reassessment of market stability and risk propagation through the lens of statistical mechanics and econophysics.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

CiteScore

7.20

自引率

9.10%

发文量

852

审稿时长

6.6 months

期刊介绍:

Physica A: Statistical Mechanics and its Applications

Recognized by the European Physical Society

Physica A publishes research in the field of statistical mechanics and its applications.

Statistical mechanics sets out to explain the behaviour of macroscopic systems by studying the statistical properties of their microscopic constituents.

Applications of the techniques of statistical mechanics are widespread, and include: applications to physical systems such as solids, liquids and gases; applications to chemical and biological systems (colloids, interfaces, complex fluids, polymers and biopolymers, cell physics); and other interdisciplinary applications to for instance biological, economical and sociological systems.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: