Luca Enriques, Yoon-Ho Alex Lee, Alessandro Romano

{"title":"内幕交易监管的安慰剂效应。","authors":"Luca Enriques, Yoon-Ho Alex Lee, Alessandro Romano","doi":"10.1093/ojls/gqaf019","DOIUrl":null,"url":null,"abstract":"<p><p>Insiders can profit from material non-public information pertaining to their own firm by trading in the shares of their own company (traditional insider trading) or in the shares of other companies whose stock prices may also be affected by such information (shadow trading). We show that traditional insider trading and shadow trading have the same consequences for financial markets and corporate governance, but only the former is pursued aggressively by regulators in the European Union, the UK and the United States. Drawing on a variety of evidence, including a survey of 200 retail investors, we suggest that, rather than protecting unsuspecting outside investors, such an arrangement enables insiders to profit at their expense. The ban on the more salient practice of traditional insider dealing regulation lulls outside investors into a false sense of security, thus effectively operating as a placebo, whilst insiders can still profit by engaging in shadow trading. We further argue that, ironically, this arrangement may nonetheless be efficient.</p>","PeriodicalId":47225,"journal":{"name":"Oxford Journal of Legal Studies","volume":"45 3","pages":"753-774"},"PeriodicalIF":1.0000,"publicationDate":"2025-06-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12395251/pdf/","citationCount":"0","resultStr":"{\"title\":\"The Placebo Effect of Insider Dealing Regulation.\",\"authors\":\"Luca Enriques, Yoon-Ho Alex Lee, Alessandro Romano\",\"doi\":\"10.1093/ojls/gqaf019\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Insiders can profit from material non-public information pertaining to their own firm by trading in the shares of their own company (traditional insider trading) or in the shares of other companies whose stock prices may also be affected by such information (shadow trading). We show that traditional insider trading and shadow trading have the same consequences for financial markets and corporate governance, but only the former is pursued aggressively by regulators in the European Union, the UK and the United States. Drawing on a variety of evidence, including a survey of 200 retail investors, we suggest that, rather than protecting unsuspecting outside investors, such an arrangement enables insiders to profit at their expense. The ban on the more salient practice of traditional insider dealing regulation lulls outside investors into a false sense of security, thus effectively operating as a placebo, whilst insiders can still profit by engaging in shadow trading. We further argue that, ironically, this arrangement may nonetheless be efficient.</p>\",\"PeriodicalId\":47225,\"journal\":{\"name\":\"Oxford Journal of Legal Studies\",\"volume\":\"45 3\",\"pages\":\"753-774\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2025-06-10\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12395251/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Oxford Journal of Legal Studies\",\"FirstCategoryId\":\"90\",\"ListUrlMain\":\"https://doi.org/10.1093/ojls/gqaf019\",\"RegionNum\":2,\"RegionCategory\":\"社会学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2025/1/1 0:00:00\",\"PubModel\":\"eCollection\",\"JCR\":\"Q1\",\"JCRName\":\"LAW\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Oxford Journal of Legal Studies","FirstCategoryId":"90","ListUrlMain":"https://doi.org/10.1093/ojls/gqaf019","RegionNum":2,"RegionCategory":"社会学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2025/1/1 0:00:00","PubModel":"eCollection","JCR":"Q1","JCRName":"LAW","Score":null,"Total":0}

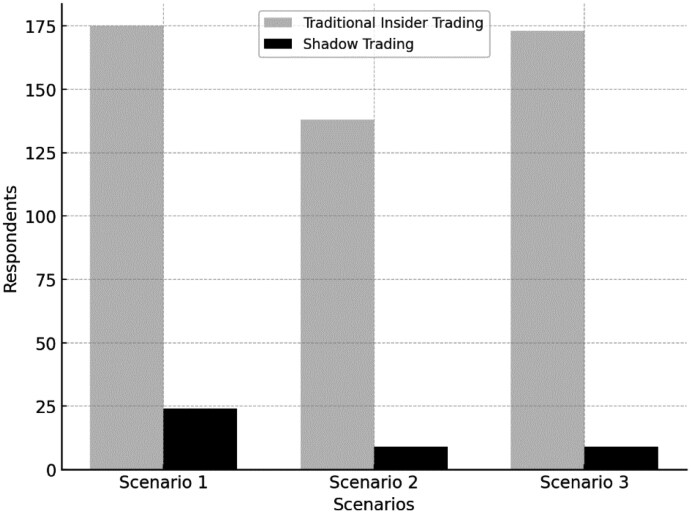

Insiders can profit from material non-public information pertaining to their own firm by trading in the shares of their own company (traditional insider trading) or in the shares of other companies whose stock prices may also be affected by such information (shadow trading). We show that traditional insider trading and shadow trading have the same consequences for financial markets and corporate governance, but only the former is pursued aggressively by regulators in the European Union, the UK and the United States. Drawing on a variety of evidence, including a survey of 200 retail investors, we suggest that, rather than protecting unsuspecting outside investors, such an arrangement enables insiders to profit at their expense. The ban on the more salient practice of traditional insider dealing regulation lulls outside investors into a false sense of security, thus effectively operating as a placebo, whilst insiders can still profit by engaging in shadow trading. We further argue that, ironically, this arrangement may nonetheless be efficient.

期刊介绍:

The Oxford Journal of Legal Studies is published on behalf of the Faculty of Law in the University of Oxford. It is designed to encourage interest in all matters relating to law, with an emphasis on matters of theory and on broad issues arising from the relationship of law to other disciplines. No topic of legal interest is excluded from consideration. In addition to traditional questions of legal interest, the following are all within the purview of the journal: comparative and international law, the law of the European Community, legal history and philosophy, and interdisciplinary material in areas of relevance.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: