{"title":"逆向增长会计:企业增长战略规划的经济工具","authors":"Ali Zeytoon-Nejad","doi":"10.1002/mde.4519","DOIUrl":null,"url":null,"abstract":"<p>Business growth is a goal of great importance for its both private and social benefits. Many firms view business growth as an imperative for their survival, stability, and long-term success. Business growth can be socially beneficial, too, as it enables businesses to expand into new territories where they can stimulate economic growth and development, creates more jobs, increase living standards, and better serve their communities by giving back more through Corporate Social Responsibility (CSR) initiatives. Business growth must be planned reasonably and optimally so that it can effectively achieve its critical ambitions in business practice. The current common practices for planning the supply side of business growth are usually ad-hoc and lack well-established mathematical and economic foundations. The present paper argues that business growth planning can be pursued more structurally, reliably, and meaningfully within the framework of Growth Accounting (GA), which was first introduced by Economics Nobel Laureate Robert Solow to study economic growth. It is shown that, although GA was initially put forth as a procedure to explain “economic growth” <i>ex-post</i>, it can similarly be used to plan “business growth” <i>ex-ante</i> when a general backward approach is taken in its procedure—called Backward Growth Accounting (BGA) in this paper. Taking this well-established economic–mathematical approach to planning business growth will enhance the current practices conceptually and structurally, as it is built on the basis of economic logic and mathematical tools. BGA can help businesses identify and plan for key drivers of output growth and assess shortcomings in the growth process, such as poor productivity, inadequate labor utilization, or insufficient capital investment. The paper outlines an eight-step procedure for planning business growth using BGA and includes appendices with real-world examples.C5, D2, L1, M11, M21, O4.</p>","PeriodicalId":18186,"journal":{"name":"Managerial and Decision Economics","volume":"46 6","pages":"3296-3317"},"PeriodicalIF":2.7000,"publicationDate":"2025-03-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/mde.4519","citationCount":"0","resultStr":"{\"title\":\"Backward Growth Accounting: An Economic Tool for Strategic Planning of Business Growth\",\"authors\":\"Ali Zeytoon-Nejad\",\"doi\":\"10.1002/mde.4519\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Business growth is a goal of great importance for its both private and social benefits. Many firms view business growth as an imperative for their survival, stability, and long-term success. Business growth can be socially beneficial, too, as it enables businesses to expand into new territories where they can stimulate economic growth and development, creates more jobs, increase living standards, and better serve their communities by giving back more through Corporate Social Responsibility (CSR) initiatives. Business growth must be planned reasonably and optimally so that it can effectively achieve its critical ambitions in business practice. The current common practices for planning the supply side of business growth are usually ad-hoc and lack well-established mathematical and economic foundations. The present paper argues that business growth planning can be pursued more structurally, reliably, and meaningfully within the framework of Growth Accounting (GA), which was first introduced by Economics Nobel Laureate Robert Solow to study economic growth. It is shown that, although GA was initially put forth as a procedure to explain “economic growth” <i>ex-post</i>, it can similarly be used to plan “business growth” <i>ex-ante</i> when a general backward approach is taken in its procedure—called Backward Growth Accounting (BGA) in this paper. Taking this well-established economic–mathematical approach to planning business growth will enhance the current practices conceptually and structurally, as it is built on the basis of economic logic and mathematical tools. BGA can help businesses identify and plan for key drivers of output growth and assess shortcomings in the growth process, such as poor productivity, inadequate labor utilization, or insufficient capital investment. The paper outlines an eight-step procedure for planning business growth using BGA and includes appendices with real-world examples.C5, D2, L1, M11, M21, O4.</p>\",\"PeriodicalId\":18186,\"journal\":{\"name\":\"Managerial and Decision Economics\",\"volume\":\"46 6\",\"pages\":\"3296-3317\"},\"PeriodicalIF\":2.7000,\"publicationDate\":\"2025-03-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/mde.4519\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Managerial and Decision Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/mde.4519\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Managerial and Decision Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/mde.4519","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Backward Growth Accounting: An Economic Tool for Strategic Planning of Business Growth

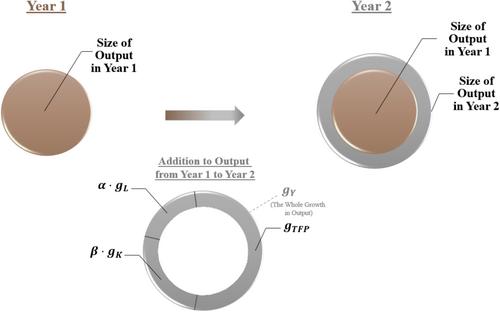

Business growth is a goal of great importance for its both private and social benefits. Many firms view business growth as an imperative for their survival, stability, and long-term success. Business growth can be socially beneficial, too, as it enables businesses to expand into new territories where they can stimulate economic growth and development, creates more jobs, increase living standards, and better serve their communities by giving back more through Corporate Social Responsibility (CSR) initiatives. Business growth must be planned reasonably and optimally so that it can effectively achieve its critical ambitions in business practice. The current common practices for planning the supply side of business growth are usually ad-hoc and lack well-established mathematical and economic foundations. The present paper argues that business growth planning can be pursued more structurally, reliably, and meaningfully within the framework of Growth Accounting (GA), which was first introduced by Economics Nobel Laureate Robert Solow to study economic growth. It is shown that, although GA was initially put forth as a procedure to explain “economic growth” ex-post, it can similarly be used to plan “business growth” ex-ante when a general backward approach is taken in its procedure—called Backward Growth Accounting (BGA) in this paper. Taking this well-established economic–mathematical approach to planning business growth will enhance the current practices conceptually and structurally, as it is built on the basis of economic logic and mathematical tools. BGA can help businesses identify and plan for key drivers of output growth and assess shortcomings in the growth process, such as poor productivity, inadequate labor utilization, or insufficient capital investment. The paper outlines an eight-step procedure for planning business growth using BGA and includes appendices with real-world examples.C5, D2, L1, M11, M21, O4.

期刊介绍:

Managerial and Decision Economics will publish articles applying economic reasoning to managerial decision-making and management strategy.Management strategy concerns practical decisions that managers face about how to compete, how to succeed, and how to organize to achieve their goals. Economic thinking and analysis provides a critical foundation for strategic decision-making across a variety of dimensions. For example, economic insights may help in determining which activities to outsource and which to perfom internally. They can help unravel questions regarding what drives performance differences among firms and what allows these differences to persist. They can contribute to an appreciation of how industries, organizations, and capabilities evolve.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: