{"title":"基于深度学习技术的股市分析多因素预测模型。","authors":"Kangyi Wang","doi":"10.1038/s41598-025-88734-6","DOIUrl":null,"url":null,"abstract":"<p><p>Stock market stability relies on the shares, investors, and stakeholders' participation and global commodity exchanges. In general, multiple factors influence the stock market stability to ensure profitable returns and commodity transactions. This article presents a contradictory-factor-based stability prediction model using the sigmoid deep learning paradigm. Sigmoid learning identifies the possible stabilizations of different influencing factors toward a profitable stock exchange. In this model, each influencing factor is mapped with the profit outcomes considering the live shares and their exchange value. The stability is predicted using sigmoid and non-sigmoid layers repeatedly until the maximum is reached. This stability is matched with the previous outcomes to predict the consecutive hours of stock market changes. Based on the actual changes and predicted ones, the sigmoid function is altered to accommodate the new range. The non-sigmoid layer remains unchanged in the new changes to improve the prediction precision. Based on the outcomes the deep learning's sigmoid layer is trained to identify abrupt changes in the stock market.</p>","PeriodicalId":21811,"journal":{"name":"Scientific Reports","volume":"15 1","pages":"5121"},"PeriodicalIF":3.9000,"publicationDate":"2025-02-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC11814281/pdf/","citationCount":"0","resultStr":"{\"title\":\"Multifactor prediction model for stock market analysis based on deep learning techniques.\",\"authors\":\"Kangyi Wang\",\"doi\":\"10.1038/s41598-025-88734-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Stock market stability relies on the shares, investors, and stakeholders' participation and global commodity exchanges. In general, multiple factors influence the stock market stability to ensure profitable returns and commodity transactions. This article presents a contradictory-factor-based stability prediction model using the sigmoid deep learning paradigm. Sigmoid learning identifies the possible stabilizations of different influencing factors toward a profitable stock exchange. In this model, each influencing factor is mapped with the profit outcomes considering the live shares and their exchange value. The stability is predicted using sigmoid and non-sigmoid layers repeatedly until the maximum is reached. This stability is matched with the previous outcomes to predict the consecutive hours of stock market changes. Based on the actual changes and predicted ones, the sigmoid function is altered to accommodate the new range. The non-sigmoid layer remains unchanged in the new changes to improve the prediction precision. Based on the outcomes the deep learning's sigmoid layer is trained to identify abrupt changes in the stock market.</p>\",\"PeriodicalId\":21811,\"journal\":{\"name\":\"Scientific Reports\",\"volume\":\"15 1\",\"pages\":\"5121\"},\"PeriodicalIF\":3.9000,\"publicationDate\":\"2025-02-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC11814281/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Scientific Reports\",\"FirstCategoryId\":\"103\",\"ListUrlMain\":\"https://doi.org/10.1038/s41598-025-88734-6\",\"RegionNum\":2,\"RegionCategory\":\"综合性期刊\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"MULTIDISCIPLINARY SCIENCES\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Scientific Reports","FirstCategoryId":"103","ListUrlMain":"https://doi.org/10.1038/s41598-025-88734-6","RegionNum":2,"RegionCategory":"综合性期刊","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"MULTIDISCIPLINARY SCIENCES","Score":null,"Total":0}

Multifactor prediction model for stock market analysis based on deep learning techniques.

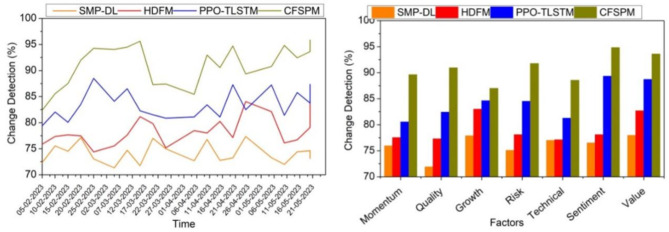

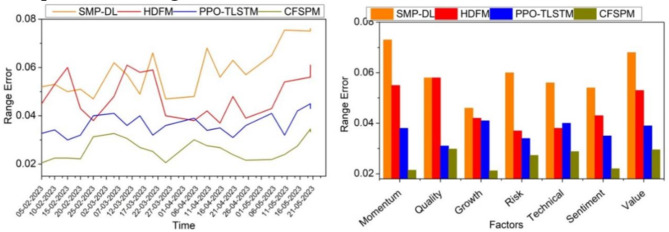

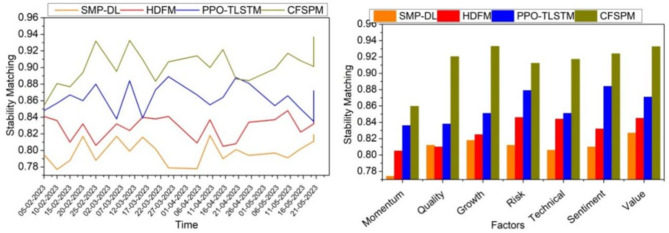

Stock market stability relies on the shares, investors, and stakeholders' participation and global commodity exchanges. In general, multiple factors influence the stock market stability to ensure profitable returns and commodity transactions. This article presents a contradictory-factor-based stability prediction model using the sigmoid deep learning paradigm. Sigmoid learning identifies the possible stabilizations of different influencing factors toward a profitable stock exchange. In this model, each influencing factor is mapped with the profit outcomes considering the live shares and their exchange value. The stability is predicted using sigmoid and non-sigmoid layers repeatedly until the maximum is reached. This stability is matched with the previous outcomes to predict the consecutive hours of stock market changes. Based on the actual changes and predicted ones, the sigmoid function is altered to accommodate the new range. The non-sigmoid layer remains unchanged in the new changes to improve the prediction precision. Based on the outcomes the deep learning's sigmoid layer is trained to identify abrupt changes in the stock market.

期刊介绍:

We publish original research from all areas of the natural sciences, psychology, medicine and engineering. You can learn more about what we publish by browsing our specific scientific subject areas below or explore Scientific Reports by browsing all articles and collections.

Scientific Reports has a 2-year impact factor: 4.380 (2021), and is the 6th most-cited journal in the world, with more than 540,000 citations in 2020 (Clarivate Analytics, 2021).

•Engineering

Engineering covers all aspects of engineering, technology, and applied science. It plays a crucial role in the development of technologies to address some of the world''s biggest challenges, helping to save lives and improve the way we live.

•Physical sciences

Physical sciences are those academic disciplines that aim to uncover the underlying laws of nature — often written in the language of mathematics. It is a collective term for areas of study including astronomy, chemistry, materials science and physics.

•Earth and environmental sciences

Earth and environmental sciences cover all aspects of Earth and planetary science and broadly encompass solid Earth processes, surface and atmospheric dynamics, Earth system history, climate and climate change, marine and freshwater systems, and ecology. It also considers the interactions between humans and these systems.

•Biological sciences

Biological sciences encompass all the divisions of natural sciences examining various aspects of vital processes. The concept includes anatomy, physiology, cell biology, biochemistry and biophysics, and covers all organisms from microorganisms, animals to plants.

•Health sciences

The health sciences study health, disease and healthcare. This field of study aims to develop knowledge, interventions and technology for use in healthcare to improve the treatment of patients.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: