{"title":"二元期权超级对冲问题中的近似和渐近问题","authors":"Sergey Smirnov, Dimitri Sotnikov, Andrey Zanochkin","doi":"10.1007/s10436-024-00454-5","DOIUrl":null,"url":null,"abstract":"<div><p>This paper considers Kolokoltsov’s multiplicative model of market price dynamics witout trading constraints. Under general assumptions and monotonic payoff functions, we show that the guaranteed deterministic approach, having a game-theoretic interpretation, yields the same result in the superhedging problem as in the probabilistic approach. We analyze in detail the superhedging problem for a special monotonic payoff function, i.e., a European-style binary option, within the guaranteed deterministic approach (GDA). Unlike the probabilistic counterpart, GDA allows a direct description of the most unfavorable mixed market strategy. We obtain some interesting analytical properties of the solutions of the corresponding Bellman–Isaacs equations, providing the minimal required reserves (also called the superhedging price) to cover the option payoff at the expiration time. The price process with the conditional distributions corresponding to the most unfavorable market scenarios can be approximated on a logarithmic scale by a random walk with two absorbing barriers. We also prove that, under an appropriate normalization, the price process weakly converges to the geometric Brownian motion with one absorbing barrier at the strike price when the discrete-time model number of steps tends to infinity.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"20 4","pages":"421 - 458"},"PeriodicalIF":0.7000,"publicationDate":"2024-09-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Approximation and asymptotics in the superhedging problem for binary options\",\"authors\":\"Sergey Smirnov, Dimitri Sotnikov, Andrey Zanochkin\",\"doi\":\"10.1007/s10436-024-00454-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This paper considers Kolokoltsov’s multiplicative model of market price dynamics witout trading constraints. Under general assumptions and monotonic payoff functions, we show that the guaranteed deterministic approach, having a game-theoretic interpretation, yields the same result in the superhedging problem as in the probabilistic approach. We analyze in detail the superhedging problem for a special monotonic payoff function, i.e., a European-style binary option, within the guaranteed deterministic approach (GDA). Unlike the probabilistic counterpart, GDA allows a direct description of the most unfavorable mixed market strategy. We obtain some interesting analytical properties of the solutions of the corresponding Bellman–Isaacs equations, providing the minimal required reserves (also called the superhedging price) to cover the option payoff at the expiration time. The price process with the conditional distributions corresponding to the most unfavorable market scenarios can be approximated on a logarithmic scale by a random walk with two absorbing barriers. We also prove that, under an appropriate normalization, the price process weakly converges to the geometric Brownian motion with one absorbing barrier at the strike price when the discrete-time model number of steps tends to infinity.</p></div>\",\"PeriodicalId\":45289,\"journal\":{\"name\":\"Annals of Finance\",\"volume\":\"20 4\",\"pages\":\"421 - 458\"},\"PeriodicalIF\":0.7000,\"publicationDate\":\"2024-09-27\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10436-024-00454-5\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-024-00454-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Approximation and asymptotics in the superhedging problem for binary options

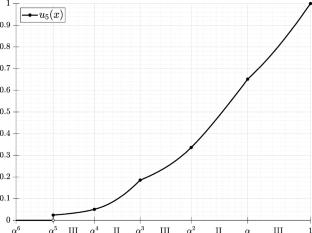

This paper considers Kolokoltsov’s multiplicative model of market price dynamics witout trading constraints. Under general assumptions and monotonic payoff functions, we show that the guaranteed deterministic approach, having a game-theoretic interpretation, yields the same result in the superhedging problem as in the probabilistic approach. We analyze in detail the superhedging problem for a special monotonic payoff function, i.e., a European-style binary option, within the guaranteed deterministic approach (GDA). Unlike the probabilistic counterpart, GDA allows a direct description of the most unfavorable mixed market strategy. We obtain some interesting analytical properties of the solutions of the corresponding Bellman–Isaacs equations, providing the minimal required reserves (also called the superhedging price) to cover the option payoff at the expiration time. The price process with the conditional distributions corresponding to the most unfavorable market scenarios can be approximated on a logarithmic scale by a random walk with two absorbing barriers. We also prove that, under an appropriate normalization, the price process weakly converges to the geometric Brownian motion with one absorbing barrier at the strike price when the discrete-time model number of steps tends to infinity.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: