揭示科维德-19 大流行病期间印度股票行业的非对称回报溢出效应及投资组合影响

IF 3.8

3区 经济学

Q1 BUSINESS, FINANCE

North American Journal of Economics and Finance

Pub Date : 2024-10-16

DOI:10.1016/j.najef.2024.102297

引用次数: 0

摘要

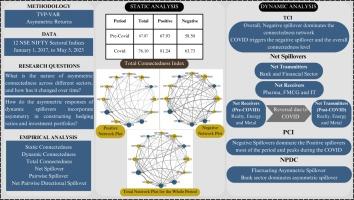

本文旨在系统探究印度行业指数网络在大流行前后的回报溢出动态。为了进行分析,本文使用了非对称时变参数向量自回归(TVP-VAR)框架。此外,本着 Broadstock 等人(2020 年)的精神,我们根据常见的对冲技术和最小连通性投资组合方法进行了动态投资组合练习,以确定哪种方法能更好地捕捉不对称现象。我们的每日数据集包括 12 种行业股票,时间跨度为 2017 年 1 月 1 日至 2023 年 5 月 5 日。研究结果表明,在整个样本期间,负连通性占主导地位,这表明利润最大化代理人和风险规避型投资者更有可能对新闻做出负面反应。我们还发现,在整个样本期内,网络中的平均净传播者是银行业和其他金融服务业,而净接收者则是信息技术、医药和快速消费品行业。我们的研究结果表明,基于夏普比率,最小关联度投资组合(MCoP)方法是一种非常有用的方法,因为在这三种竞争方法中,它是第一或第二大盈利方法。因此,这些结果为政策制定者和投资者提供了宝贵的见解。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Unveiling asymmetric return spillovers with portfolio implications among Indian stock sectors during Covid-19 pandemic

This paper aims to provide a systematic inquiry into the return spillover dynamics between a network of Indian sectoral indices during the pre- and post-pandemic periods. To analyze the same, this paper uses the asymmetric time-varying parameter vector autoregressions (TVP-VAR) framework. Furthermore, in the spirit of Broadstock et al. (2020), we perform dynamic portfolio exercises based on common hedging techniques and the minimum connectedness portfolio approach to determine what better captures asymmetry. Our daily dataset includes 12 sectoral stocks spanning from January 01, 2017, to May 5, 2023. The findings reveal that negative connectedness dominates throughout the sample period, demonstrating that profit-maximizing agents and risk-averse investors are more likely to react negatively to news. We also show that in the network, the average net transmitters are the banking and other financial service sectors, whereas the net receivers are the information technology, pharmaceutical, and fast-moving consumer goods sectors throughout the period under consideration. Our results show that the minimum connectedness portfolio (MCoP) approach is a very useful method based on Sharpe ratios, as it is either the first or second most profitable among these three competing methods. These results, therefore, yield valuable insights for policymakers and investors.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

CiteScore

7.30

自引率

8.30%

发文量

168

期刊介绍:

The focus of the North-American Journal of Economics and Finance is on the economics of integration of goods, services, financial markets, at both regional and global levels with the role of economic policy in that process playing an important role. Both theoretical and empirical papers are welcome. Empirical and policy-related papers that rely on data and the experiences of countries outside North America are also welcome. Papers should offer concrete lessons about the ongoing process of globalization, or policy implications about how governments, domestic or international institutions, can improve the coordination of their activities. Empirical analysis should be capable of replication. Authors of accepted papers will be encouraged to supply data and computer programs.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: