多因素视角下的波动率管理投资组合

IF 9.5

1区 经济学

Q1 BUSINESS, FINANCE

引用次数: 0

摘要

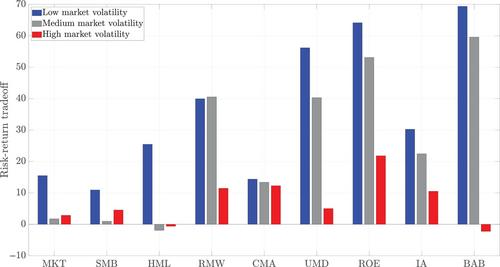

莫雷拉和穆尔质疑是否存在强烈的风险收益权衡,他们的研究表明,当风险因素的波动性较高时,投资者可以通过减少风险因素的暴露来提高业绩。然而,Cederburg 等人的研究表明,这些策略在样本外失效,而 Barroso 和 Detzel 的研究则表明,这些策略无法在交易成本的影响下生存。我们提出了一种有条件的多因子投资组合,即使在样本外和扣除成本后,其表现也优于无条件的对应策略。此外,我们还表明,因子风险价格一般会随着市场波动而降低。我们的研究结果表明,风险收益权衡的分解比以前想象的更加令人费解。本文章由计算机程序翻译,如有差异,请以英文原文为准。

A Multifactor Perspective on Volatility-Managed Portfolios

Moreira and Muir question the existence of a strong risk-return trade-off by showing that investors can improve performance by reducing exposure to risk factors when their volatility is high. However, Cederburg et al. show that these strategies fail out-of-sample, and Barroso and Detzel show they do not survive transaction costs. We propose a conditional multifactor portfolio that outperforms its unconditional counterpart even out-of-sample and net of costs. Moreover, we show that factor risk prices generally decrease with market volatility. Our results demonstrate that the breakdown of the risk-return trade-off is more puzzling than previously thought.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Finance

Multiple-

CiteScore

12.90

自引率

2.50%

发文量

88

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: