债券与股票:投资信息

IF 9.5

1区 经济学

Q1 BUSINESS, FINANCE

引用次数: 0

摘要

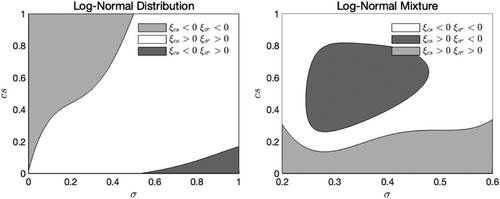

我们提供了一个以债务和股权融资的公司进行投资的简单模型,并提供了经验证据来证明,一旦我们用信用利差控制了债务悬置问题,资产波动对投资来说就是一个明确的积极信号,而股权波动则是一个混合信号:波动率上升会提高股权期权价值,增加财务稳健企业的投资,但会加剧债务悬置,减少濒临违约企业的投资。我们的研究为投资、信用利差、股票相对于资产波动率、杠杆率和托宾 q$q$ 之间的结构和经验关系提供了一个简单统一的理解。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Bonds versus Equities: Information for Investment

We provide a simple model of investment by a firm funded with debt and equity and empirical evidence to demonstrate that, once we control for the debt overhang problem with credit spreads, asset volatility is an unambiguously positive signal for investment, while equity volatility sends a mixed signal: Elevated volatility raises the option value of equity and increases investment for financially sound firms, but exacerbates debt overhang and decreases investment for firms close to default. Our study provides a simple unified understanding of the structural and empirical relationships between investment, credit spreads, equity versus asset volatility, leverage, and Tobin's .

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Finance

Multiple-

CiteScore

12.90

自引率

2.50%

发文量

88

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: