Evelyn R. Patterson, J. Reed Smith, Samuel L. Tiras

{"title":"审计委员会在战略背景下进行监督的效果和潜在益处","authors":"Evelyn R. Patterson, J. Reed Smith, Samuel L. Tiras","doi":"10.1111/1911-3846.12964","DOIUrl":null,"url":null,"abstract":"<p>Since the passage of the Sarbanes-Oxley Act of 2002, many notable frauds have been tied to ineffective audit committee (AC) oversight. As a result, AC oversight is of continuing interest, and regulators continue to debate this issue, garnering a growing body of research focused on the role played by the AC. But little theoretical research exists to guide analytical and empirical researchers investigating AC oversight. The purpose of this study is to provide theoretical guidance by examining AC oversight in a strategic setting. We focus on the AC's role in overseeing internal controls (ICs) and the impact of whether the AC relies on management in designing the controls. We characterize how the nature of control risk changes and how IC strength is associated with the amount of managerial fraud, expected probability of fraud detection (which, on average, equates to audit effort), and audit quality (assessed as 1 − audit risk) across two settings defined by the degree of AC oversight. As one example that highlights the need for theoretical guidance, we consider the literature's presumption that IC strength is negatively associated with audit effort. We find that this association may be positive or negative as IC changes, where the association varies with the degree of direct AC oversight and the change in payoff parameters.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 3","pages":"2013-2040"},"PeriodicalIF":3.8000,"publicationDate":"2024-08-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12964","citationCount":"0","resultStr":"{\"title\":\"The effects and potential benefits of audit committee oversight in a strategic setting\",\"authors\":\"Evelyn R. Patterson, J. Reed Smith, Samuel L. Tiras\",\"doi\":\"10.1111/1911-3846.12964\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Since the passage of the Sarbanes-Oxley Act of 2002, many notable frauds have been tied to ineffective audit committee (AC) oversight. As a result, AC oversight is of continuing interest, and regulators continue to debate this issue, garnering a growing body of research focused on the role played by the AC. But little theoretical research exists to guide analytical and empirical researchers investigating AC oversight. The purpose of this study is to provide theoretical guidance by examining AC oversight in a strategic setting. We focus on the AC's role in overseeing internal controls (ICs) and the impact of whether the AC relies on management in designing the controls. We characterize how the nature of control risk changes and how IC strength is associated with the amount of managerial fraud, expected probability of fraud detection (which, on average, equates to audit effort), and audit quality (assessed as 1 − audit risk) across two settings defined by the degree of AC oversight. As one example that highlights the need for theoretical guidance, we consider the literature's presumption that IC strength is negatively associated with audit effort. We find that this association may be positive or negative as IC changes, where the association varies with the degree of direct AC oversight and the change in payoff parameters.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 3\",\"pages\":\"2013-2040\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2024-08-13\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12964\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12964\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12964","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

摘要

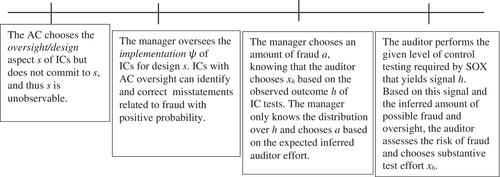

自 2002 年《萨班斯-奥克斯利法案》通过以来,许多著名的欺诈案都与审计委员会(AC)监督不力有关。因此,审计委员会的监督问题一直备受关注,监管机构也一直在争论这个问题,并引发了越来越多关于审计委员会作用的研究。但是,很少有理论研究能为调查 AC 监督的分析和实证研究人员提供指导。本研究的目的是通过研究战略背景下的AC监督来提供理论指导。我们重点关注审计委员会在监督内部控制(IC)方面的作用,以及审计委员会在设计控制时是否依赖管理层的影响。我们描述了控制风险的性质是如何变化的,以及在由审计委员会监督程度定义的两种情况下,内部控制的力度是如何与管理舞弊的数量、舞弊被发现的预期概率(平均而言,相当于审计工作量)和审计质量(评估为 1 - 审计风险)相关联的。作为强调理论指导必要性的一个例子,我们考虑了文献中关于集成电路强度与审计工作负相关的假设。我们发现,随着集成电路的变化,这种关联可能是正的,也可能是负的,其关联随审计委员会的直接监督程度和报酬参数的变化而变化。

The effects and potential benefits of audit committee oversight in a strategic setting

Since the passage of the Sarbanes-Oxley Act of 2002, many notable frauds have been tied to ineffective audit committee (AC) oversight. As a result, AC oversight is of continuing interest, and regulators continue to debate this issue, garnering a growing body of research focused on the role played by the AC. But little theoretical research exists to guide analytical and empirical researchers investigating AC oversight. The purpose of this study is to provide theoretical guidance by examining AC oversight in a strategic setting. We focus on the AC's role in overseeing internal controls (ICs) and the impact of whether the AC relies on management in designing the controls. We characterize how the nature of control risk changes and how IC strength is associated with the amount of managerial fraud, expected probability of fraud detection (which, on average, equates to audit effort), and audit quality (assessed as 1 − audit risk) across two settings defined by the degree of AC oversight. As one example that highlights the need for theoretical guidance, we consider the literature's presumption that IC strength is negatively associated with audit effort. We find that this association may be positive or negative as IC changes, where the association varies with the degree of direct AC oversight and the change in payoff parameters.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: