Augustin Bergeron, Gabriel Tourek, Jonathan L. Weigel

{"title":"税率的国家能力上限:刚果民主共和国随机减税的证据","authors":"Augustin Bergeron, Gabriel Tourek, Jonathan L. Weigel","doi":"10.3982/ECTA19959","DOIUrl":null,"url":null,"abstract":"<div>\n <p>This paper investigates how tax rates and tax enforcement jointly impact fiscal capacity in low-income countries. We study a policy experiment in the D.R. Congo that randomly assigned 38,028 property owners to the status quo tax rate or to a rate reduction. This variation in tax liabilities reveals that the status quo rate lies <i>above</i> the revenue-maximizing tax rate (RMTR). Reducing rates by about one-third would maximize government revenue by increasing tax compliance. We then exploit two sources of variation in enforcement—randomized enforcement letters and random assignment of tax collectors—to show that the RMTR increases with enforcement. Including an enforcement message on tax letters or replacing tax collectors in the bottom quartile of enforcement capacity with average collectors would raise the RMTR by about 40%. Tax rates and enforcement are thus complementary levers. Jointly optimizing tax rates and enforcement would lead to 10% higher revenue gains than optimizing them independently. These findings provide experimental evidence that low government enforcement capacity sets a binding ceiling on the revenue-maximizing tax rate in some developing countries, thereby demonstrating the value of increasing tax rates in tandem with enforcement to expand fiscal capacity.</p>\n </div>","PeriodicalId":50556,"journal":{"name":"Econometrica","volume":"92 4","pages":"1163-1193"},"PeriodicalIF":7.1000,"publicationDate":"2024-07-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.3982/ECTA19959","citationCount":"0","resultStr":"{\"title\":\"The State Capacity Ceiling on Tax Rates: Evidence From Randomized Tax Abatements in the DRC\",\"authors\":\"Augustin Bergeron, Gabriel Tourek, Jonathan L. Weigel\",\"doi\":\"10.3982/ECTA19959\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div>\\n <p>This paper investigates how tax rates and tax enforcement jointly impact fiscal capacity in low-income countries. We study a policy experiment in the D.R. Congo that randomly assigned 38,028 property owners to the status quo tax rate or to a rate reduction. This variation in tax liabilities reveals that the status quo rate lies <i>above</i> the revenue-maximizing tax rate (RMTR). Reducing rates by about one-third would maximize government revenue by increasing tax compliance. We then exploit two sources of variation in enforcement—randomized enforcement letters and random assignment of tax collectors—to show that the RMTR increases with enforcement. Including an enforcement message on tax letters or replacing tax collectors in the bottom quartile of enforcement capacity with average collectors would raise the RMTR by about 40%. Tax rates and enforcement are thus complementary levers. Jointly optimizing tax rates and enforcement would lead to 10% higher revenue gains than optimizing them independently. These findings provide experimental evidence that low government enforcement capacity sets a binding ceiling on the revenue-maximizing tax rate in some developing countries, thereby demonstrating the value of increasing tax rates in tandem with enforcement to expand fiscal capacity.</p>\\n </div>\",\"PeriodicalId\":50556,\"journal\":{\"name\":\"Econometrica\",\"volume\":\"92 4\",\"pages\":\"1163-1193\"},\"PeriodicalIF\":7.1000,\"publicationDate\":\"2024-07-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.3982/ECTA19959\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Econometrica\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.3982/ECTA19959\",\"RegionNum\":1,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Econometrica","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.3982/ECTA19959","RegionNum":1,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

The State Capacity Ceiling on Tax Rates: Evidence From Randomized Tax Abatements in the DRC

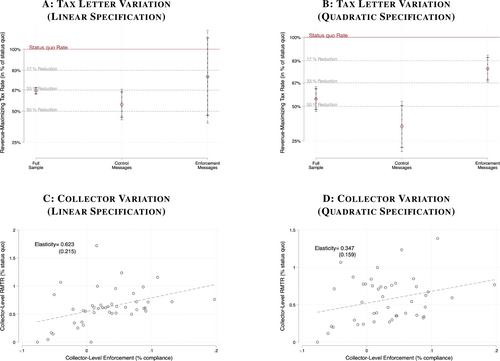

This paper investigates how tax rates and tax enforcement jointly impact fiscal capacity in low-income countries. We study a policy experiment in the D.R. Congo that randomly assigned 38,028 property owners to the status quo tax rate or to a rate reduction. This variation in tax liabilities reveals that the status quo rate lies above the revenue-maximizing tax rate (RMTR). Reducing rates by about one-third would maximize government revenue by increasing tax compliance. We then exploit two sources of variation in enforcement—randomized enforcement letters and random assignment of tax collectors—to show that the RMTR increases with enforcement. Including an enforcement message on tax letters or replacing tax collectors in the bottom quartile of enforcement capacity with average collectors would raise the RMTR by about 40%. Tax rates and enforcement are thus complementary levers. Jointly optimizing tax rates and enforcement would lead to 10% higher revenue gains than optimizing them independently. These findings provide experimental evidence that low government enforcement capacity sets a binding ceiling on the revenue-maximizing tax rate in some developing countries, thereby demonstrating the value of increasing tax rates in tandem with enforcement to expand fiscal capacity.

期刊介绍:

Econometrica publishes original articles in all branches of economics - theoretical and empirical, abstract and applied, providing wide-ranging coverage across the subject area. It promotes studies that aim at the unification of the theoretical-quantitative and the empirical-quantitative approach to economic problems and that are penetrated by constructive and rigorous thinking. It explores a unique range of topics each year - from the frontier of theoretical developments in many new and important areas, to research on current and applied economic problems, to methodologically innovative, theoretical and applied studies in econometrics.

Econometrica maintains a long tradition that submitted articles are refereed carefully and that detailed and thoughtful referee reports are provided to the author as an aid to scientific research, thus ensuring the high calibre of papers found in Econometrica. An international board of editors, together with the referees it has selected, has succeeded in substantially reducing editorial turnaround time, thereby encouraging submissions of the highest quality.

We strongly encourage recent Ph. D. graduates to submit their work to Econometrica. Our policy is to take into account the fact that recent graduates are less experienced in the process of writing and submitting papers.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: