{"title":"预期与利率中性","authors":"John H. Cochrane","doi":"10.1016/j.red.2024.04.004","DOIUrl":null,"url":null,"abstract":"<div><p>Our central banks set interest rates, and do not even pretend to control money supplies. How do interest rates affect inflation? We finally have a complete economic theory of inflation under interest rate targets and unconstrained liquidity. Its long-run properties mirror those of monetary theory: Inflation can be stable and determinate under interest rate targets, including a peg, analogous to a k-percent rule.</p><p>Uncomfortably, stability means that higher interest rates eventually raise inflation, just as higher money growth eventually raises inflation. Sticky prices generate some short-run non-neutrality: Higher nominal interest rates can raise real rates and lower output. A model in which higher nominal interest rates temporarily lower inflation, without a change in fiscal policy, is a harder task. I exhibit one such model, but it paints a more limited picture than standard beliefs. Generically, without a change in fiscal policy, monetary policy can only move inflation from one time to another.</p><p>The last decade has provided a near-ideal set of natural experiments to distinguish the principal theories of inflation. Inflation did not show spirals or indeterminacies at the long zero bound. The large monetary-fiscal expansion of the covid era produced a temporary spurt of inflation. The same money unleashed in quantitative easing had no such effect.</p></div>","PeriodicalId":47890,"journal":{"name":"Review of Economic Dynamics","volume":"53 ","pages":"Pages 194-223"},"PeriodicalIF":2.3000,"publicationDate":"2024-05-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Expectations and the neutrality of interest rates\",\"authors\":\"John H. Cochrane\",\"doi\":\"10.1016/j.red.2024.04.004\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Our central banks set interest rates, and do not even pretend to control money supplies. How do interest rates affect inflation? We finally have a complete economic theory of inflation under interest rate targets and unconstrained liquidity. Its long-run properties mirror those of monetary theory: Inflation can be stable and determinate under interest rate targets, including a peg, analogous to a k-percent rule.</p><p>Uncomfortably, stability means that higher interest rates eventually raise inflation, just as higher money growth eventually raises inflation. Sticky prices generate some short-run non-neutrality: Higher nominal interest rates can raise real rates and lower output. A model in which higher nominal interest rates temporarily lower inflation, without a change in fiscal policy, is a harder task. I exhibit one such model, but it paints a more limited picture than standard beliefs. Generically, without a change in fiscal policy, monetary policy can only move inflation from one time to another.</p><p>The last decade has provided a near-ideal set of natural experiments to distinguish the principal theories of inflation. Inflation did not show spirals or indeterminacies at the long zero bound. The large monetary-fiscal expansion of the covid era produced a temporary spurt of inflation. The same money unleashed in quantitative easing had no such effect.</p></div>\",\"PeriodicalId\":47890,\"journal\":{\"name\":\"Review of Economic Dynamics\",\"volume\":\"53 \",\"pages\":\"Pages 194-223\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2024-05-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Economic Dynamics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S1094202524000140\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Economic Dynamics","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S1094202524000140","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

摘要

我们的中央银行设定利率,甚至不假装控制货币供应。利率如何影响通货膨胀?在利率目标和流动性不受约束的情况下,我们终于有了关于通货膨胀的完整经济理论。它的长期属性与货币理论的属性如出一辙:在利率目标(包括类似于 k 百分比规则的挂钩)下,通货膨胀可以是稳定的、确定的。令人不安的是,稳定意味着利率的提高最终会提高通货膨胀,正如货币增长的提高最终会提高通货膨胀一样。粘性价格会产生一些短期的非中立性:名义利率的提高会提高实际利率并降低产出。在一个模型中,在不改变财政政策的情况下,提高名义利率会暂时降低通胀率,这是一项更艰巨的任务。我展示了一个这样的模型,但它所描绘的情况比标准信念更为有限。一般来说,在不改变财政政策的情况下,货币政策只能将通胀从一个时间推移到另一个时间。过去十年为区分通胀的主要理论提供了一套近乎理想的自然实验。在长期零界时,通胀并未出现螺旋式上升或不确定性。科维德时代的大规模货币财政扩张产生了暂时性的通货膨胀。而在量化宽松政策中释放的同样货币却没有这种效果。

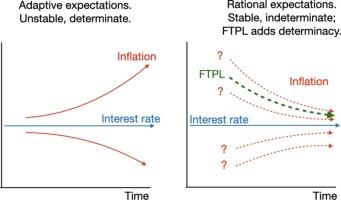

Our central banks set interest rates, and do not even pretend to control money supplies. How do interest rates affect inflation? We finally have a complete economic theory of inflation under interest rate targets and unconstrained liquidity. Its long-run properties mirror those of monetary theory: Inflation can be stable and determinate under interest rate targets, including a peg, analogous to a k-percent rule.

Uncomfortably, stability means that higher interest rates eventually raise inflation, just as higher money growth eventually raises inflation. Sticky prices generate some short-run non-neutrality: Higher nominal interest rates can raise real rates and lower output. A model in which higher nominal interest rates temporarily lower inflation, without a change in fiscal policy, is a harder task. I exhibit one such model, but it paints a more limited picture than standard beliefs. Generically, without a change in fiscal policy, monetary policy can only move inflation from one time to another.

The last decade has provided a near-ideal set of natural experiments to distinguish the principal theories of inflation. Inflation did not show spirals or indeterminacies at the long zero bound. The large monetary-fiscal expansion of the covid era produced a temporary spurt of inflation. The same money unleashed in quantitative easing had no such effect.

期刊介绍:

Review of Economic Dynamics publishes meritorious original contributions to dynamic economics. The scope of the journal is intended to be broad and to reflect the view of the Society for Economic Dynamics that the field of economics is unified by the scientific approach to economics. We will publish contributions in any area of economics provided they meet the highest standards of scientific research.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: