{"title":"数据分析战略和内部信息质量","authors":"Katie W. Lem","doi":"10.1111/1911-3846.12942","DOIUrl":null,"url":null,"abstract":"<p>I examine whether a strategic focus on data analytics is associated with improvements in firms' internal information quality. Using textual analysis of firm disclosures to identify a data analytics strategy, I first document that firm, leadership, and operating environment characteristics are all important determinants of the decision to adopt a data analytics strategy. I next use operating and financial reporting outcomes to infer whether a data analytics strategy improves internal information quality. I find that a data analytics strategy is associated with enhanced operating efficiency, as adopting firms invest and utilize existing resources more efficiently. I also find that a data analytics strategy is associated with more accurate management forecasts. These results, collectively, are consistent with a data analytics strategy improving firms' internal information quality. Lastly, I corroborate and extend my findings with job postings data, and the results suggest that firm leadership signals their support for data analytics initiatives through disclosure.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 2","pages":"1376-1410"},"PeriodicalIF":3.8000,"publicationDate":"2024-03-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12942","citationCount":"0","resultStr":"{\"title\":\"Data analytics strategy and internal information quality\",\"authors\":\"Katie W. Lem\",\"doi\":\"10.1111/1911-3846.12942\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>I examine whether a strategic focus on data analytics is associated with improvements in firms' internal information quality. Using textual analysis of firm disclosures to identify a data analytics strategy, I first document that firm, leadership, and operating environment characteristics are all important determinants of the decision to adopt a data analytics strategy. I next use operating and financial reporting outcomes to infer whether a data analytics strategy improves internal information quality. I find that a data analytics strategy is associated with enhanced operating efficiency, as adopting firms invest and utilize existing resources more efficiently. I also find that a data analytics strategy is associated with more accurate management forecasts. These results, collectively, are consistent with a data analytics strategy improving firms' internal information quality. Lastly, I corroborate and extend my findings with job postings data, and the results suggest that firm leadership signals their support for data analytics initiatives through disclosure.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 2\",\"pages\":\"1376-1410\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2024-03-04\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12942\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12942\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12942","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Data analytics strategy and internal information quality

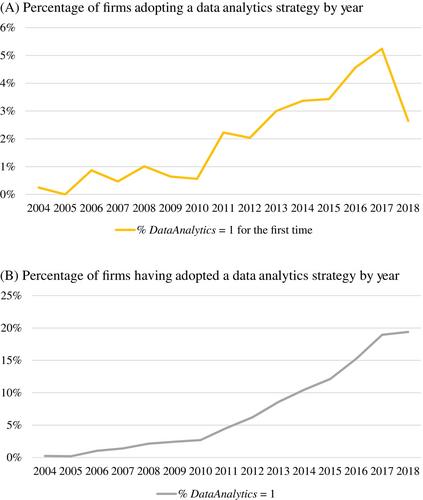

I examine whether a strategic focus on data analytics is associated with improvements in firms' internal information quality. Using textual analysis of firm disclosures to identify a data analytics strategy, I first document that firm, leadership, and operating environment characteristics are all important determinants of the decision to adopt a data analytics strategy. I next use operating and financial reporting outcomes to infer whether a data analytics strategy improves internal information quality. I find that a data analytics strategy is associated with enhanced operating efficiency, as adopting firms invest and utilize existing resources more efficiently. I also find that a data analytics strategy is associated with more accurate management forecasts. These results, collectively, are consistent with a data analytics strategy improving firms' internal information quality. Lastly, I corroborate and extend my findings with job postings data, and the results suggest that firm leadership signals their support for data analytics initiatives through disclosure.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: