{"title":"稳定变化点检测编码方法","authors":"Xiaodong Wang, Fushing Hsieh","doi":"10.1007/s10994-023-06510-x","DOIUrl":null,"url":null,"abstract":"<p>Without imposing prior distributional knowledge underlying multivariate time series of interest, we propose a nonparametric change-point detection approach to estimate the number of change points and their locations along the temporal axis. We develop a structural subsampling procedure such that the observations are encoded into multiple sequences of Bernoulli variables. A maximum likelihood approach in conjunction with a newly developed searching algorithm is implemented to detect change points on each Bernoulli process separately. Then, aggregation statistics are proposed to collectively synthesize change-point results from all individual univariate time series into consistent and stable location estimations. We also study a weighting strategy to measure the degree of relevance for different subsampled groups. Simulation studies are conducted and shown that the proposed change-point methodology for multivariate time series has favorable performance comparing with currently available state-of-the-art nonparametric methods under various settings with different degrees of complexity. Real data analyses are finally performed on categorical, ordinal, and continuous time series taken from fields of genetics, climate, and finance.</p>","PeriodicalId":49900,"journal":{"name":"Machine Learning","volume":"630 1","pages":""},"PeriodicalIF":4.3000,"publicationDate":"2024-02-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"An encoding approach for stable change point detection\",\"authors\":\"Xiaodong Wang, Fushing Hsieh\",\"doi\":\"10.1007/s10994-023-06510-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Without imposing prior distributional knowledge underlying multivariate time series of interest, we propose a nonparametric change-point detection approach to estimate the number of change points and their locations along the temporal axis. We develop a structural subsampling procedure such that the observations are encoded into multiple sequences of Bernoulli variables. A maximum likelihood approach in conjunction with a newly developed searching algorithm is implemented to detect change points on each Bernoulli process separately. Then, aggregation statistics are proposed to collectively synthesize change-point results from all individual univariate time series into consistent and stable location estimations. We also study a weighting strategy to measure the degree of relevance for different subsampled groups. Simulation studies are conducted and shown that the proposed change-point methodology for multivariate time series has favorable performance comparing with currently available state-of-the-art nonparametric methods under various settings with different degrees of complexity. Real data analyses are finally performed on categorical, ordinal, and continuous time series taken from fields of genetics, climate, and finance.</p>\",\"PeriodicalId\":49900,\"journal\":{\"name\":\"Machine Learning\",\"volume\":\"630 1\",\"pages\":\"\"},\"PeriodicalIF\":4.3000,\"publicationDate\":\"2024-02-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Machine Learning\",\"FirstCategoryId\":\"94\",\"ListUrlMain\":\"https://doi.org/10.1007/s10994-023-06510-x\",\"RegionNum\":3,\"RegionCategory\":\"计算机科学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Machine Learning","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s10994-023-06510-x","RegionNum":3,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE","Score":null,"Total":0}

An encoding approach for stable change point detection

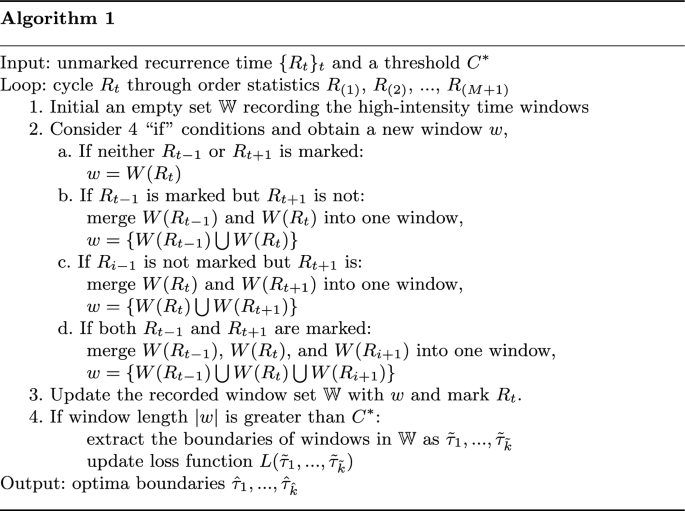

Without imposing prior distributional knowledge underlying multivariate time series of interest, we propose a nonparametric change-point detection approach to estimate the number of change points and their locations along the temporal axis. We develop a structural subsampling procedure such that the observations are encoded into multiple sequences of Bernoulli variables. A maximum likelihood approach in conjunction with a newly developed searching algorithm is implemented to detect change points on each Bernoulli process separately. Then, aggregation statistics are proposed to collectively synthesize change-point results from all individual univariate time series into consistent and stable location estimations. We also study a weighting strategy to measure the degree of relevance for different subsampled groups. Simulation studies are conducted and shown that the proposed change-point methodology for multivariate time series has favorable performance comparing with currently available state-of-the-art nonparametric methods under various settings with different degrees of complexity. Real data analyses are finally performed on categorical, ordinal, and continuous time series taken from fields of genetics, climate, and finance.

期刊介绍:

Machine Learning serves as a global platform dedicated to computational approaches in learning. The journal reports substantial findings on diverse learning methods applied to various problems, offering support through empirical studies, theoretical analysis, or connections to psychological phenomena. It demonstrates the application of learning methods to solve significant problems and aims to enhance the conduct of machine learning research with a focus on verifiable and replicable evidence in published papers.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: