Abdul-Rahman Khokhar, Jiaping Qiu, Mohammad M. Rahaman

{"title":"公司的流动性是否与年度报告中显示的一样?","authors":"Abdul-Rahman Khokhar, Jiaping Qiu, Mohammad M. Rahaman","doi":"10.1111/1911-3846.12929","DOIUrl":null,"url":null,"abstract":"<p>Fiscal-year-end cash holdings are an important indicator in external stakeholders' assessment of a firm's liquidity and credit risk. Do fiscal-year-end cash holdings reflect a firm's intra-year liquidity conditions? We observe that firms report significantly higher cash holdings in the fourth fiscal quarter, followed by a subsequent reversal. This pattern is pervasive across industries, persistent over time, and not explained by conventional factors or calendar effects. The extent of the fourth-quarter cash increase is more pronounced for informationally opaque firms reliant on external markets and those with financial constraints and reduced monitoring. We investigate firms' real, financing, and timing activities that could potentially account for this pattern. Our study suggests that a complete picture of intra-year cash holdings dynamics is necessary for external stakeholders to fully assess a firm's liquidity and credit conditions.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 2","pages":"944-975"},"PeriodicalIF":3.2000,"publicationDate":"2024-01-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12929","citationCount":"0","resultStr":"{\"title\":\"Are firms as liquid as they appear in annual reports?\",\"authors\":\"Abdul-Rahman Khokhar, Jiaping Qiu, Mohammad M. Rahaman\",\"doi\":\"10.1111/1911-3846.12929\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Fiscal-year-end cash holdings are an important indicator in external stakeholders' assessment of a firm's liquidity and credit risk. Do fiscal-year-end cash holdings reflect a firm's intra-year liquidity conditions? We observe that firms report significantly higher cash holdings in the fourth fiscal quarter, followed by a subsequent reversal. This pattern is pervasive across industries, persistent over time, and not explained by conventional factors or calendar effects. The extent of the fourth-quarter cash increase is more pronounced for informationally opaque firms reliant on external markets and those with financial constraints and reduced monitoring. We investigate firms' real, financing, and timing activities that could potentially account for this pattern. Our study suggests that a complete picture of intra-year cash holdings dynamics is necessary for external stakeholders to fully assess a firm's liquidity and credit conditions.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 2\",\"pages\":\"944-975\"},\"PeriodicalIF\":3.2000,\"publicationDate\":\"2024-01-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12929\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12929\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12929","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Are firms as liquid as they appear in annual reports?

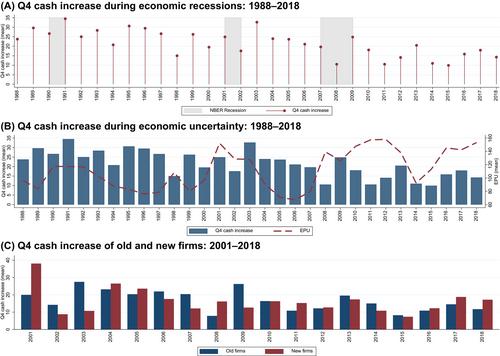

Fiscal-year-end cash holdings are an important indicator in external stakeholders' assessment of a firm's liquidity and credit risk. Do fiscal-year-end cash holdings reflect a firm's intra-year liquidity conditions? We observe that firms report significantly higher cash holdings in the fourth fiscal quarter, followed by a subsequent reversal. This pattern is pervasive across industries, persistent over time, and not explained by conventional factors or calendar effects. The extent of the fourth-quarter cash increase is more pronounced for informationally opaque firms reliant on external markets and those with financial constraints and reduced monitoring. We investigate firms' real, financing, and timing activities that could potentially account for this pattern. Our study suggests that a complete picture of intra-year cash holdings dynamics is necessary for external stakeholders to fully assess a firm's liquidity and credit conditions.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: