{"title":"从大数据量化回归透视宏观经济尾部风险的非线性因素","authors":"Jan Prüser, Florian Huber","doi":"10.1002/jae.3018","DOIUrl":null,"url":null,"abstract":"<p>Modeling and predicting extreme movements in GDP is notoriously difficult, and the selection of appropriate covariates and/or possible forms of nonlinearities are key in obtaining precise forecasts. In this paper, our focus is on using large datasets in quantile regression models to forecast the conditional distribution of US GDP growth. To capture possible nonlinearities, we include several nonlinear specifications. The resulting models will be huge dimensional, and we thus rely on a set of shrinkage priors. Since Markov chain Monte Carlo estimation becomes slow in these dimensions, we rely on fast variational Bayes approximations to the posterior distribution of the coefficients and the latent states. We find that our proposed set of models produces precise forecasts. These gains are especially pronounced in the tails. Using Gaussian processes to approximate the nonlinear component of the model further improves the good performance, in particular in the right tail.</p>","PeriodicalId":48363,"journal":{"name":"Journal of Applied Econometrics","volume":null,"pages":null},"PeriodicalIF":2.3000,"publicationDate":"2023-12-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3018","citationCount":"0","resultStr":"{\"title\":\"Nonlinearities in macroeconomic tail risk through the lens of big data quantile regressions\",\"authors\":\"Jan Prüser, Florian Huber\",\"doi\":\"10.1002/jae.3018\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Modeling and predicting extreme movements in GDP is notoriously difficult, and the selection of appropriate covariates and/or possible forms of nonlinearities are key in obtaining precise forecasts. In this paper, our focus is on using large datasets in quantile regression models to forecast the conditional distribution of US GDP growth. To capture possible nonlinearities, we include several nonlinear specifications. The resulting models will be huge dimensional, and we thus rely on a set of shrinkage priors. Since Markov chain Monte Carlo estimation becomes slow in these dimensions, we rely on fast variational Bayes approximations to the posterior distribution of the coefficients and the latent states. We find that our proposed set of models produces precise forecasts. These gains are especially pronounced in the tails. Using Gaussian processes to approximate the nonlinear component of the model further improves the good performance, in particular in the right tail.</p>\",\"PeriodicalId\":48363,\"journal\":{\"name\":\"Journal of Applied Econometrics\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2023-12-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jae.3018\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Applied Econometrics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jae.3018\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Econometrics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jae.3018","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

摘要

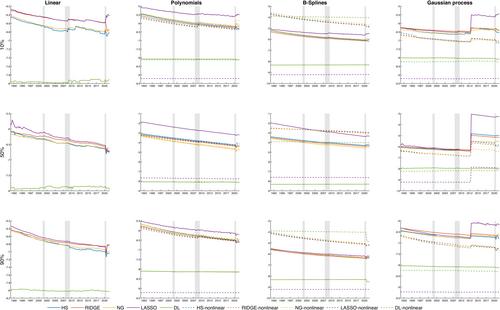

对 GDP 的极端变动进行建模和预测是出了名的困难,选择适当的协变量和/或可能的非线性形式是获得精确预测的关键。在本文中,我们的重点是在量子回归模型中使用大型数据集来预测美国 GDP 增长的条件分布。为了捕捉可能的非线性因素,我们加入了多个非线性规范。由此产生的模型将是一个巨大的维度,因此我们依赖于一套收缩先验。由于马尔科夫链蒙特卡罗估计在这些维度上会变得很慢,因此我们依靠快速变分贝叶斯近似来计算系数和潜在状态的后验分布。我们发现,我们提出的这套模型可以产生精确的预测。这些收益在尾部尤为明显。使用高斯过程来近似模型的非线性部分进一步提高了良好的性能,尤其是在右尾部。

Nonlinearities in macroeconomic tail risk through the lens of big data quantile regressions

Modeling and predicting extreme movements in GDP is notoriously difficult, and the selection of appropriate covariates and/or possible forms of nonlinearities are key in obtaining precise forecasts. In this paper, our focus is on using large datasets in quantile regression models to forecast the conditional distribution of US GDP growth. To capture possible nonlinearities, we include several nonlinear specifications. The resulting models will be huge dimensional, and we thus rely on a set of shrinkage priors. Since Markov chain Monte Carlo estimation becomes slow in these dimensions, we rely on fast variational Bayes approximations to the posterior distribution of the coefficients and the latent states. We find that our proposed set of models produces precise forecasts. These gains are especially pronounced in the tails. Using Gaussian processes to approximate the nonlinear component of the model further improves the good performance, in particular in the right tail.

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: