回报预测中的复杂性美德

IF 7.6

1区 经济学

Q1 BUSINESS, FINANCE

引用次数: 0

摘要

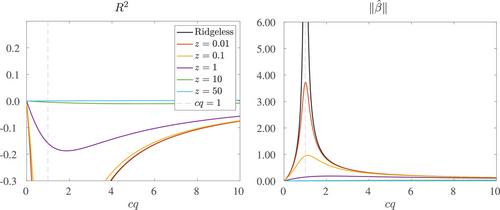

现有文献大多采用仅使用几个参数的 "简单 "模型来预测市场回报。与传统观点相反,我们从理论上证明,与参数数量超过观测数据数量的 "复杂 "模型相比,简单模型严重低估了回报率的可预测性。我们通过实证证明了复杂模型在美国股市回报预测中的优势。我们的研究结果为通过机器学习建立预期收益模型提供了理论依据。本文章由计算机程序翻译,如有差异,请以英文原文为准。

The Virtue of Complexity in Return Prediction

Much of the extant literature predicts market returns with “simple” models that use only a few parameters. Contrary to conventional wisdom, we theoretically prove that simple models severely understate return predictability compared to “complex” models in which the number of parameters exceeds the number of observations. We empirically document the virtue of complexity in U.S. equity market return prediction. Our findings establish the rationale for modeling expected returns through machine learning.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Journal of Finance

Multiple-

CiteScore

12.90

自引率

2.50%

发文量

88

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: