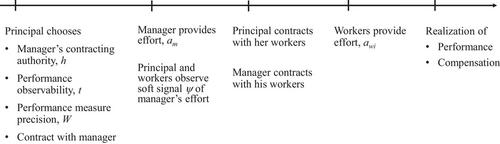

{"title":"等级制度的透明度","authors":"CHRISTIAN HOFMANN, RAFFI J. INDJEJIKIAN","doi":"10.1111/1475-679X.12516","DOIUrl":null,"url":null,"abstract":"<p>We use an agency model to address the benefits and costs of transparency in a hierarchical organization in which the principal employs a manager entrusted with contracting authority and several workers, all under conditions of moral hazard. We define the principal's transparency choices as a decision to allow workers to observe their coworkers’ performances (<i>observability</i>) and as an investment in monitoring worker performance (<i>precision</i>). We find that whereas precision alleviates agency conflicts as expected, observability can exacerbate agency conflicts, especially if the manager's interests are misaligned sufficiently with those of the principal. Our results suggest several testable hypotheses including predictions that opaque performance measurement practices are well suited for small organizational units at lower hierarchical ranks, and in settings where the sensitivity-precision of the available measures is low, workers’ performances are correlated positively, and managerial productivity is modest.</p>","PeriodicalId":48414,"journal":{"name":"Journal of Accounting Research","volume":"62 1","pages":"411-445"},"PeriodicalIF":4.9000,"publicationDate":"2023-10-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12516","citationCount":"0","resultStr":"{\"title\":\"Transparency in Hierarchies\",\"authors\":\"CHRISTIAN HOFMANN, RAFFI J. INDJEJIKIAN\",\"doi\":\"10.1111/1475-679X.12516\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We use an agency model to address the benefits and costs of transparency in a hierarchical organization in which the principal employs a manager entrusted with contracting authority and several workers, all under conditions of moral hazard. We define the principal's transparency choices as a decision to allow workers to observe their coworkers’ performances (<i>observability</i>) and as an investment in monitoring worker performance (<i>precision</i>). We find that whereas precision alleviates agency conflicts as expected, observability can exacerbate agency conflicts, especially if the manager's interests are misaligned sufficiently with those of the principal. Our results suggest several testable hypotheses including predictions that opaque performance measurement practices are well suited for small organizational units at lower hierarchical ranks, and in settings where the sensitivity-precision of the available measures is low, workers’ performances are correlated positively, and managerial productivity is modest.</p>\",\"PeriodicalId\":48414,\"journal\":{\"name\":\"Journal of Accounting Research\",\"volume\":\"62 1\",\"pages\":\"411-445\"},\"PeriodicalIF\":4.9000,\"publicationDate\":\"2023-10-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12516\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12516\",\"RegionNum\":2,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12516","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

We use an agency model to address the benefits and costs of transparency in a hierarchical organization in which the principal employs a manager entrusted with contracting authority and several workers, all under conditions of moral hazard. We define the principal's transparency choices as a decision to allow workers to observe their coworkers’ performances (observability) and as an investment in monitoring worker performance (precision). We find that whereas precision alleviates agency conflicts as expected, observability can exacerbate agency conflicts, especially if the manager's interests are misaligned sufficiently with those of the principal. Our results suggest several testable hypotheses including predictions that opaque performance measurement practices are well suited for small organizational units at lower hierarchical ranks, and in settings where the sensitivity-precision of the available measures is low, workers’ performances are correlated positively, and managerial productivity is modest.

期刊介绍:

The Journal of Accounting Research is a general-interest accounting journal. It publishes original research in all areas of accounting and related fields that utilizes tools from basic disciplines such as economics, statistics, psychology, and sociology. This research typically uses analytical, empirical archival, experimental, and field study methods and addresses economic questions, external and internal, in accounting, auditing, disclosure, financial reporting, taxation, and information as well as related fields such as corporate finance, investments, capital markets, law, contracting, and information economics.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: