跨国企业子公司资本结构:一个新的内部化理论视角

IF 4.1

3区 管理学

Q2 MANAGEMENT

引用次数: 0

摘要

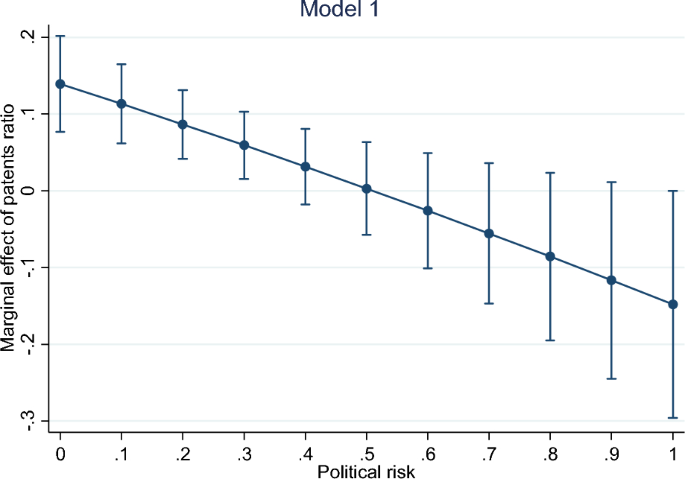

摘要本文从“新内部化理论”的视角对子公司资本结构作为跨国企业内部治理机制进行了研究。我们建立在交易成本理论的论点之上,即股权和债务不仅是金融工具,也是替代的治理结构,股权对于为不能很好地作为抵押品的特定资产融资有用,特别是在外部不确定性很高的情况下。在跨国公司内部,债务代表部分地重新引入市场机制,这种机制可以限制治理成本并加强对子公司经理的激励。但是,如果子公司拥有特定的资产,而这些资产在执行债务合同时将会损失,则债务融资可能是不合适的。利用挪威跨国公司子公司层面的面板数据,我们认为子公司注册的专利代表了跨国公司特有的非地点约束的知识资产,而子公司的研发收入代表了地点约束和子公司特有的资产。我们预测,在外部不确定性条件下,跨国公司特定资产与外债呈负相关,子公司特定资产与所有债务呈负相关。我们的假设只得到部分支持。当以政治风险为形式的外部不确定性较高时,专利与外债呈负相关。然而,我们没有发现由子公司研发收入衡量的地点约束和子公司特定资产的类似显著结果。对于这两项指标,有证据表明债务融资在低风险环境下是可行的。进一步分析表明,与全资子公司相比,合资企业的影响有所不同。我们在部分出乎意料的结果的基础上,提出了子公司资本结构的扩大内部化视角。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Subsidiary Capital Structure in Multinational Enterprises: A New Internalization Theory Perspective

Abstract We study subsidiary capital structure as a mechanism of intra-MNE (multinational enterprise) governance from the perspective of “new internalization theory”. We build on the argument from transaction cost theory that equity and debt are not just financial instruments but also alternative governance structures, with equity useful for financing specific assets that do not serve well as collateral, especially when external uncertainty is high. Inside an MNE, debt represents a partial reintroduction of market mechanisms that can limit governance costs and strengthen subsidiary manager incentives. However, debt financing may be inappropriate if subsidiaries possess specific assets that are lost if debt contracts are enforced. Using subsidiary-level panel data from Norwegian MNEs, we argue that patents registered in the subsidiary represent MNE-specific non-location bound knowledge assets, while subsidiary R&D income represents location-bound and subsidiary-specific assets. We predict MNE-specific assets to be negatively related to external debt, and subsidiary-specific assets to be negatively related to all debt, under conditions of external uncertainty. We find only partial support for our hypotheses. Patents are negatively related to external debt when external uncertainty in the form of political risk is high. However, we do not find similar significant results for location-bound and subsidiary-specific assets, measured by subsidiary R&D income. For both measures, there is evidence that debt financing is viable in low-risk contexts. Further analysis indicates different effects for joint ventures as compared to wholly owned subsidiaries. We build on the partly unexpected results to propose an expanded internalization perspective on subsidiary capital structure.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Management International Review

MANAGEMENT-

CiteScore

6.50

自引率

11.60%

发文量

34

期刊介绍:

Management International Review publishes research-based articles that reflect significant advances in the key areas of International Management. Its target audience consists of scholars in International Business Administration.

Management International Review is a double-blind refereed journal that aims at the advancement and dissemination of research in the fields of International Management. The scope of the journal comprises International Business, Cross-Cultural Management, and Comparative Management. The journal publishes research that builds or extends International Management theory so that it can contribute to International Management practice.

Management International Review welcomes both theoretical and empirical work. Original papers are invited that are based on a solid theoretical basis and a rigorous methodology. In the area of empirical studies, the journal publishes both quantitative and qualitative research. To be published in

Management International Review, a paper must make strong contributions and highlight the significance of those contributions to the field of International Management. The editors are especially interested in manuscripts that break new ground rather than papers that make only incremental contributions.

Management International Review publishes articles and research notes. Every year, six issues are published. On average, two of these issues are Focused Issues, which concentrate on a specific subfield of International Management.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: